If you’re a homeowner, you’ve probably asked yourself this question multiple times, “Should I pay off my mortgage?”

For most people, their mortgage is their biggest debt. And we all know that debt is bad. Debt is an emergency that we must pay off as soon as possible.

But is all debt bad? Is paying off your mortgage quickly a good personal finance strategy? Paying off your mortgage early has both advantages and disadvantages. Let’s explore what those are.

Is Paying off a Mortgage a Good Idea?

We get a lot of emails asking about paying off mortgages early and people site various reasons for wanting to do so. A lot of people want to join the FIRE movement. They want to quit their jobs, retire much earlier than the typical retirement age of 65, and sometimes start a business with their extra money and time.

Perhaps Mr. Money Mustache is the God Father of the FIRE movement or at least its most famous proponent. He paid his mortgage off years ago and while it’s not the only reason he is able to live on something like $30,000 a year, it is a major component.

Some people, a lot of those who follow Dave Ramsey, only want to be debt-free and the idea of having any debt hanging over their heads is non-negotiable. A mortgage is the biggest source of debt for most.

There are some homeowners who have a bad interest rate and want to save as much money as they can in a bad situation.

And then there are those lucky folks who just happen to have a lot of extra cash lying around and want to know if using it to pay off their mortgage faster is the best way to use it.

Yes, the idea of being mortgage free is seductive but before you decide anything, we want to show you how to pay off your mortgage strategically.

What Happens When You Pay off Your Mortgage?

Making a list of pros and cons is a good way to help you make any big decision so let’s take a look at the pros and cons of paying off your mortgage.

Pros

Paying off your mortgage greatly improves your monthly cash flow.

The median monthly mortgage payment for U.S. homeowners is $1,030 according to the latest American Housing Survey from the U.S. Census Bureau.

Sure you can save money by canceling subscription services and lowering your cell phone bill but if you really want to improve your cash flow, you have to go after the source of your biggest expense. No one would turn down an extra $1,000 a month and paying off your mortgage would give you that.

Given the current state of leadership, people are nervous about the economic and political climate. Uncertainty isn’t a condition that tempts people to invest their money in the stock market. There are no guaranteed returns no matter when you invest or what you invest in but you know what is a guaranteed return?

Paying off debt. Paying off debt is a sure-fire way to lock in a return on your cash.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

Is It Better to Pay off a Mortgage or Save Money?

Cons

Using money for paying off your mortgage will not perform as well over the long-term when compared to using that money for investing. But, what about the money I’ll save on interest? Take a look at this.

A $220,000 30 year mortgage at 4% interest on a $275,000 home. You’ll pay $158,000 in interest over the life of the loan.

Paying an additional $100 a month towards the mortgage principal will $28,000 in interest and 3 years on the loan. That same $100 a month invested over the same period of time with a 7% return (which is conservative) will earn you nearly $117,000.

Hmmm. Save $28,000 or make $117,000? We prefer a better rate of return!

It’s also wise to sock away money into a savings account like your emergency fund or retirement savings (Traditional IRA, Roth), instead of making extra payments on a mortgage – especially if you haven’t started building one yet.

The two most expensive things in life are interest and taxes. We showed that paying off your mortgage early doesn’t save you as much in interest as you can make investing but what about taxes?

If you pay off your mortgage early, you lose a significant tax deduction. $750,000 a year in mortgage interest is tax-deductible for couples while individuals can deduct up to $375,000.

These deductions reduce your taxable income by the amount of interest you pay. If your tax rate is 30%, it technically means your mortgage interest is 30% cheaper because it’s pre-tax.

Paying Off Your Mortgage Strategically

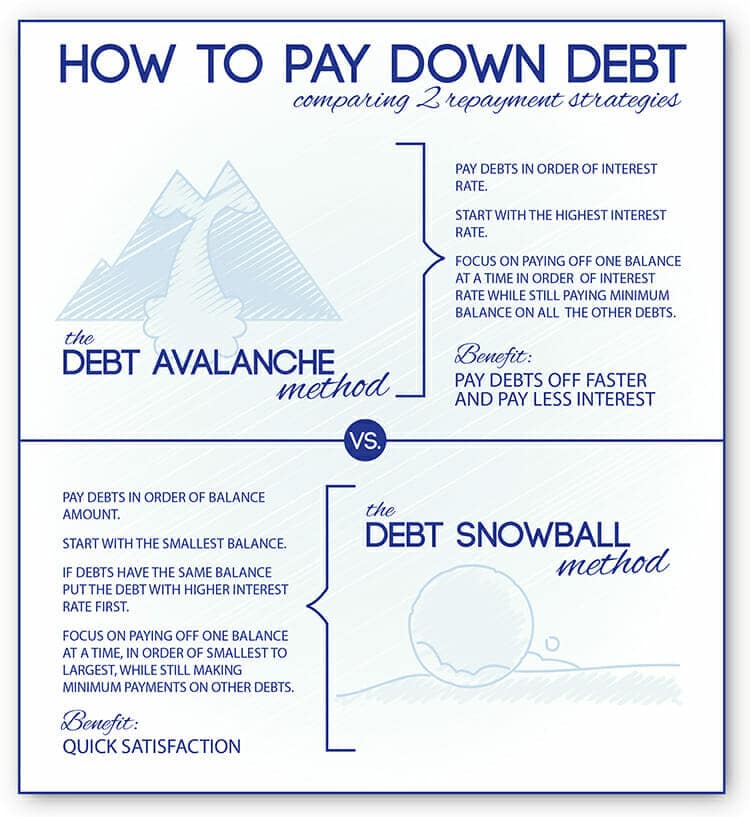

For the same reason we use the snowball or stacking method to pay off credit card debt, because being strategic accelerates the process and saves money when compared to just throwing extra money at the cards willy nilly, if you’re going to pay off your mortgage, you have to do it strategically. Here are some strategies you can use.

We’re using the same numbers we used in our above example.

A $220,000 30 year mortgage at 4% interest on a $275,000 home. You’ll pay $158,000 in interest over the life of the loan.

Is It Smart to Pay Extra Principal on a Mortgage?

Quarterly Additional Payment: By making one extra mortgage payment every three months, you’ll pay off your mortgage eleven years early and save more than $65,000 in interest over the life of the loan.

Extra $20 Per Month: An extra $20 per month towards the principal will shave off 1 year off your loan and save $7,000 in interest.

Extra $100 Per Month: An extra $100 per month towards the principal will shave off 3 years off your loan and save $28,000 in interest.

Paying a little extra on your mortgage each month is a strategy not dissimilar to the Golden Butterfly Portfolio strategy of investing. You’re not tying up a lot of money into paying extra on your mortgage, you’re paying a little while doing other things with the rest of your money.

Maybe maxing out your retirement accounts, saving some money to buy a rental property, and holding back some cash for an opportunity fund. “Small” amounts of money (small being relative to each of us) spread out across a few different areas.

Reduce What’s Required

This is banker talk for refinancing your mortgage. Let’s use a real example. Should Matt refinance the mortgage on his much-hated condo?

The condo was purchased for $180,000 and according to Zillow, is now worth $135,000. He has $130,000 and 20 years left on a 30-year mortgage at 4.5%. The monthly payment including taxes is $1,300, there is a $166 HOA fee and $125 property management fee, both paid monthly. The condo is rented out for $1,490 per month.

Reducing your interest rate is a good thing but a refinance can reduce your monthly payment which is not necessarily a good thing. A lower payment can be the result of extending the life of your loan which means you’ll pay even more in interest. It increases monthly cash flow – which is a good thing right?

It depends on what you do with the extra money. Will you invest it? Great, a refinance may be worth it. Are you going to buy a bunch of crap you don’t need with it? Well, you’ll pay more in interest and have nothing to show for it. Bad idea.

But Matt’s condo is an income-generating piece of real estate (rental property) so that makes things a little different. A

Refinancing a mortgage isn’t free so take closing costs into account when deciding whether or not to do it. How long will it take for the refi to pay for itself?

Refinancing generally costs 3%-6% of the loan’s principal. Because it’s considered a new mortgage, it requires an appraisal, title search, and application fees. If your closing costs $5,000 and it saves you $200 a month, it will take 25 months to break even.

Refinancing generally makes the most sense later in the mortgage when payments are mostly going to principal rather than interest.

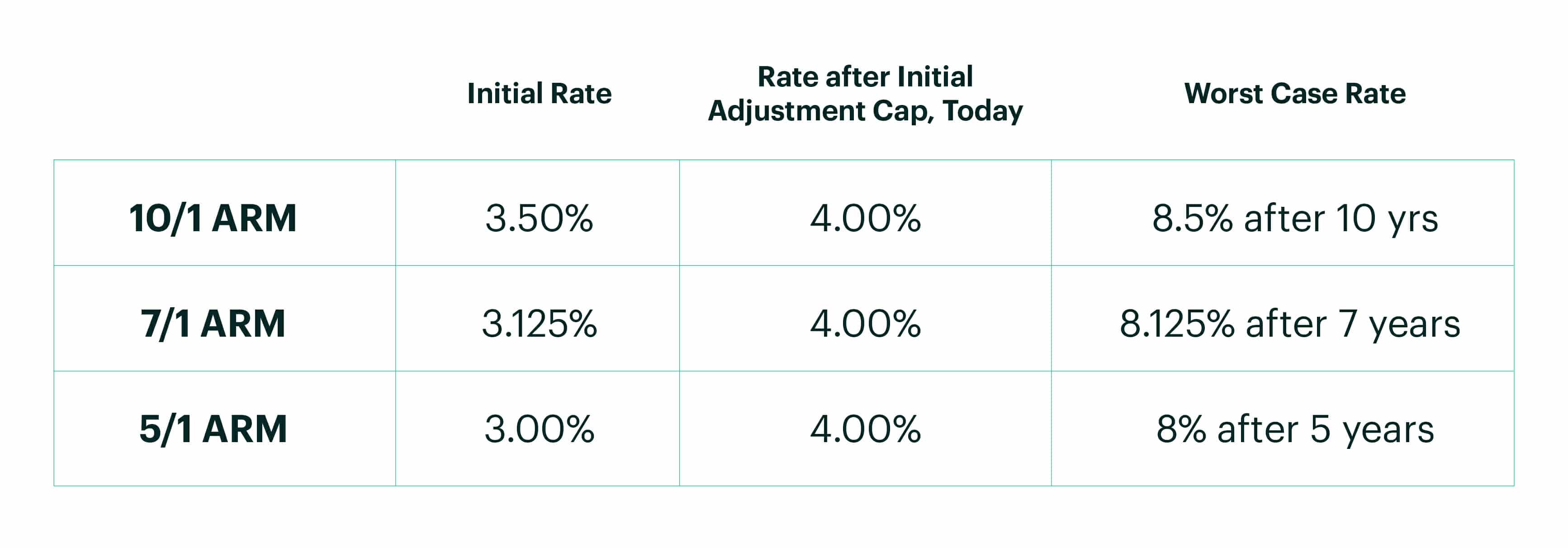

The 7/1 ARM Strategy

This was the financial decision Andrew and Laura made. They knew they weren’t staying in this house for 30 years. Their goal was to get the lowest mortgage interest rate possible. They found a 3.25% rate through Wells Fargo by taking out a 7/1 adjustable rate mortgage.

The 7 means they have a fixed rate mortgage for the first 7 years. After the first 7 years, the rate can increase once each year, the increase is capped at 1%. Andrew did a ton of historic research on interest rates and found almost no cases of the rate reaching the cap.

Because they don’t plan to stay in the home for seven years, this strategy isn’t risky. But what if they do stay and the rate goes up, all the way to the cap? Simple. They’d just refinance to another 7/1.

HELOC Strategy

HELOC is a home equity line of credit. Different from a home loan where you get a lump sum, HELOC’s work with a revolving credit line.

A HELOC will work and you can use it to pay down your mortgage in a third of the time, saving thousands on interest but it’s a constant juggling act between your credit cards and the HELOC because all of your money goes into the HELOC to pay your mortgage.

In select months, you use your entire paycheck to pay your mortgage and put all of your expenses on a credit card with at least a 45 day grace period.

At the end of the grace period, you transfer your credit card balance to the HELOC. With the next paycheck, you pay off your HELOC balance instead of paying your mortgage. The next paycheck is used to pay your mortgage. Rinse and repeat.

Financial Goals Will Decide for You

Will paying off your mortgage early bring you peace of mind?

Check the loan terms. What’s the mortgage rate? Can you direct any extra payments to the principal and not the interest? If not, don’t do it. Is there a prepayment penalty? If there is a penalty, will it cost more than you could save with early repayment?

Run the numbers with a mortgage payoff calculator.

In uncertain times, paying off your mortgage early is a way to get a guaranteed return. We still don’t think you should plow all of your money into early repayment while investing nothing; the opportunity cost is too great.

Typically you’ll get higher returns from the stock market, but putting some extra money towards paying off your mortgage early is a good hedge in volatile times.

The market always does what it's supposed to do only never when it's supposed to do it.

Tweet ThisHow close are you to retirement? The closer you are, the shorter your time horizon for investing because your money has fewer years to ride out market volatility. If you’re getting close, the money you use for paying off your mortgage faster is a guaranteed return.

How far into your 30-year mortgage are you? If you’re 10 years or fewer in, all your extra money may be going towards interest payments and not principal so it doesn’t make sense to pay extra.

How’s your financial situation? If you have other high-interest debt in the shape of credit cards, personal loans or car loans, consider paying that down first.

Paying off your mortgage early can be a good financial strategy. When you do it strategically.

Show Notes

Peachy Bones: An India Pale Ale

Jam Skate: A Double IPA

![Home Equity Loans: Requirements, HELOCs, and Securing One [UPDATED]](https://www.listenmoneymatters.com/wp-content/uploads/2019/02/home-equity-loans-768x432.png)