Not so long ago, there was no such thing as a credit score. FICO was first introduced in 1958 but didn’t become widely used to score consumer credit until 1989. But today, just three decades later, credit scores are a regular part of our lives, and unless you have enough cash to pay for everything, including a home, you need a good credit score.

Your credit score tells potential lenders how likely you are to repay borrowed money. Every time you apply for a credit card, a car loan, a mortgage, a personal loan, a business loan, or a refinance, your credit score will be checked. Your credit score is also checked when you rent an apartment; some employers will run a credit check on prospective employees.

If you have a good credit score, you’ll get a better interest rate when you borrow money. The only time this doesn’t apply is in the case of credit cards. Credit cards have a set interest rate, and it doesn’t change according to your credit score. But you may be refused a credit card if you have poor credit.

Two of the most expensive things in life are taxes and interest, so if you don’t have a good credit score, life will be more costly than it has to be. So if your credit isn’t stellar, let us show you how to fix bad credit.

What is a Credit Score?

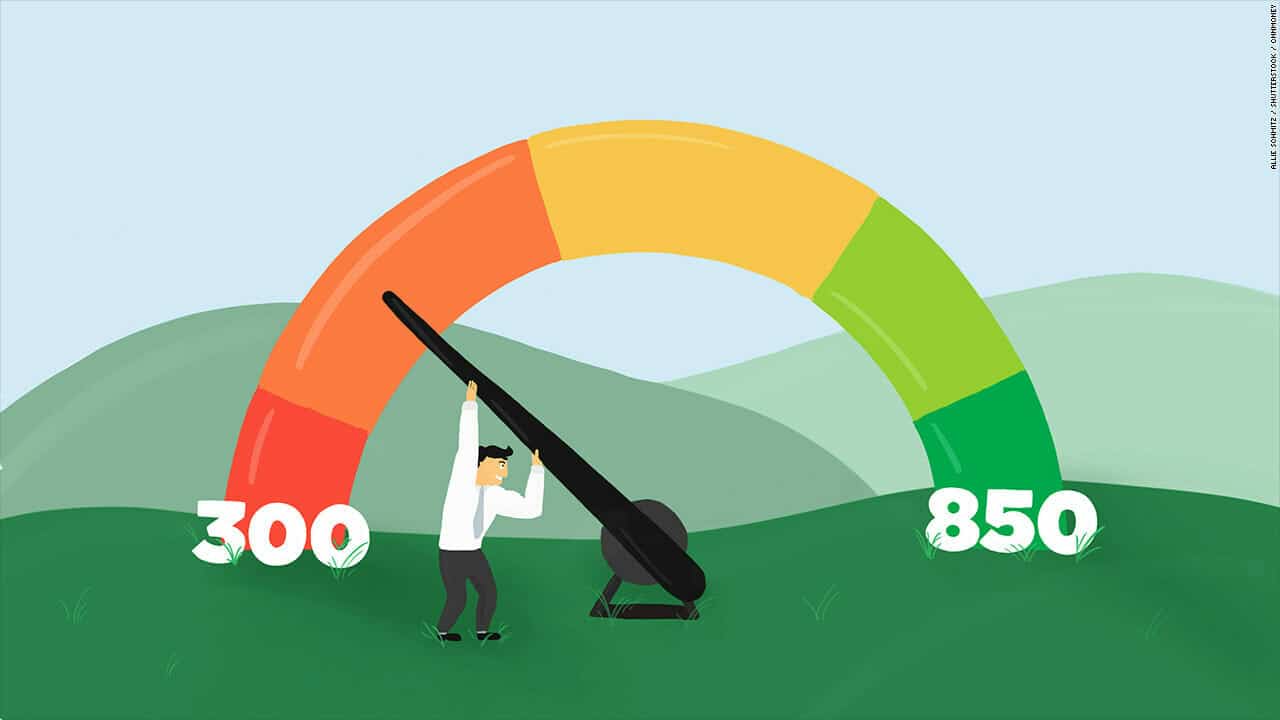

Your credit score is a three-digit number that tells potential lenders how likely you are to repay your debts. The number is based on the information in your credit report. Your credit report is a history of money you’ve borrowed and how you paid that money back. Or did not pay it back.

Credit scores have a range:

- Bad Credit: 300-630

- Fair Credit: 630-689

- Good Credit: 690-719

- Excellent Credit: 720-850

There is some variation to these numbers because each credit reporting company has its proprietary formula to calculate consumer credit scores, but this range tells us what we need to know.

What Makes Up a Credit Score

Payment History: This means how good you pay your bills on time. The best way to build, improve, or maintain a good credit score is always to pay all of your accounts on time. Late payments will impact your score negatively. This is 25% of your credit score.

Credit Utilization: This is the percentage of your available credit you’re using. Ideally, your utilization ratio is under 30%. For example, if you had one credit card with a $1,000 limit, you would charge no more than $300 each month before paying it off. This is 25% of your score.

Derogatory Remarks: These are negative items like accounts sent to a collection agency, bankruptcies, and civil judgments. This is 25% of your credit score.

Length of Credit History: This shows how long you’ve had credit, averaged out across all your accounts. This is 12.5% of your score.

Total Accounts: This tells lenders how many open accounts you have and what kind. The more diverse your bills (credit cards, personal loans, mortgage, etc), the better. This is 6.3% of your credit score.

Credit Inquiries: These are how many times lenders have checked your credit. There are soft credit inquiries and hard credit inquiries. A soft check is done when you shop for rates on a personal loan. These don’t impact your credit score. A hard inquiry is made when you apply for credit. For instance, a hard question is done if you apply for a credit card. These do impact your credit score but not by much. This is 6.3% of your credit score.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

Who is Scoring You?

There are three leading credit reporting agencies; Equifax, Experian, and TransUnion. They compile consumer credit reports and credit scoring models like VantageScore and FICO. These proprietary formulas are used to calculate your credit history into a three-digit number, and voila! We’re all tattooed for life with our credit score.

If you follow personal finance news, you’ll probably remember Equifax for this;

Equifax disclosed that hackers stole the personal information of 147.7 million Americans from its servers. Hackers infiltrated its network and stole customer names, Social Security numbers, birthdates, and addresses, affecting more than half the US population.

How to Fix Bad Credit

If you don’t know your credit score, you can check it in several places. Credit Karma will give you a free score and a breakdown of that score. Most credit card companies and some banks also offer free credit scores.

You might think that if you have a good credit score, you don’t need to know how to fix bad credit because you don’t have bad credit. But everyone should check their credit report regularly. There can be mistakes on those reports that mean your credit score is not as high as it could be. Regularly checking your credit report is also an excellent way to protect yourself against identity theft.

Where to Get Your Credit Reports

If you try to find information online about getting your credit report, you’ll find lots of sites offering free accounts. But most of those sites are credit monitoring sites, and they’ll ask for a credit card number. You don’t need to pay someone else to monitor your credit report; you can do it for free.

The site you want to go to get a free copy of your credit reports is annualcreditreport.com. The Fair Credit Reporting Act (FCRA) requires each credit reporting agency (the primary three, Experian, Equifax, and TransUnion) to provide consumers with a free copy of their credit report once every twelve months. You can request your free reports online, read them online, and print them out.

Order all three reports because they will likely have some different information on them, and you want the most complete picture possible so you know how to fix bad credit.

What to Look For

Correct Identifying Information: Each of your credit reports will list your name, date of birth, Social Security number, current and past addresses, phone numbers, and employers. For instance, if your middle initial is wrong, it can mean information that isn’t yours is on your report.

Existing Credit Information: This is a detailed list of all your credit accounts, open and closed. It shows the opening dates, credit limit or loan amount, co-signer information, recent account balances, monthly payments, recent payments, and complete or partial account numbers.

This is the worst section to go through. It takes tons of cross-referencing with things like your Mint account, online bank, and credit card statements, and you might have to dig to verify information on closed accounts. It’s essential to go through it carefully because if you’ve been the victim of identity theft, you’ll see it here.

Accounts closed in good standing will appear on your report for ten years. Accounts closed in lousy standing will drop off your information after seven years.

Payment History: This section shows a two-year record of account statuses. Suppose they were paid or are past due. Missed payments drop off after seven years. This is the most critical area to check because it’s such a significant factor in your credit score. Again, a PITA to cross-reference but worth it when you consider how to fix bad credit.

Public Records: This information comes from transactions recorded by government entities and includes things like buying real estate, liens, foreclosures, bankruptcies, civil judgments, and divorces. This part is easy. Most of us remember all of our divorces.

Credit Inquiries: This shows companies or individuals who have requested a copy of your report in the past two years. This is another good section to find identity theft.

The Next Step: Disputing Errors

Under the FCRA, credit reporting agencies and the entity providing the information must correct information on your credit report that is not accurate or incomplete.

You can dispute the information with all three credit reporting agencies online or in writing. Ideally, you’ll do both to have an electronic and a paper trail. Anything you mail should be sent certified so you have proof of delivery.

Your dispute should include a copy of the report with specific information about what is inaccurate, any information proving your claim, and a request that the incorrect information is removed.

This is the moment all that cross-referencing pays off. Include as much proof as you can. If your report shows you made a late student loan payment but you have an e-receipt showing otherwise, include the receipt. You can also include a screenshot or print out of your checking account statement showing the money left your account on or before the due date.

The credit reporting agencies have 30 days to investigate and respond. Then, they must forward the information and proof you’ve provided to the entity that provided the disputed information. If the entity agrees the information is incorrect, it must notify all three credit bureaus so your file can be updated.

Once the process is complete, the credit bureaus must provide you with the results of the investigation in writing and a free credit report if the report has changed based on the research.

Disputing Their Dispute

You can escalate things to the Consumer Financial Protection Bureau online if they dispute your dispute. You can also start an appeal with the credit reporting agency. You should appeal to the body misreporting the information too, and ask them to correct the information with the credit bureaus.

I didn't come this far only to come this far.

Tweet ThisIf you still don’t get the desired result, request that a copy of the dispute be attached to your credit file and included in your future credit reports. Sorry, having a debate on your credit report won’t improve your credit score, but it can show potential lenders that you don’t believe the information to be entirely accurate.

Identity Theft

Dealing with identity theft is different from correcting misinformation on your credit report. Identifying theft is a serious matter and can devastate your entire life, not just your financial life. However, the Federal Trade Commission (FTC) has a website where you can report possible identity theft, get a recovery plan, and get help from people who can walk you through the process.

You also need to contact each credit reporting agency and ask them to put a fraud alert on your account. The next step is to put a freeze on your credit reports. If a potential creditor can’t access your report, they won’t open any new accounts in your name (i.e., the thief or thieves can’t open new accounts in your name).

Lastly, file a police report. The cops aren’t going to do jack shit but creditors may ask for the report when you’re disputing information.

Ask for an Update

Once the information is corrected, you have a right to ask the credit bureaus to send the updated information to any company or person who pulled your credit report in the past six months.

Monitor Your Report

The best way to monitor your credit report is to get a free credit report from a different reporting bureau once every four months. Yes, each report has slightly different information, but getting a report quarterly means you don’t have to wait for a year between receiving a report or paying for a report.

So every four months, get a report and look for the negative information we discussed and any new credit accounts that you did not open. This is especially important for those who have been a victim of identity theft.

The faster you catch onto the fact that someone is using your identity to open new credit accounts or seek medical treatment (this is an increasingly common form of identity theft), the sooner you can start repairing the damage.

Credit Repair Services

A credit repair service will request a copy of your credit reports, comb through them, and tell you what information they think should be disputed. The service will outline a plan for disputing errors and negative information. They may request the information provider validate the debt, send dispute letters, or cease-and-desist letters to collection agencies.

Some credit repair services charge a flat fee and some a monthly fee. These services really don’t do anything you can’t do yourself. That’s why we wanted to write a guide on how to fix bad credit; you wouldn’t have to pay a service to do something you can do for free.

But for some of us, time is money. It’s understandable if you want to hire someone else to do this. It’s not difficult but can be time-consuming and probably not anyone’s idea of a good time.

Don’t Go Nuts

Should everyone get copies of their credit reports and go through them? Yes, we all should. But should we all start disputing things left and right? Probably not. The process of disputing things on your credit score can take time and be frustrating. Of course, if you’ve been the victim of identity theft, you have to address it.

But if there are just a few errors on your reports and they aren’t in areas that have a high impact on your score, there are easier ways to build a better credit score.

And while having a good credit score is important, it’s only important when you’re planning to borrow money in the form of applying for a credit card, mortgage, car loan, personal or business loan, or a refinance on current debt. You want your credit score to be as high as possible before borrowing money. You’ll get the best interest rates as long as your credit score is 760 or above. No need to strive for 850.

There is a caveat to this: An open dispute on your credit report can negatively impact your mortgage application.

Disputes are supposed to be resolved in 30 days but it can take much longer. Mortgage lenders know that a credit report under dispute may not be an accurate representation of a borrower’s creditworthiness. However, it may require the dispute to be resolved before approving the loan.

If you plan to apply for a mortgage, wait a few months after the last dispute has been settled.