Competition is heating up among the Robo-Advisors. We get a lot of emails asking which is better. So, we broke down each of the services to see who deserves your investment. This is the Betterment vs Wealthfront vs Acorns face-off.

The whole point of going with a

For someone just looking to invest with the right service, it’s getting harder and harder to tell where you should put your money.

Before we get started, I also wrote an incredibly in-depth

In this article, I’ll be focusing more on the nuances of each service as opposed to which types of investment accounts they offer (e.g., SEP IRAs), required minimum balances, or annual fees.

Which Robo-Advisor Is Best?

Minimum Investment:

$500

Management Fees:

0.25%

Promotion:

Invest your first $5,000 free, for life

Tax Loss Harvesting:

Yes

Portfolio Rebalancing:

Yes

Assets Under Management:

$10 billion

Minimum Investment:

$0

Management Fees:

$1, $2 or $3 a month.

Promotion:

Signup and get $5

Tax Loss Harvesting:

No

Portfolio Rebalancing:

Yes

Assets Under Management:

$1 billion

On paper, they’re very similar, but as you know, the devil is in the details. To objectively compare

Round 1: User Experience and Aesthetic Appeal

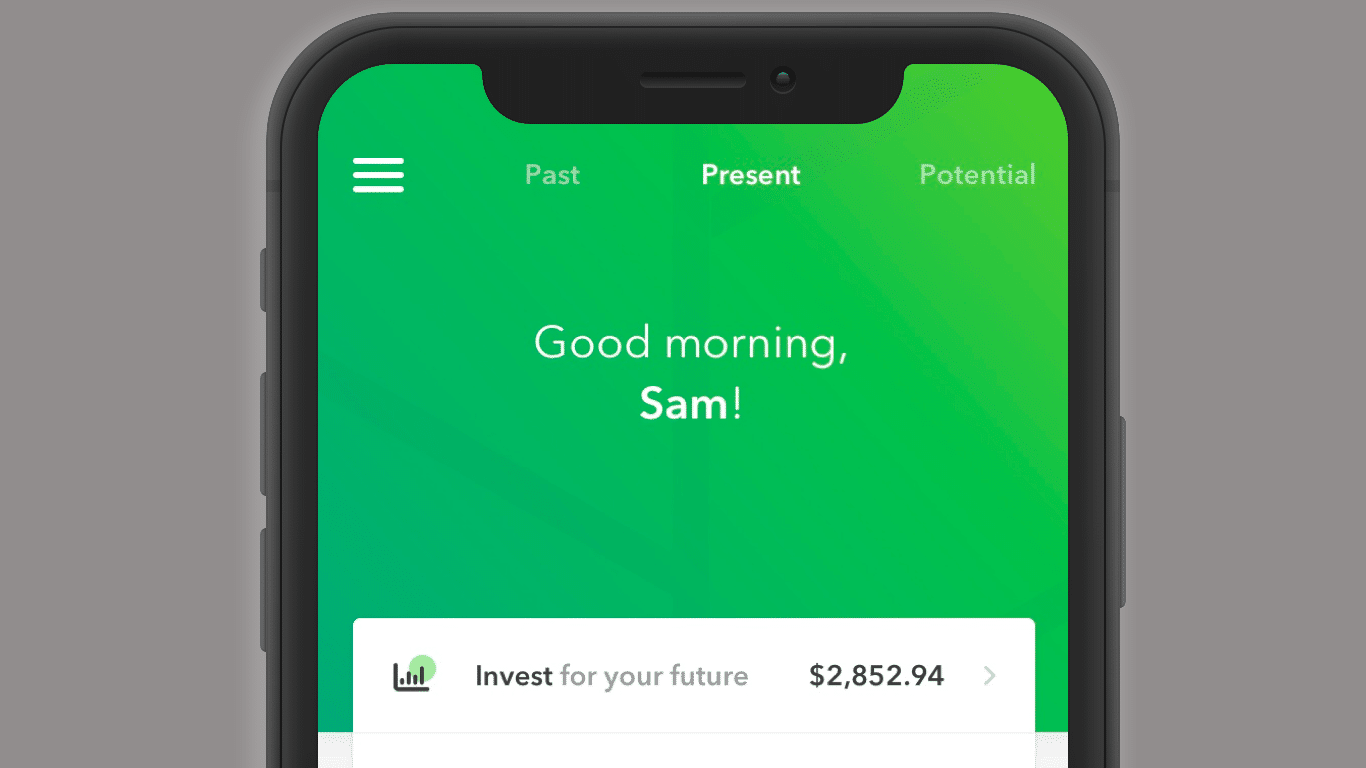

Acorns

Acorns has a beautiful mobile app and a beautiful website. It’s one of the best-designed apps on my phone by a long shot. I’m, of course, not the only one to notice this – they’ve won some sort of design award nearly every year since they opened their doors.

This Round was just going to be called Ease of Use, but Acorns elevated it to Aesthetic Appeal. I’m willing to bet this is the most significant way they get people to try them out. Stunning screenshots.

A beautiful interface can also be a downside, though. We’re all about investing for the long-term here, so if you keep opening your app just to see the beauty, you’ll also see daily price fluctuations and go slowly insane. That said, we still love beautiful things.

These screenshots play into Acorns ease of use as their app screams hours of OCD design discussions. From adding your checking account (see: Round-Up account later in the article) to selecting your risk tolerance – they make it all very easy. It’s important to note that while I only put up screenshots of their app, their website is equally pleasant to view.

Acorns Mobile App

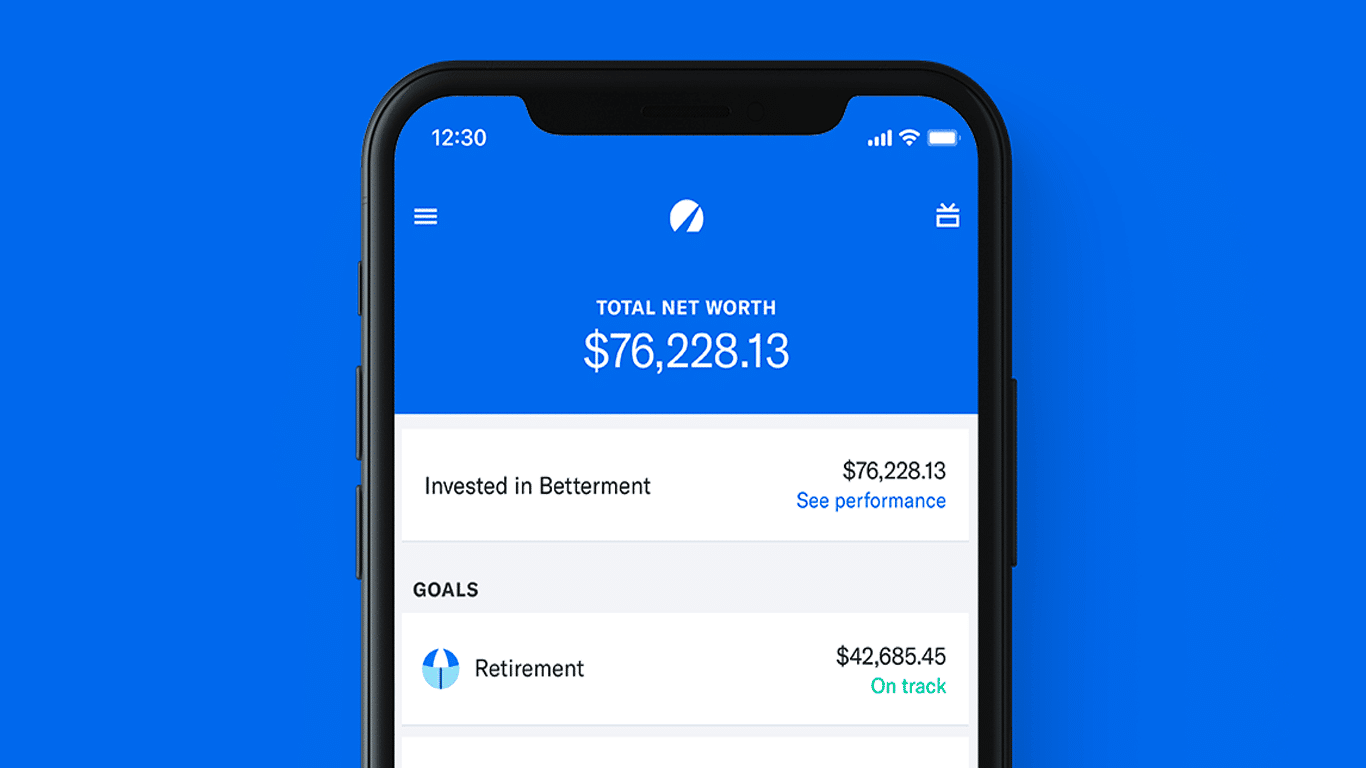

Betterment Mobile App

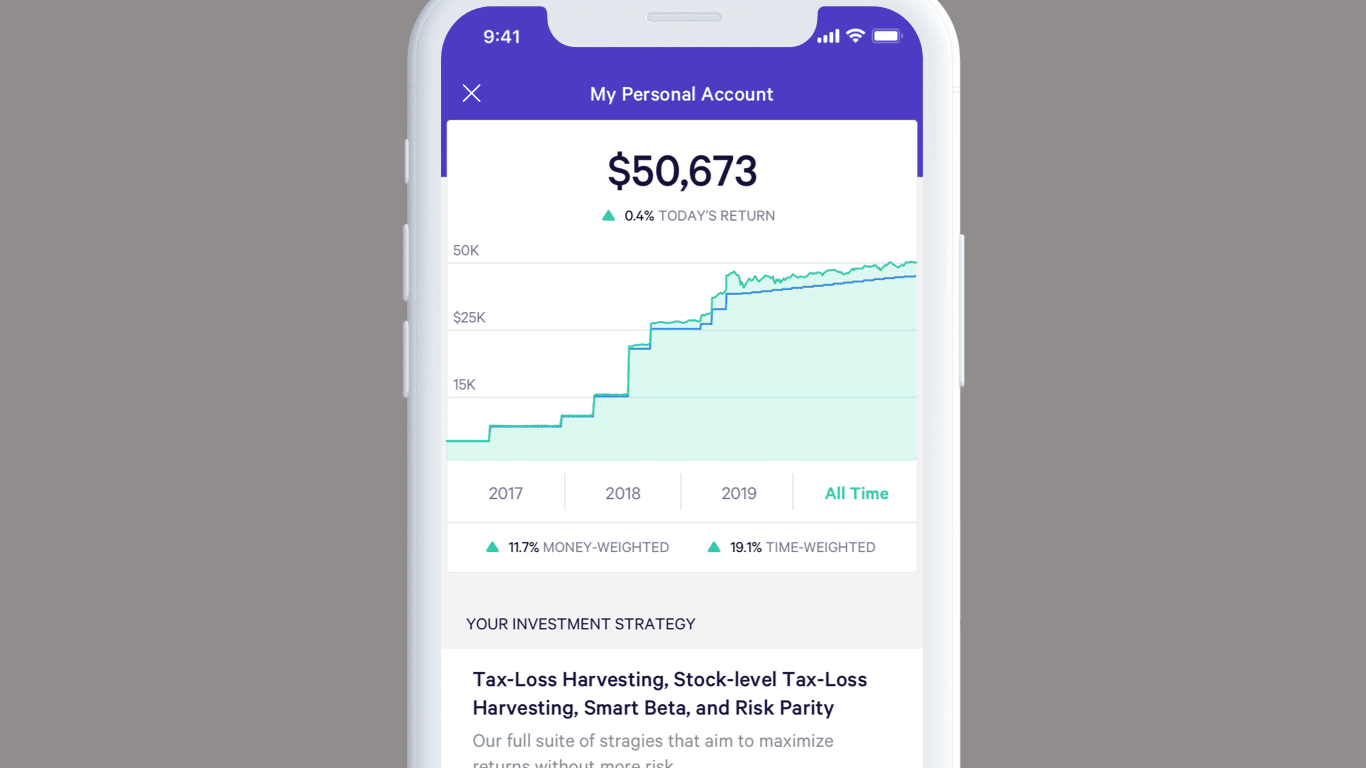

Wealthfront Mobile App

Betterment

Now, don’t get me wrong, there is beauty in simplicity, and this area

They’ve spent hours deciding what to remove from the app and how to tweak the wording to elicit “better behavior” from their customers.

For example, during a market downturn, people tend to act irrationally and sell (you’re supposed to sell high, not low). By conveying the tax implications when you attempt to withdraw, they’re able to keep more people doing the right thing. One point for transparency!

Wealthfront

Wealthfront has come quite a long way since we first wrote this review back in 2014. They’ve been through at least two complete redesigns and have substantially closed the gap.

While their app looks amazing, all you need to do is compare and read the reviews of Wealthfront vs. Acorns and Wealthfront vs.

Acorns and

Summary

Acorns and

Editor's Note

ROUND WINNER: Acorns. Both Acorns and

Fiscal flexibility that’s funny, free and delivered weekly.

Round 2: Investing Methodology

Perhaps the biggest question I had when I first started was, why I should invest with either service? Before any of the Robo-Advisors existed, I just picked the best low-cost Vanguard funds I could find and parked my money there.

And while all three companies use funds from industry leaders including Vanguard, Charles Schwab, and Blackrock, it wasn’t until I learned how they invested that got me hooked.

Acorns

While both

Acorns has 7 ETF’s (exchange-traded funds) that they will invest you in, depending on the risk level you select:

- Large Company – VOO

- Small Company – VB

- Developed Market – VEA

- Emerging Market – VWO

- Real Estate – VNQ

- Corporate Bond – LQD

- Government Bond – SHY

Every portfolio gains you exposure to bonds, US stocks, and foreign stocks. That said, this is about as much as you’ll find from Acorns on how they do things. I get that most people don’t care to know the details, but what about the people who do?

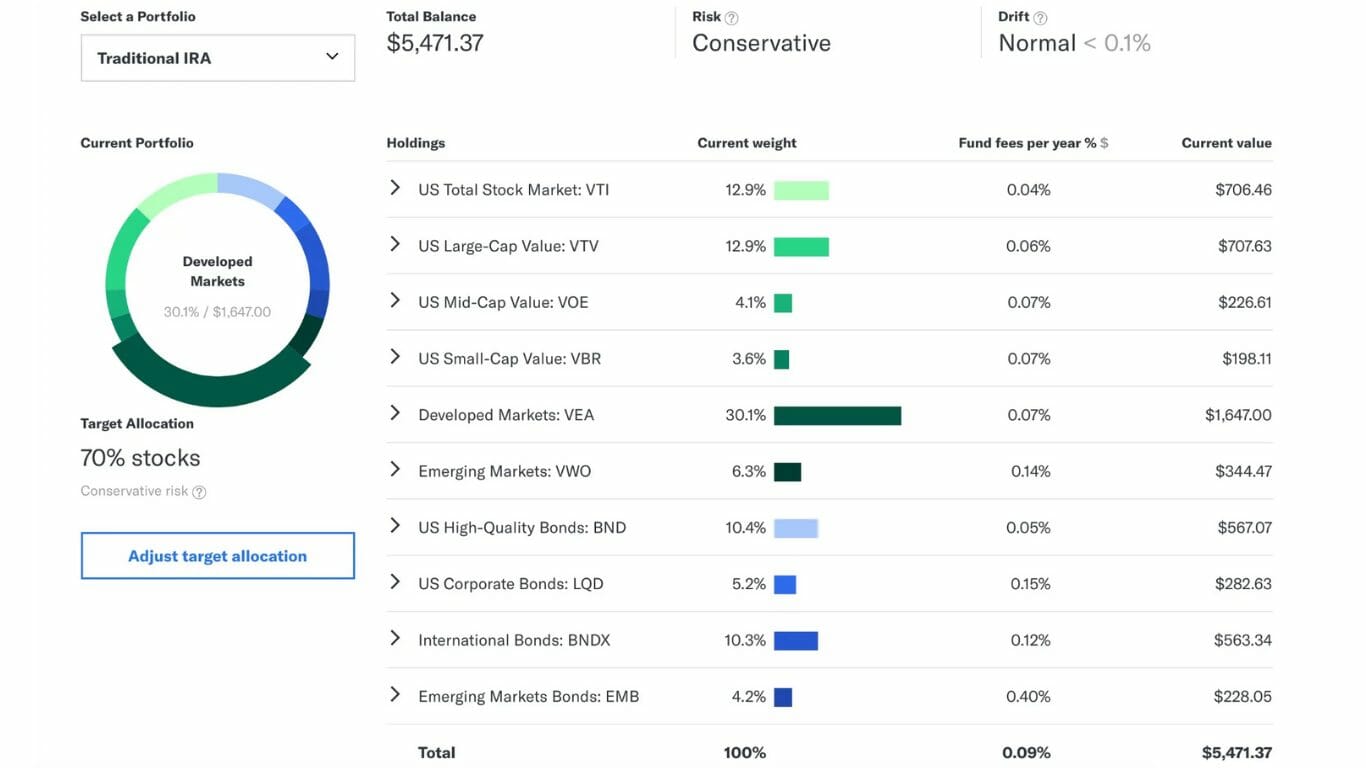

Betterment

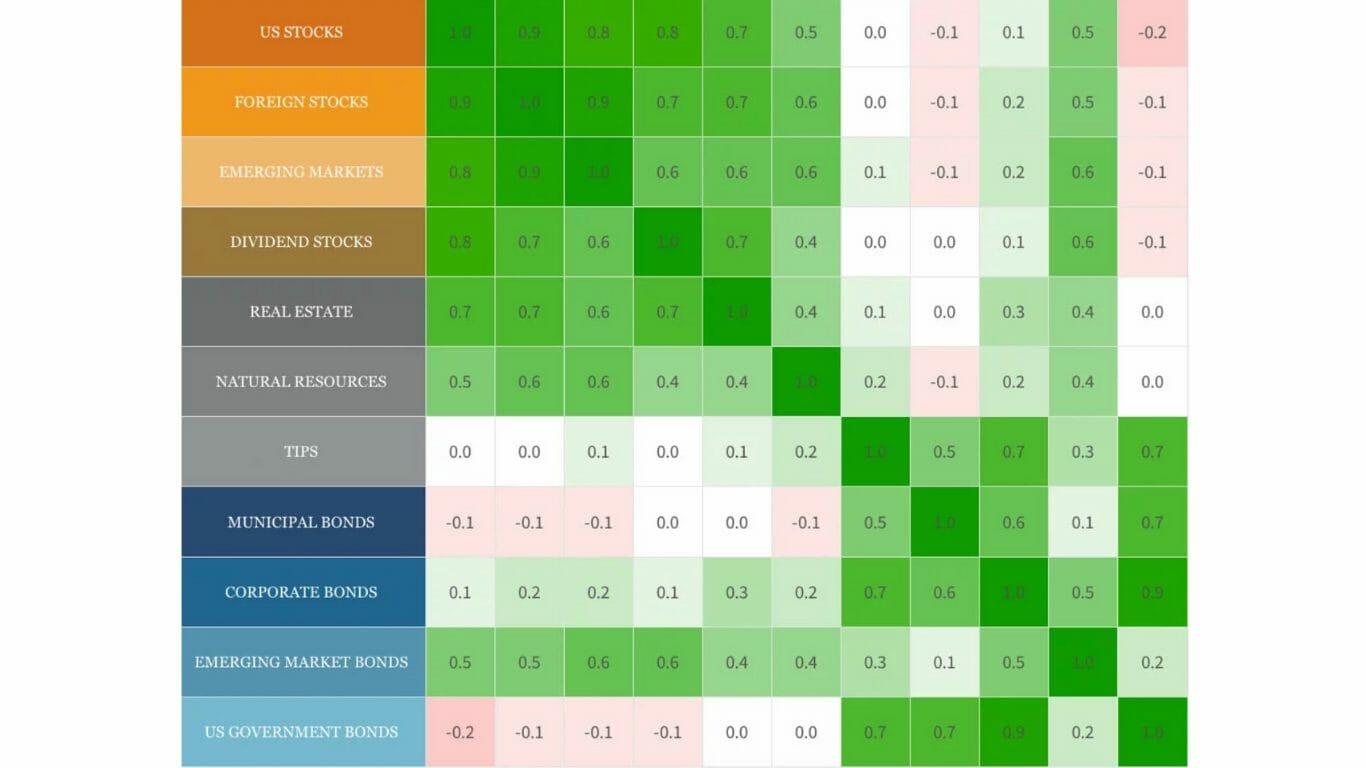

In addition to giving you an exhaustive 3,386-word white paper entitled “Our Investment Selection Methodology,” they provide you with interactive graphs and charts in every conceivable form of asset allocation.

It seems that not only do they want to share every nuance of their decisions, but they also spent a considerable amount of time, making it easy to digest and enjoyable to discover.

Betterment made a very conscious decision to treat me like an adult. It feels like there is nothing to hide; all their cards are on the table. With all the attention to detail around educating me, it makes me think about how much attention to detail is baked into their product.

Their investment portfolios maximize your return depending on risk tolerance and allocate your money across asset classes with fractional shares.

Betterment has, and Acorns doesn’t:

- US Total Stock Market – VTI, SCHB, and ITOT

- US Large-Cap Value Stocks – VTV, SCHV, and IVE

- US Mid-Cap Value Stocks – VOE, IJJ, and IWS

- US Small-Cap Value Stocks – VBR, IJS, and IWN

- International Developed Stocks – VEA, IEFA, and SCHF

- Emerging Market Stocks – VWO, SCHE, and IEMG

- Short-Term Treasuries – SHV

- Short-Term Investment-Grade Bonds – NEAR

- Inflation-Protected Bonds – VTIP

- US Municipal Bonds – MUB and TFI

- US High-Quality Bonds – AGG and BND

- US High-Yield Corporate Bonds – HYLB, JNK, and HYG

- International Developed Bonds – BNDX

- International Emerging Market Bonds – EMB, PCY, and VWOB

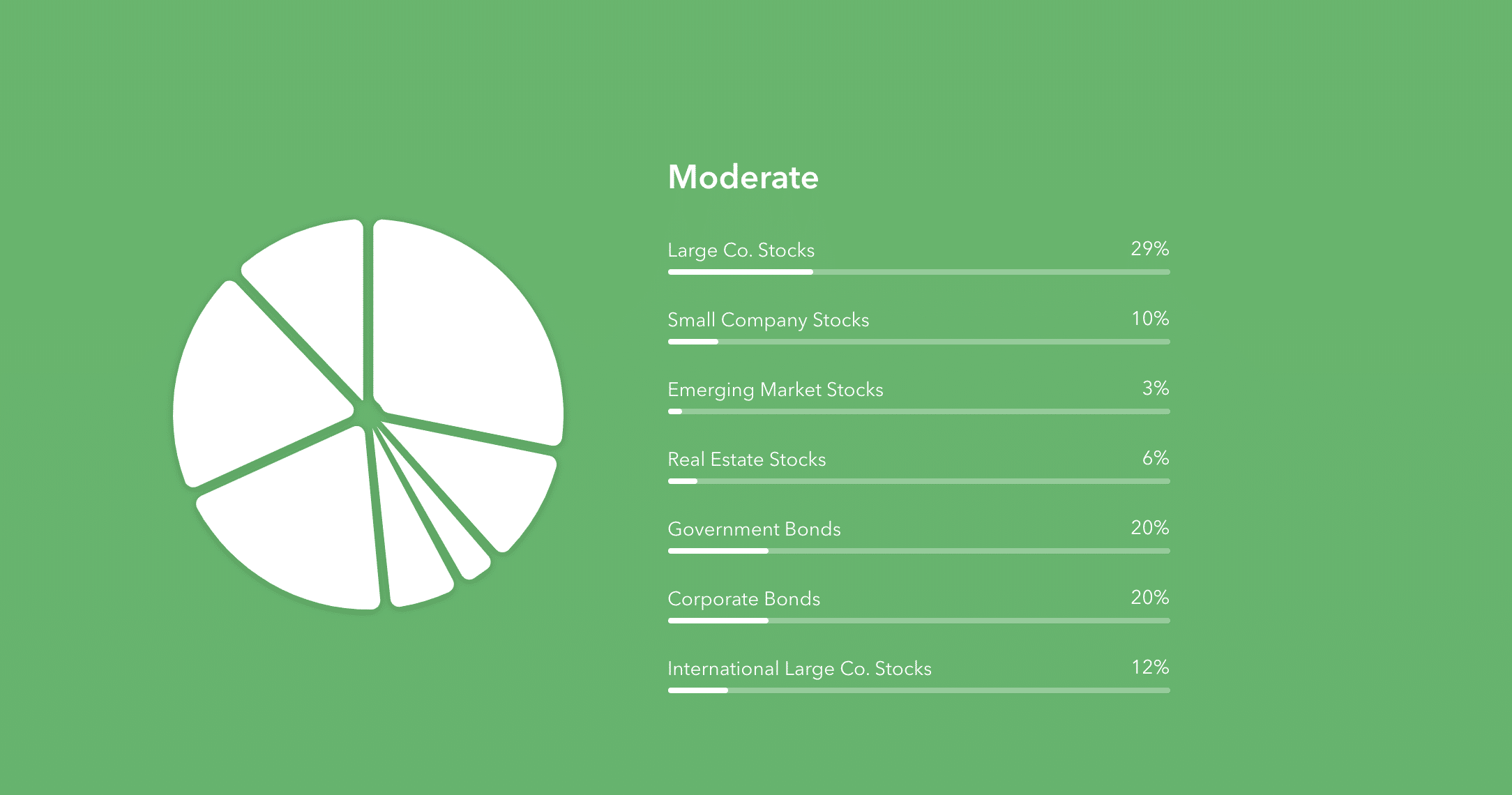

Wealthfront

Wealthfront’s Chief Investment Officer has a reputation that precedes him. Burton Malkiel was a director at Vanguard for 28 years, served on the Council of Economic Advisers, was president of the American Finance Association, was dean of Yale School of Management, and wrote the acclaimed book A Random Walk Down Wall Street that’s sold over 1.5 million copies. If the guy never slept a night in his life, I wouldn’t be surprised.

Their Investment Methodology white paper is undoubtedly very nerdy and includes plenty of charts and graphs.

I found it impressive that they shared their expectations as compared to other industry standards as well as their expected standard deviation of those results. Sufficiently nerdy with enough references and citations to make your favorite librarian proud.

Wealthfront’s diversified portfolio spans across 18 ETF’s and nine asset classes. While still crushing Acorns, there is less asset class diversification compared to what’s inside a

- US Total Stock Market – VTI and SCHB

- International Developed Stocks – VEA and SCHF

- Emerging Market Stocks – VWO and IEMG

- Real Estate – VNQ and SCHH

- Natural Resources – XLE and VDE

- US Government Bonds – BND and BIV

- Inflation-Protected Bonds – SCHP and VTIP

- US Municipal Bonds – VTEB and TFI

- Dividend Stocks – VIG and SCHD

This is coming after my less than favorable impression of Wealthfront’s interface. It restored a lot of confidence but, when you compare it to

I learn through interaction, and I was able to gather more from

Editor's Note

ROUND WINNER: Betterment. They made better choices, went the extra mile to educate their customers, and weren’t afraid to put it all out there.

Round 3: Advanced Features

Why invest in either

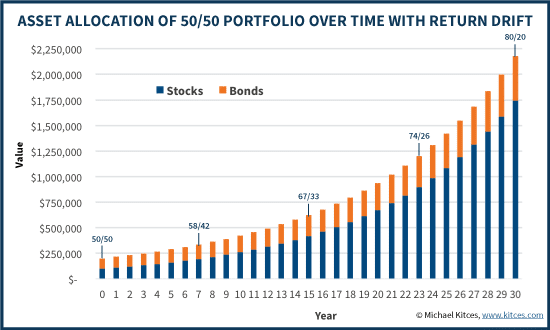

The first advanced feature is automatic rebalancing, a solution also known as Drift.

Drift is what happens to your portfolio over time as some investments grow faster than others. Since the past is no indication of the future, it’s vital to rebalance your portfolio.

It also helps significantly reduce risk. If in year one you think you’re at a 50% risk level, it better stay on that path. Both services protect you from risk while remaining tax-efficient.

One problem with trying to mirror what

Automatic Rebalancing and Zero Transaction Fees is where the feature similarity ends. Each service has one killer feature that distinguishes it from the pack.

Acorns Round-Ups

Acorn’s core feature is Round-Ups. The idea is that you link your checking accounts and credit cards to Acorns, and they will round every transaction up to the nearest dollar and invest it. Spent $5.06 at Starbucks? You’ve just invested $0.94.

All these small Acorns start to add up, and before you know it, you’re saving and investing. This is perfect for the person who has trouble saving.

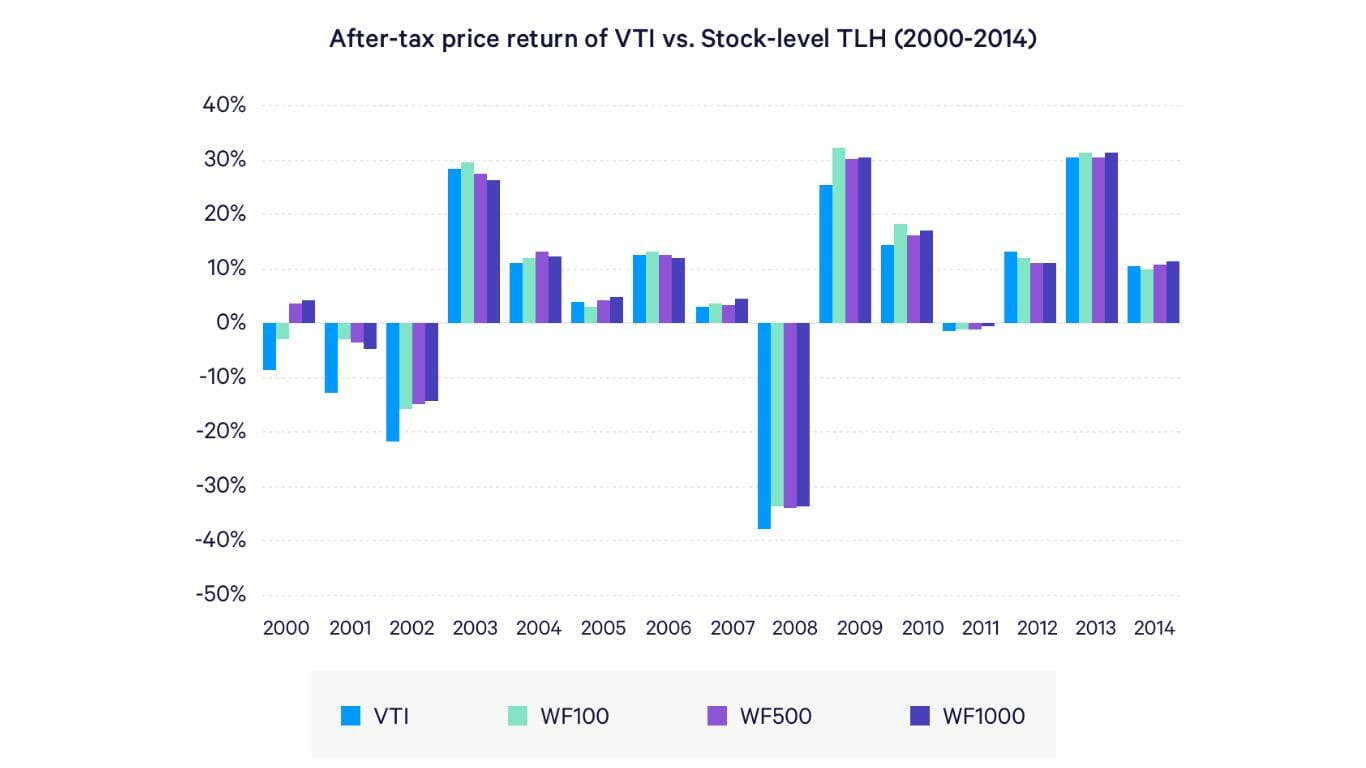

Wealthfront Stock-Level Tax-Loss Harvesting

Wealthfront and

Wealthfront was first to market here, but the service is practically identical.

Without going too deep, and with brilliant behind the scenes work, both

With TLH, you can expect to increase your overall market gains by 0.99% or pay 14.01% in taxes. So, for every $1,000 you invest, you can gain up to $10 more in tax savings.

Acorns investment strategy doesn’t include Tax Loss Harvesting. If you expect to earn more now than in retirement, Tax Loss Harvesting can be very beneficial, bringing significant gains to your portfolio.

Wealthfront now offers an enhanced form of tax-loss harvesting for taxable account balances between $100K and $500K, Stock-Level Tax-Loss Harvesting, that looks for movements in individual stocks, harvesting more losses and further reducing your tax bill.

With features like Stock-Level Tax-Loss Harvesting, you stand to make a lot more through economies of scale than you would below that price threshold.

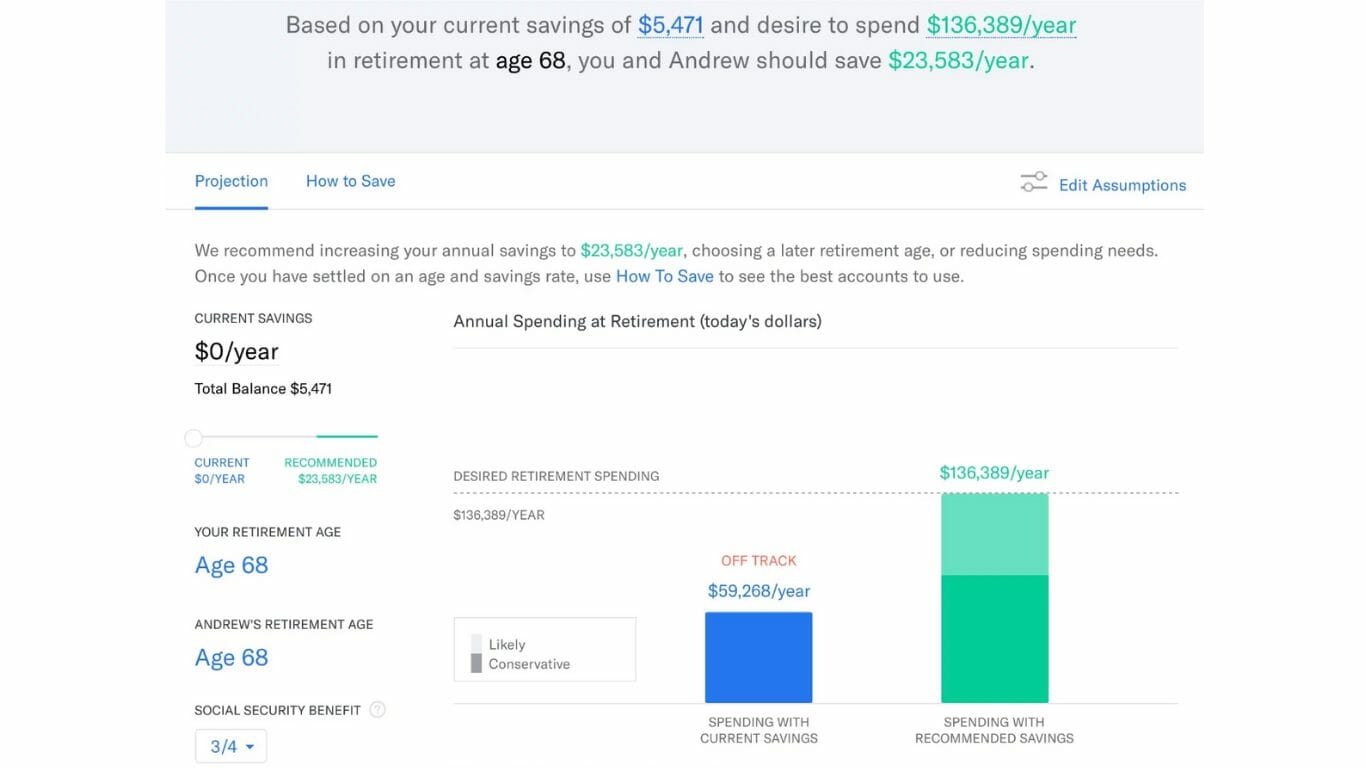

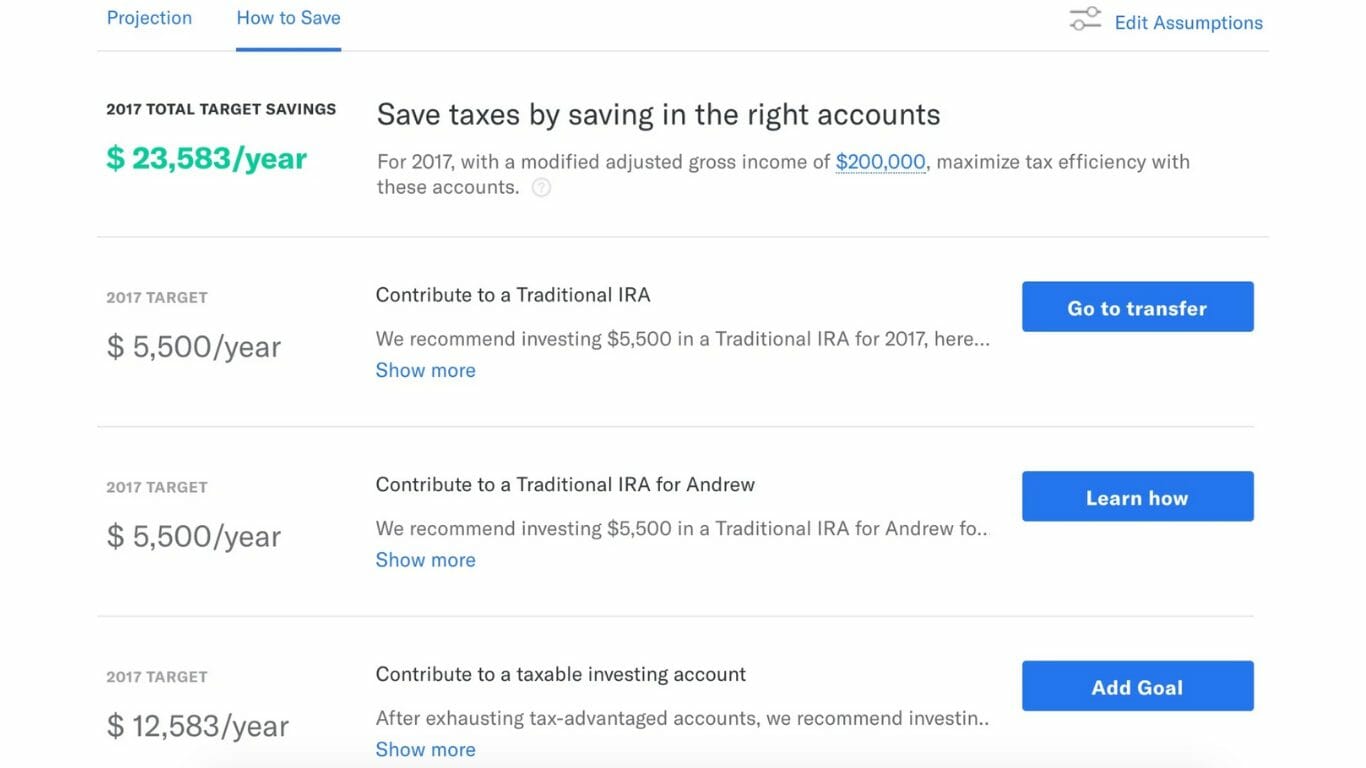

Betterment’s Retirement Planning Suite

Betterment set the bar very, very high.

They cover the basics like “how much do you make” and “when do you want to retire,” but every retirement calculator you’ve ever used does that. That’s the price of entry. What impressed me is how they account for things like existing assets, the cost of living, and how much income is needed during retirement.

For example, if I lived in Ames, Iowa (zip: 50010) like Thomas,

Therefore I’ve got to save an epic amount more if I want to continue living here AND retire here. Having

Good calculators give you the answer; great calculators make you think. This is a great calculator.

Editor's Note

ROUND WINNER: Betterment narrowly wins here. While Wealthfront’s Direct Indexing is amazing, you need to have $100k with them to take advantage, which rules out almost everyone.

Note: Round-Up by Acorns is a novel idea and perfect for the non-savers, but it won’t exactly make me more money. I want my money to grow faster automatically, and TLH does that. Couple that with RetireGuide, and you have a platform I can get behind.

Robo-Advisor?

FINAL WINNER:

Betterment is the best platform for the average investor. There’s no account minimum, and no minimum deposit, and you can get up to one year managed for free.

They’ve focused on providing a smarter, well-rounded platform. We receive frequent emails regarding retirement planning, so any financial advisor should make a priority to give good personalized financial advice.

The Smart Deposit feature automatically invests any excess cash in your bank account to makes it easy to start building wealth automatically.

Acorns is a fresh addition to the

Wealthfront is a sizable step up from Acorns in what it provides to its customers. However, their biggest advantage is Direct Indexing.

However, it caters to the high net worth investor.

Both

Acorns is great for students and people who can only invest what’s found in their couch cushions. Investing the “spare change” of your monthly expenses is a good idea in theory but generally doesn’t amount to much.

The average American makes 59 transactions a month. If each one ended in $0.01, then the average American would invest $58.41 a month with Acorns. Not enough for most people to retire on.

If you invest more, the Acorns platform is reliable, but it won’t blow your mind. Of course,

Get a Deal on Your Robo-Advisor of Choice

We’ve spoken with the CEOs of all three companies. We even got schooled on Opportunity Cost with Dan Egan, the head of Behavioral Finance and Investments at

As a result, we were able to capture some deals if you join one of these Robo-Advisors through us.

Fiscal flexibility that’s funny, free and delivered weekly.

Current Project: Making bloggers money with Lasso.