Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

We tend to talk about stocks much more often than bonds. Why? Because since LMM began, our audience has skewed young, most of our listeners are in their twenties and thirties. But the show has been around for seven years now. Those who have been with us from the beginning are seven years older.

We want to serve our audience, so we need to focus a little more on bonds. Most of you know the basics, and we’ve covered bond investing in the past. But now we’re going to go a little deeper into the weeds and talk about the yield curve.

For those listeners who have been with us from the beginning or newer listeners who’ve worked their way through the LMM catalog, today’s guest will be familiar.

J. David Stein has been on the show a few times. He has his own podcast, Money For the Rest of Us, and has a book coming out soon. David is back to explain what the yield curve is and why we need to know.

Is the yield curve a sure sign of a coming recession? If so, what can we do to prepare for it? Rethink our whole investment strategy, sell off all of our investments (definitely not!), build a bunker, and buy some gold bars. Or is all the talk about the yield curve scaremongering that we should just tune out?

What is a Bond?

A bond is a debt instrument, a loan made to a large entity like the U.S. government, a city, or a corporation. Bonds are considered a fixed-income investment. You loan the entity money, earn interest on that loan, and are repaid the face value when the bond matures. Bonds are typically safer for your investment portfolio than stocks, but with lower risk comes lower returns.

You can go directly to the source to buy individual bonds or own lots of bonds within a mutual fund or exchange-traded fund. What you need to know about a bond is what a bond’s yield is, its cash flow. The yield is sensitive to changes in interest rates. When interest rates change, the value of a bond changes. The longer the maturity, the more sensitive a bond is to interest rates.

Why Bother Owning Bonds?

If you can make more money investing in stocks than bonds, why bother with bond investments? Some pay about the same as a money market account or high-yield savings account. Because there is such a thing as having too much risk in your portfolio. Bonds reduce that risk, and the standard advice is to increase your asset allocation, so it’s more heavily weighted towards bonds as you age.

Your bond portfolio acts as a counterweight to your stock portfolio.

There’s a simple rule of thumb to estimate bond returns, the SEC Yield.

The SEC yield is a standard yield calculation developed by the U.S. Securities and Exchange Commission (SEC) that allows for fairer comparisons of bond funds. It is based on the most recent 30-day period covered by the fund’s filings with the SEC. The yield figure reflects the dividends and interest earned during the period after the deduction of the fund’s expenses. It is also referred to as the “standardized yield.”

If you hold a bond for seven or so years, the SEC Yield is a reasonable estimate of your return.

Are There High-Yield Bonds?

We all want the best of both worlds when it comes to personal finance. A safe investment with a high return. Can a high-yield bond provide that?

A high-yield bond has a lower credit rating than investment-grade corporate bonds or other types of bonds. The higher risk of default means that high-yield bonds pay higher yields than other bonds. Also known as “junk bonds,” high-yield bonds have a rating below BBB from Standard & Poor’s, or below Baa from Moody’s.

Some years high-yield bonds have had better returns than both investment-grade bonds and stocks. And some years high-yield bonds have underperformed both.

But a lack of creditworthiness may be enough to put a lot of you off this type of bond.

The Risks Associated with Investing in Bonds

No investment is risk-free, not even bonds. What is your risk tolerance?

Risk from Inflation

Because the interest payments on a bond are fixed, inflation can erode their value. The longer the term of the bond, the greater the inflation risk. On the other hand, deflation increases the worth of the dollars that bond investors are paid.

Interest Rate Risk

Bond prices move in the opposite direction of interest rates. When interest rates rise, bond prices go down because new bonds are issued, and they pay higher coupons, which makes the older bonds with lower yields less attractive. The longer a bond’s term, the more volatile they are.

But bond prices go up when interest rates drop because the old bonds have higher payouts than the newly issued bonds.

Call Risk

Some corporate or municipal bond issuers can redeem or “call” their bonds before the maturity date. When that happens, the issuer must pay the bondholders par value only. This usually happens when interest rates fall, and the bond issuer wants to lower its costs by selling new bonds with a lower yield.

Credit Risk

The bond issuer is unable to make its payment on time or at all. This is what we talked about in the high-yield bond section. So-called junk bonds are at the highest risk for this. Government bonds don’t run this risk. If the U.S. Treasury can’t make its bond payments, we’ll all have more significant problems.

Fiscal flexibility that’s funny, free and delivered weekly.

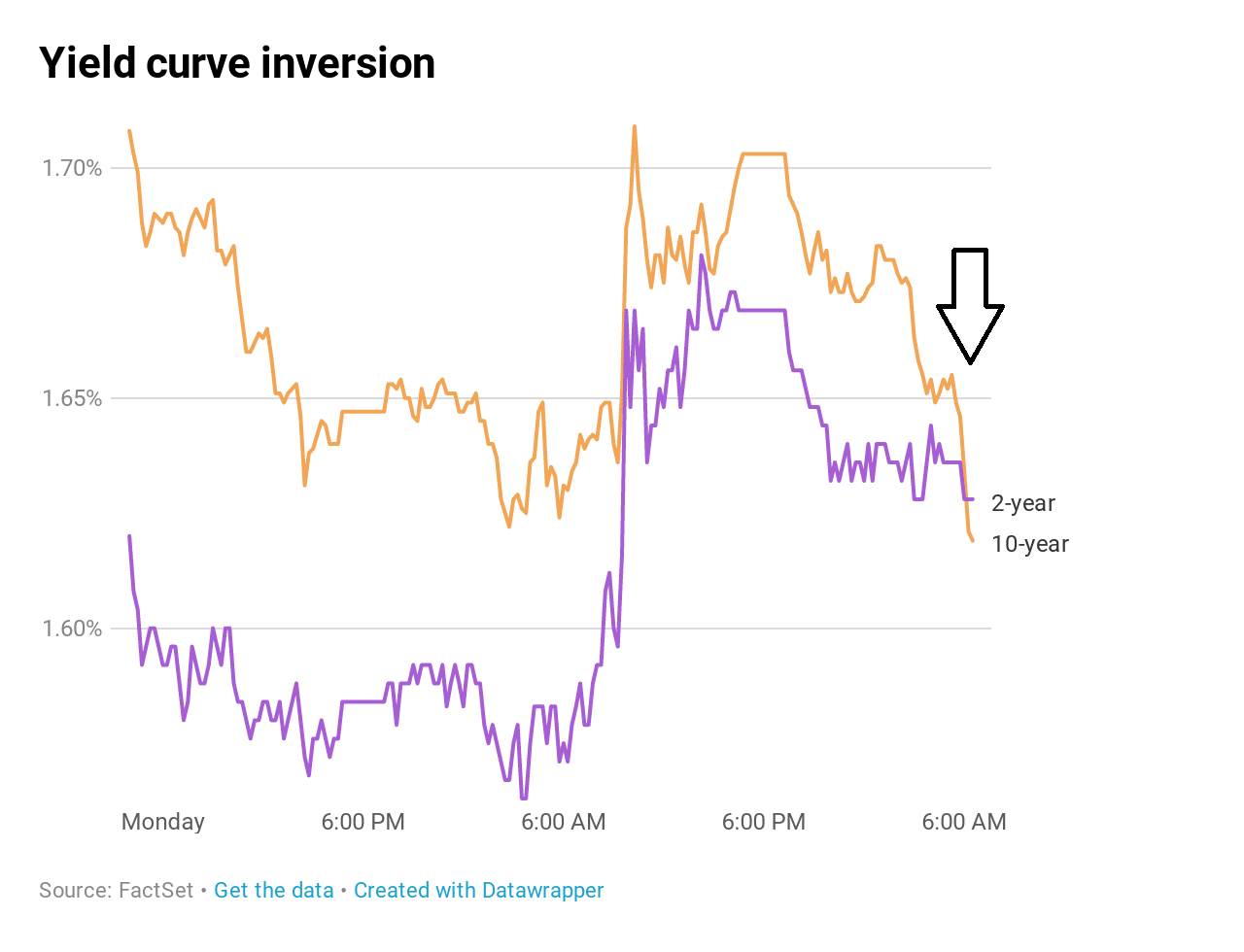

What is a Yield Curve?

is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity. There are three main types of yield curve shapes: normal (upward sloping curve), inverted (downward sloping curve) and flat.

In a normal yield curve, long-term bonds have a higher yield compared to short-term bonds because of the risks associated with time, primarily inflation and interest rates, as discussed above.

The Inverted Yield Curve

The inverted yield curve is when short-term bond yield rates are higher than long-term yields. Why do we hear about this concept so much lately? Because the phenomenon in the bond market can be a sign of a coming recession.

Central banks can lower interest rates when they fear a recession because doing so is a way to encourage people to borrow money to do things like buy homes and cars, things that stimulate the economy. This causes IYC. So is it a sign of a recession this time?

Other Signs of Recession

The drumbeat about another recession has been happening for a while now. Is it true, or is there something else going on?

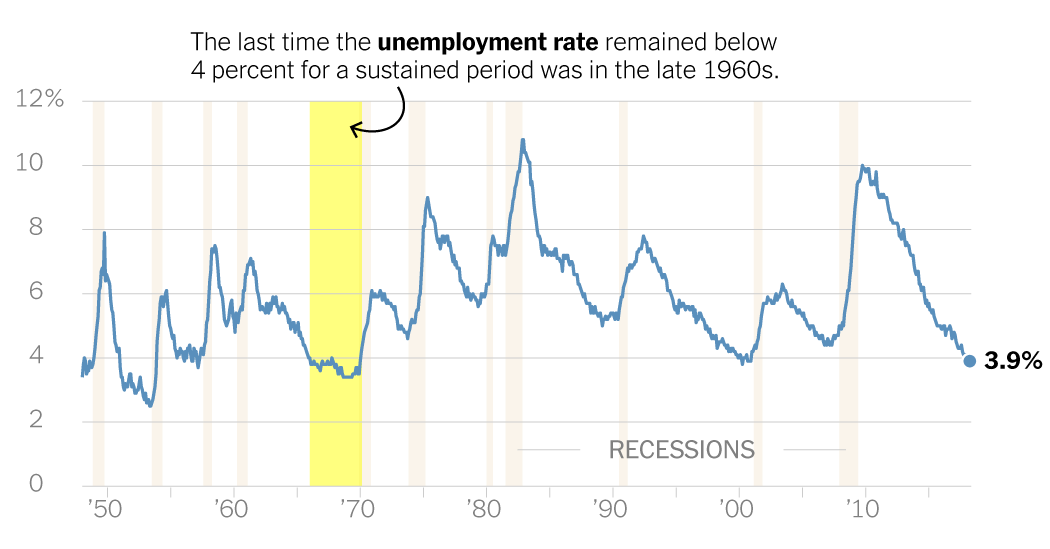

The Unemployment Rate

Higher rates of unemployment typically come during or after a recession. But the United States economy has added close to 20 million jobs since the last recession.

The most recent unemployment numbers came out in August 2019 and are at 3.7%. That was a small increase from June 2019 when the rate was at 3.6%, a 49-year low.

PMI Surveys

PMI is the Purchasing Manager’s Index:

The Purchasing Managers’ Index (PMI) is an index of the prevailing direction of economic trends in the manufacturing and service sectors. It consists of a diffusion index that summarizes whether market conditions, as viewed by purchasing managers, are expanding, staying the same, or contracting. The purpose of the PMI is to provide information about current and future business conditions to company decision makers, analysts, and investors.

The manufacturing aspect of the survey is nearing contraction levels but hasn’t nose-dived off a cliff as you would expect prior to a recession. Non-manufacturing industries are still in expansion mode.

The stock market climbs a wall of worry.

Tweet ThisShiller PE Ratio

Nobel prize-winning economist Robert Shiller created the cyclically adjusted price-earnings (CAPE) ratio, which is based on average inflation-adjusted earnings from the past ten years and is used as a way to assess whether the current market is overvalued or undervalued.

The CAPE ratio is at a near-record high, nearly double its long-term historical average of 16.8.

Is IYC Always a Sign Of Recession?

Not always and when IYC has been a precursor to a recession, the recession has happened 1 to 3 years after the IYC. So if a recession is coming, to the United States and possibly the larger world(and lots of people including LMM, think it is), we may have a few years.

So why all the hand wringing and dire predictions? Because people were severely burned in the last recession and they haven’t forgotten it. They’re always sort of flinching, just waiting for the next one. We’ve been in a recovery from the 2008 recession for a decade. Is it still even considered a recovery a decade on? That’s a long period of time.

But if you lived through it, you understand. It sucked, people lost their jobs, their homes, and their savings.

No wonder we’re poised continuously for the next blow. What will the next blow be, a full recession? Not necessarily. It could be a slowing down of the economy or a mild recession. But you know, those don’t make for sexy, the sky is falling headlines.

What Should We Do With This Information?

Ignore it mostly. A lot of you email and ask what Andrew and Laura are doing with their investments, and they do think a recession is coming and in the not too distant future. Check out our first Golden Butterfly episode and the follow up to find out.

In the case of a full-blown recession, how badly your investments will be impacted depends mostly on the size and time horizon of your investment portfolio. If you have millions invested and you lose 50% of it, that will suck, but you can absorb it. If you’re a long way from retirement and not going to touch your investments for a decade or two or three, you’ll be fine. Your money has time to recoup even a significant loss.

If you’re feeling nervous and are in neither of those positions, you can always change your allocation to a more conservative one. Understandably, your risk tolerance goes down when things are uncertain. Your investment objectives can change.

If the economy does tank, you can take some of your money and buy up stocks cheap. You might also consider diversifying your portfolio by adding an additional asset class. You know we like real estate be that a rental property or a REIT.

That’s it. We’re buy and hold just like always; inverted yield curve be damned!

Show Notes

Flatter Flatter: An IPA from SingleCut Beersmiths

Blue Light Rain: An unfiltered German Pilsner from Knotted Root Brewing Company

Money for the Rest of Us: J. David Stein’s site and podcast.

![Universal Basic Income: Is It Just Another Handout? [UPDATED]](https://www.listenmoneymatters.com/wp-content/uploads/2018/01/LMM-Cover-Images-66-768x432.jpg)