Peer to peer lending is a new concept for some, and while it’s relatively new, it’s been around in its current form for over a decade.

In the wake of the 2008 financial crisis, traditional banks and other financial institutions were overly cautious. Many had spent years leading up to 2008, making loans to anyone with a bank account without regard to their credit history. They got burned (although nowhere nearly as burned as the taxpayers who got stuck with the bill for the poor, risky decisions of these financial institutions) and in the aftermath, banks were loathed to make loans unless a borrower had a practically perfect FICO score.

But people still needed to borrow money whether for personal loans, debt consolidation, or small business loans. Peer to peer lending platforms like

It’s a mistake to think of peer lenders as second-class lenders compared to banks and other more traditional financial institutions. Peer lenders often have some significant advantages over banks including looser credit score requirements, a wider range of loan amounts, more favorable loan terms, fewer fees, and best of all, lower interest rates. Millions of Americans have used a peer to peer lender.

Roughly 26% of Americans said they used a P2P lending service. It’s predicted the domestic market would be worth as much as $86 billion in 2018. And by 2024, the global industry was expected to climb as high as $898 billion by 2024, according to a report by Transparency Market Research.

Intrigued but wondering how does peer to peer lending work? We’ll explain everything you need to know and give you the rundown on some of the best peer to peer lending sites.

What is Peer to Peer Lending for Borrowers?

Peer-to-peer lenders make unsecured personal loans and small business loans. The peer lending platforms don’t make the loans; they act as the middle man between a borrower and a lender. The platforms use an algorithm to connect borrowers like you and me to individual lenders.

A borrower who may have bad credit (or at least a credit score not good enough to get bank loans) can get peer loans often faster and at a lower interest rate than a bank offers. And the individual lender has the opportunity to earn interest on the money they lend just as a bank does.

You may also see this referred to as p2p lending, p2p platforms, p2p lenders, or peer lending sites.

In the Dark Ages, if you needed to borrow money, you went to a local bank or credit union and applied for a loan. This was a lengthy, arduous process requiring reams of paperwork and documentation. A loan officer would look at things including your credit score, debt-to-income ratio, and the amount of money in the bank account you maintained with them.

Based on this information, the loan would be made or denied. P2P lending platforms have completely streamlined this process. Some borrowers will have the loan money in their bank account within a few business days of starting the loan process.

How Does Peer to Peer Lending Work for Borrowers?

Every peer lending company has its own process, but in general, they all work pretty similarly. This is how the process works for borrowers:

- Answer some questions about your personal financial situation and the type of loan you want. This process will allow the p2p lending platform to run a soft credit check, which will not impact your credit score.

- Based on this soft credit score, you will be assigned a loan grade which tells potential lenders how high risk or low risk you are. Based on this grade, they will decide if they want to lend you money. Once enough, investors are willing to fund your loan; the loan will be approved.

- A borrower now provides the requested documentation including things like proof and length of employment, total income, and the amount of debt they have if any. All documentation is reviewed for accuracy, and borrowers may need to provide additional information and documents.

- Once the loan approval is complete, the finalization documents are sent to the borrower. Once the forms are signed and returned, the loan money is wired into the borrower’s bank account, usually with two business days.

Nearly all p2p loans can be handled entirely online — no need to go into a bank or even talk to anyone on the phone. The required forms and documents between a borrower and the lending platform can all be sent back and forth via scanning and emails.

Most p2p personal loans are between $2,000 and $35,000, although some offer bigger loans. The loan term is often between three years and five years. Some peer lending companies have an origination fee of 1% to 5% of the loan amount and is deducted from the borrowed funds before the funds are transferred to a borrower.

Types of Loans

Each peer platform lending site offers its own loan products. These are some standard offerings.

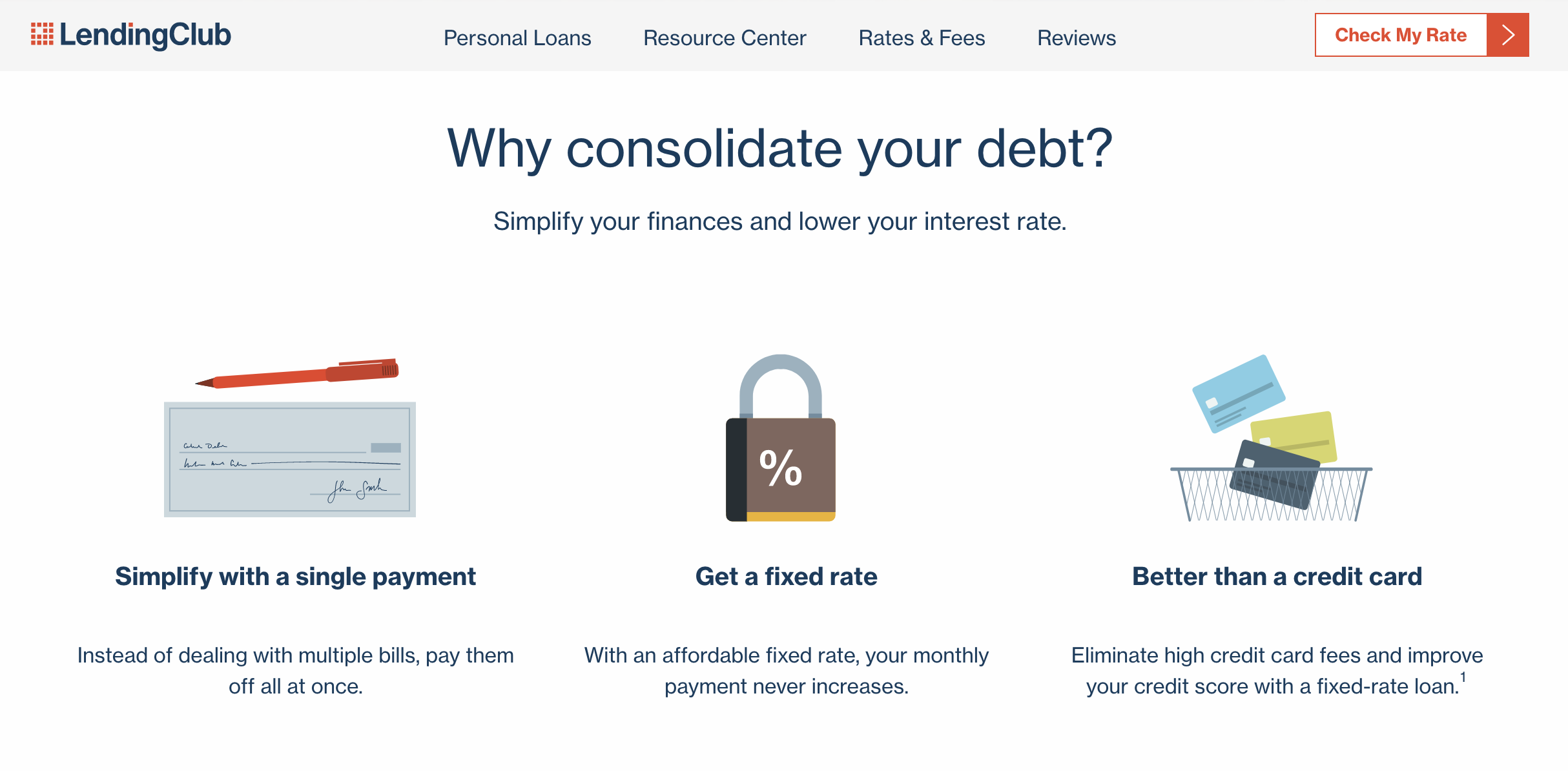

Personal Loans: Unsecured, (the loan does not require a borrower to provide collateral) fixed-rate personal loans are the bread and butter of most p2p lenders. If your credit score is good enough, you can typically borrow up to $35,000 with a loan term between two and five years. Interest rates (depending on your credit score) generally start in the mid-single digits. Personal loans can be used for anything, including debt consolidation, home improvement projects, and even a car.

Business Loans: If it’s challenging to get a personal loan from a bank, it’s doubly so for business loans. Once again, p2p lenders have stepped up to fill a gap. Four of the biggest peer-to-peer sites,

Mortgages and Refinances: P2P lenders are slowly wading into the mortgage and mortgage refinancing aspects of lending. SoFi, perhaps best known for student loan refinancing, now offers mortgages and mortgage refinancing (not in every state currently), and

Student Loan Refinancing: Earnest offers some of the lowest interest rates (as low as 2.27%) and lets you pick a customized payment plan. CommonBond is a more recent player in the field also offering competitive rates.

Healthcare Loans: Most of us are all too aware of the rising cost of health care in America. While you can take out a personal loan from a peer-to-peer lender to cover medical expenses,

Best Peer-to-Peer Lenders for Borrowers

This isn’t an exhaustive list of p2p lending platforms, but we consider them to be among the best.

Lending Club: Lending Club offers a variety of loans. Borrowers can take out a personal loan for up to $40,000. APRs for personal loans range from 6.95% to 35.89% and have fixed rates and fixed monthly payments.

Prosper: Prosper offers a variety of loans. Borrowers can take out a personal loan for up to $40,000. APRs for personal loans range from 6.95% to 35.99% and have fixed rates and fixed monthly payments.

Upstart: Upstart offers a variety of loans. Borrowers can take out a personal loan for up to $35,000. APRs for personal loans range from 7.46% to 35.99% and have fixed rates and fixed monthly payments.

Funding Circle: Funding Circle offers small business loans from $25,000 to $500,000. APRs range from 4.99% to 39.6% and have fixed rates and fixed monthly payments.

What is Peer to Peer Lending for Investors?

We’ve established that the money for p2p loans doesn’t come from the lending platforms. The money comes from regular people. This is how peer to peer lending works for those investors.

How Does Peer to Peer Lending Work for Investors?

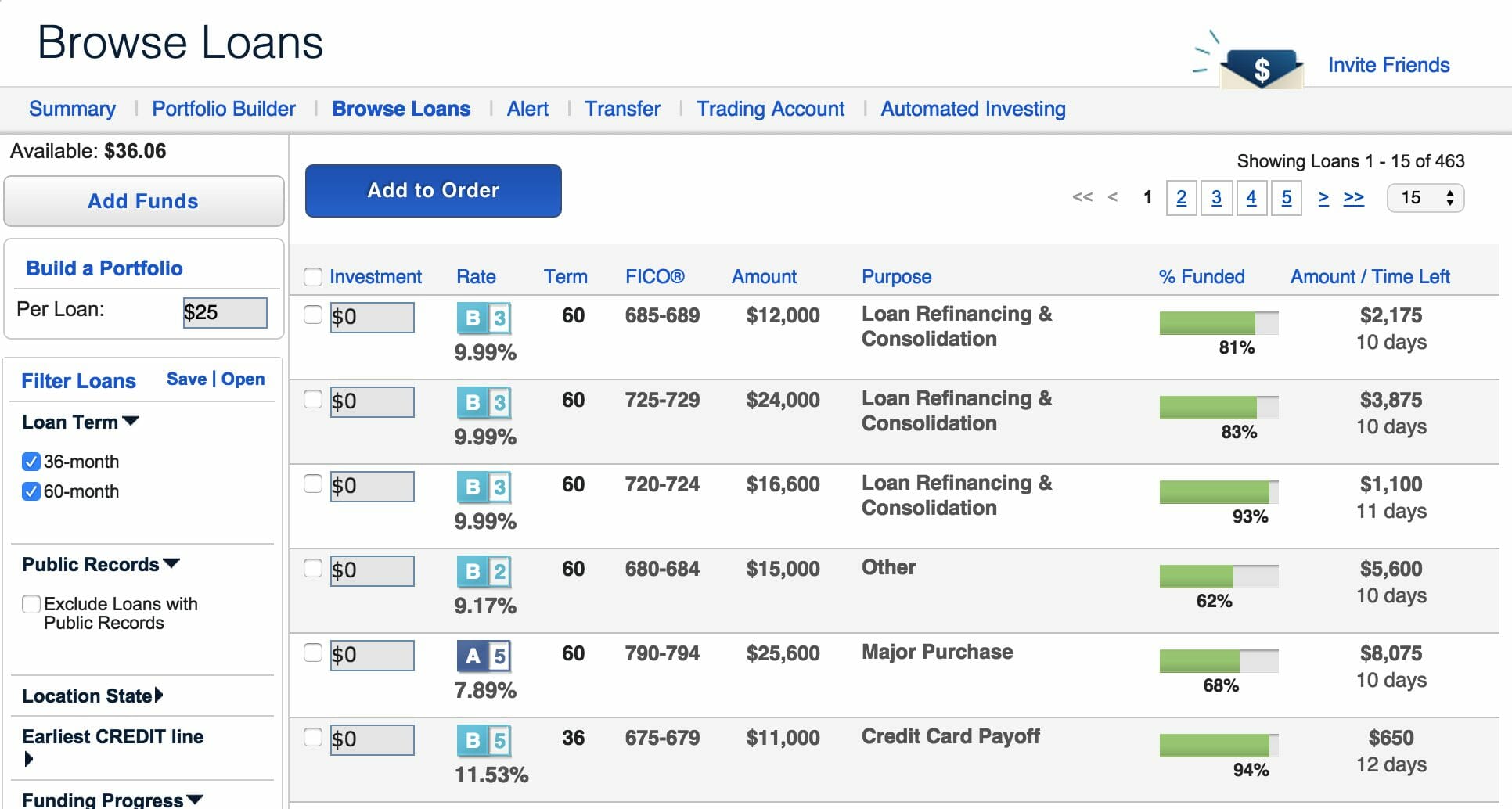

P2P lending platforms let investors buy consumer debt with the hope of making a return on that buy. Investors can peruse borrower profiles and based on the information in them, choose which borrowers they want to loan money to.

Most loans are crowdfunded, meaning more than one investor funds each loan. Most platforms have a minimum dollar requirement to invest, and investors can choose how much they want to invest in each loan. It’s best to invest smaller amounts in several loans rather than a more substantial amount in a single loan. If one of your borrowers defaults, your other investments can absorb some of the loss. It’s a way to diversify this type of investment.

When borrowers make their monthly payments, part of it goes to each investor until the loan is paid in full. Sounds kind of high risk, doesn’t it? You don’t really know who you’re lending to and your money isn’t FDIC insured as it is when you stick it in a savings account. P2P investing is riskier than say, buying bonds, but you can mitigate the risk by investing in several loans, and it’s a way to include some diversity in your portfolio. And higher risk investments can have higher returns than more conservative investments.

Best Peer-to-Peer Lenders for Investors

Some states have imposed restrictions on p2p investing, so the option isn’t available everywhere.

Lending Club

- Lenders must have a gross income and a net worth of at least $70,000 ($85,000 in CA). The income requirement is waived with a net worth of $250,000 or more.

- $25 minimum investment with a $1,000 minimum in your account.

- You can invest through a taxable investment account or an IRA account.

- Investors pay a 1% annual fee.

Prosper

- Lenders must have a gross income and a net worth of at least $70,000 ($85,000 in CA). The income requirement is waived with a net worth of $250,000 or more.

- $25 minimum investment with a $1,000 minimum in your account.

- You can invest through a taxable investment account or an IRA account.

- Investors pay a 1% annual fee.

Upstart

- Must be an accredited investor.

- You must open an account with at least $100.

- You can invest through a self-directed IRA account.

- Investors do not pay any fees.

- Investors cannot choose individual loans to invest in. Instead, they choose to invest in a specific loan grade or loans with set criteria.

Funding Circle

- Must be an accredited investor.

- You must open an account with at least $50,000. The minimum investment per loan is $500.

- You can invest through a taxable investment account or an IRA.

- There is a 0.083% service charge on loans per month.

Fiscal flexibility that’s funny, free and delivered weekly.

Never a Lender or Borrower Be?

Peer-to-peer lenders are a relatively new phenomenon. Should you use one on either side of the equation?

Pros for Borrowers

- For those with imperfect credit, p2p lenders are often more willing to loan money than banks.

- Depending on your credit score, you may get a better interest rate with a p2p lender than a bank.

- The process is fast and can be done entirely online.

- You can window shop for the best rates with no impact to your credit score.

- Many p2p lenders charge fewer fees than banks.

- Borrowers don’t need collateral.

Cons for Borrowers

- You can’t borrow your way out of debt. If you get a p2p loan for debt consolidation but don’t curb irresponsible spending, you’ll only compound the problem.

- For those with bad credit, the interest rates are high.

Pros for Lenders

- Some platforms have very small minimums.

- Thousands of loans to choose from.

- A great way to diversify investments.

- Provides passive income in the form of the monthly payments investors receive.

Cons for Lenders

- Some platforms require investors to be accredited, putting them out of reach for many.

- Borrowers may default making p2p investing something of a high-risk investment.

- In order to be considered diversified within p2p investing, some experts suggest investing in as many as 175 loans. This is a lot to keep track of.

- Your money is locked up for the term of the loan which can be up to five years. Once you make the investment, you can’t sell it.

In our estimation, there are more cons for potential investors than borrowers. As long as you’re borrowing for the right reason (to consolidate debt not to go on a blow-out vacation, for example), a p2p loan can be a great tool.

That’s not to say p2p can’t be an excellent tool for investors too, but it does come with some risk. Of course, all investments do, but if you buy stock in Apple, it’s pretty unlikely that the company will go under and you’ll lose all of your investment. Whereas if a borrower defaults on a loan, something that does happen, you’ve invested it, you do indeed lose all of your investment.

Take the risk or lose the chance.

Tweet ThisIf you’re going to invest this way, make sure it’s with money you can afford to lose, you carefully research each borrower before funding their loan, and you diversify by investing relatively small amounts across several loans.

Because sometimes it does pay to borrow and lend.

Show Notes

Andrew’s Article: Andrew details the success he has had as a