There are a lot of things that deserve your energy but paying off debt isn’t one of them. If you have debt, it can feel hopeless. But you can get out of debt, and it’s easier than you think. We can show you how to be lazy and pay off your debt.

An All-Time Record

If you have debt, you’re not alone.

Total household debt—a category that includes mortgages, student loans, and car loans along with credit card and other debt—dipped in the wake of the Great Recession, but it has since steadily rebounded in the years since.

Overall, Americans’ debt hit a new high of $13 trillion last year, surpassing the previous record set in 2008 by $280 billion, according to the New York Fed.”

Not all debt is the same. Mortgage debt, for instance, is typically low-interest debt and a home can be an investment. It’s the other kinds of debt, credit cards, and student loans, that can hinder all of your long-term financial goals.

So let’s tackle that kind of debt once and for all, and be lazy while we do it.

Get A Repayment Plan

Paying off debt is a process, and there are several steps. These steps can take a while to accomplish. But until you do, it’s incredibly difficult to save money for your future.

You might get 85 years on this planet, don't spend 65 paying off a lifestyle you can't afford.

Tweet ThisYou didn’t accumulate this debt overnight, and you’re not going to pay it overnight.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

Determine the Total Amount

It’s terrifying to sit down and total up just how much debt you’re in, but that is the first step if you want to pay off your debt. Make a list of all of your outstanding debts and the interest rate on each. The best way to see all of your debt is in your Credit Karma account.

Not only will you see all of the debts but you’ll be able to see your credit report and credit score too. It’s free to make an account so do that now if you don’t already have one.

Go through your credit report and make sure all of the listed debts are legitimate. There are a variety of reasons debts that aren’t your’s can end up on a report. If you find debts that are not yours, you can dispute them.

Consult Your Budget Before Making Debt Payments

What’s that? Don’t you have a budget? Well, go to Personal Captial and get a good overall picture of your finances and your spending.

How much money do you have coming in compared to how much is going out?

Do you have any money that isn’t going out?

Your budget is going to identify the cash you can use to pay off your debt. You should be dedicating at least 20% of your income to paying off your debt.

Once you have a month’s worth of budget data, go through it with a fine-toothed comb. Where are your spending leaks?

Saving money is easier than making more money, so if you want to be lazy and pay off your debt, this is the best place to do it, by cutting your budget.

Let Trim find and cancel expenses like gym memberships you don’t use and subscription services you can’t afford when you have debt to pay off.

Let Billshark negotiate better rates for things like your cable and internet service. Every dollar you save is an extra dollar you have to pay off your debt more quickly.

Triage the Damage

Are you behind on any payments but not so far behind that they’ve been sent to collections? Those are the first debts you want to work on because once they go to collections, they will tank your credit score.

Call up those creditors and let them know you want to work out a plan to get current. There are entire departments dedicated to this.

These creditors wish to work with you because doing so makes them more money than they’ll get when they sell off your debt to a collection agency for pennies on the dollar.

Do you have any debts that have already been sent to collections? How old are they? If the debts are only a few years old, these are the ones you want to pay off first because of the damage they’re doing to your credit score.

You may be able to settle these debts for less than their dollar amount.

Creditors often just want to get deadbeat accounts off their books and getting something is better than getting nothing. Save up some cash and make an offer. Low ball and ask if they’ll accept 25% of the amount you owe in cash (in the form of a money order) to settle.

Not really good at negotiating? Don’t worry. Companies like National Debt Relief will do it for you.

They might say no, they might say yes, and they might make a counteroffer. Whatever happens, you won’t be any worse off than you are now, so it’s worth a shot.

If the debts are five or six years old, this is a judgment call. These debts will fall off your credit report after seven years and no longer impact your score.

What Debt Should Be Paid Off First

Now that you’ve dealt with the most urgent debts, you need to prioritize the others. There are two methods of debt repayment that will help you pay off debt more quickly and efficiently.

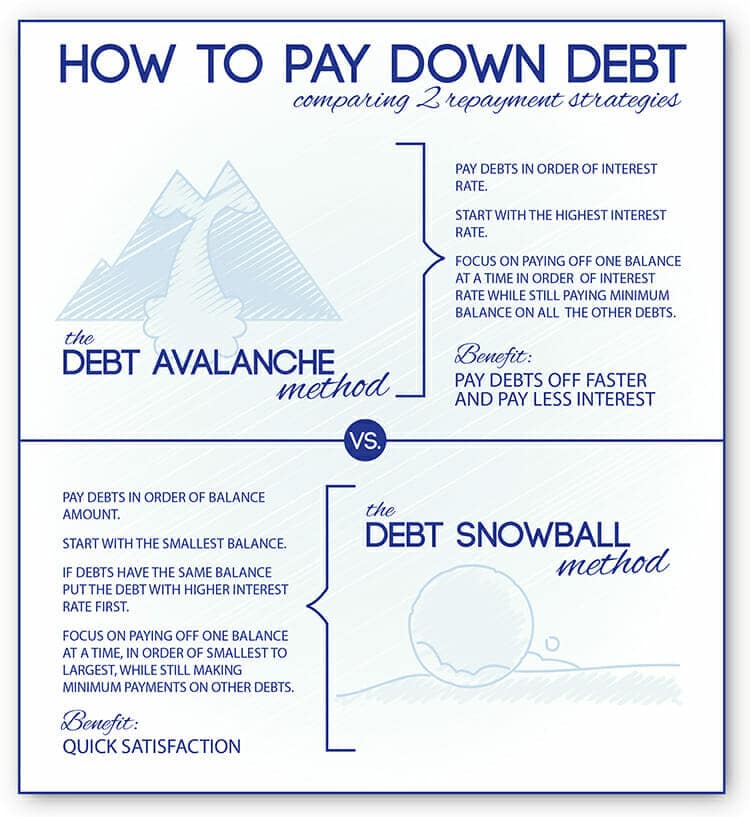

#1. The Debt Snowball Method

You prioritize the debts according to the dollar amount, least to most. You use every dollar you can spare to paying off the smallest debt while paying only the minimum payment on the rest.

When you pay the first debt off, you use the money you were paying on it along with every spare dollar to pay off the next in line while continuing the pay only the minimum payment on the others. So on and so on until all the debts are paid.

#2. The Stacking Method (aka Debt Avalanche)

You list the debts according to interest rate, highest to lowest. You use the same method described above to pay off the debt with the highest interest rate and then continue down the list.

Which Is Better?

The stacking method will save you the most money because it saves the most on interest.

That said, the snowball method can be more satisfying especially if you have a few debts that are for relatively small amounts. Killing off those little debts can be motivating and give you an extra boost to get the bigger ones paid off.

You could even use both methods. Start out using the snowball to get a few debts out of the way and a feeling of accomplishment and then switch to stacking, so you save more money on the remaining debts.

Get a Balance Transfer Credit Card

A balance transfer card is a credit card with a 0% APR introductory period. You can find cards with 0% interest for six to 24 months.

Go to Credit Karma to see a list of cards that you’re likely to be approved for based on your credit score. Each time you apply for a credit card, your credit score takes a little dip, so you don’t want to apply for cards you are unlikely to be approved for.

If you’re approved for one of these cards, you can transfer the balance from a high-interest card to the new card. The new card generally handles this for you, great for lazy people wanting to pay off debt!

During the 0% APR period, all of your payments go to paying off the principal because you aren’t accruing interest. Do not use this card to make new purchases. In fact, don’t use any card to make new purchases. You can’t pay off credit card debt if you’re continually adding to it.

You must do your best to pay off the entire balance before the introductory period ends. Any remaining balance will be subject to the new interest rate which may be higher than the rate on the old card.

Refinance the Debt

Another option for both credit card and student loan debt is to refinance it with a company like

Refinancing simply means taking out a new loan at a lower interest rate and using it to pay off the higher interest rate debt.

Lending Club is a peer-to-peer lender. Rather than going to a bank for a loan, you crowdfund the loan on

It also means you have a single monthly payment rather than paying off various credit cards each month. You’ve consolidated several debts into a single debt.

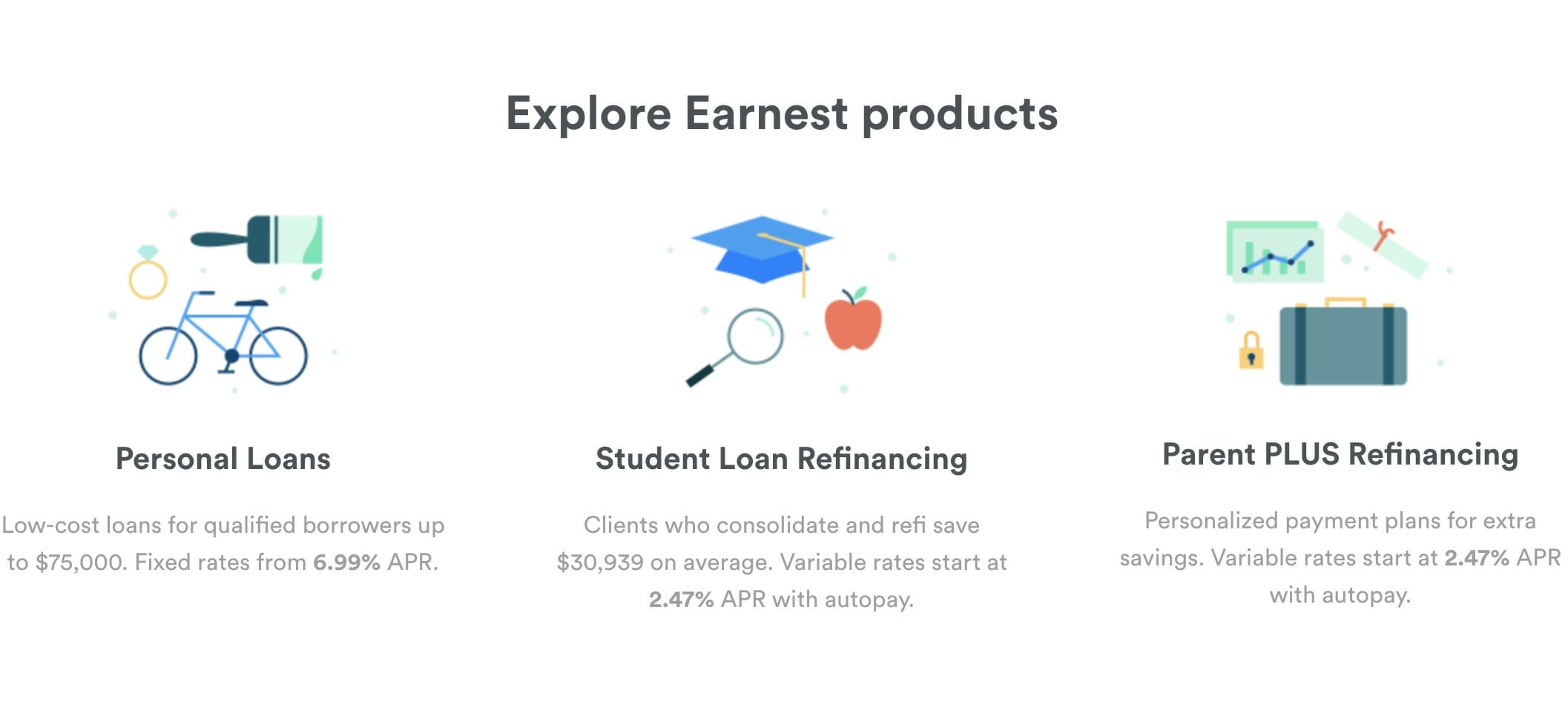

Earnest specializes in student loan refinancing. The average borrower saves an amazing $30,939 over the life of their loan when they refinance with Earnest. Imagine how much faster you could pay off your debt if there were $30,000 less of it!

Checking your rates on Earnest only takes two minutes and won’t affect your credit score.

Make More Money

Because your debt is an emergency, you want to pay it off as fast as you can. You’ve already made some money-saving cuts, and that’s great. But to really attack your debt, you need to make more money.

The money you make from your primary job is already budgeted, and part of it goes to necessary expenses like housing, utilities, and food. But the great thing about making extra money is that every dollar of that can be budgeted solely to pay off your debt.

The average American watches five hours of television a day, that’s almost another full-time job’s worth of hours.

So don’t tell us you don’t have time to make more money. We know some of you don’t watch that much television, but nearly everyone has at least a few hours a week they could dedicate to bringing in extra cash.

There are a ton of ways to make more money, and we’ve covered them in-depth. Spend a few hours a week driving for Uber or Lyft. Rent out your home on Airbnb a few weeks a year. Even if you don’t live in a typical tourist area, people might rent your home for things like sporting events, concerts, or parents’ weekends and graduations if you live in a college town.

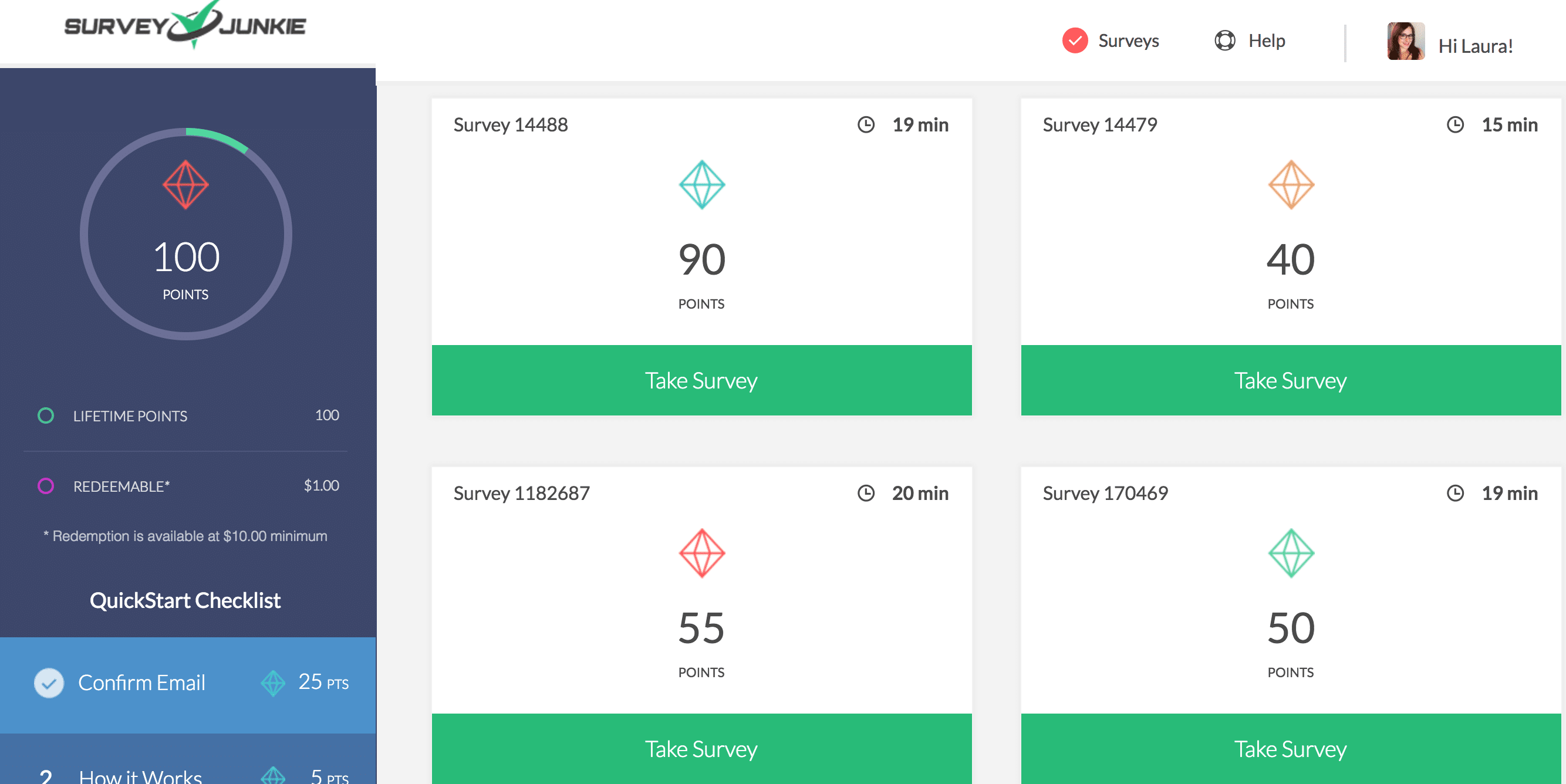

Even doing things like answering online surveys on a site like Survey Junkie or watching videos on Swagbucks can earn you a few dollars a week.

Ask your boss for a raise and go into his or her office armed with the reasons you deserve one. Start looking for a better paying job which typically gives you a much more significant income boost than a raise at your current job will.

Now What?

It took a while, but you did it, you paid off your debt, and it was easier than you thought when we started this process. Now that you have zero debt, what should you do with all your extra money?

Start Investing

Now comes the fun part! It’s fun to see the amount of debt you owe dwindle down to zero, but it’s more fun to see the money you make investing go up and up!

Your investing priority should be maxing out your retirement accounts. This money needs a long time to grow which is what retirement accounts are designed to provide, and they are tax-advantaged. The only thing more expensive than credit card interest is taxes, so we want to minimize both.

Start with your employer’s 401k if they offer one, especially if they’re offering to match. The match you get in a 401k is free money, and we never turn that down. Once you’ve maxed that out, move on to a Roth, Traditional or Roth, we’ve explained the finer points of each.

Next, explore

If you’re interested in dipping your toes into real estate investing, there are lazy ways to do that too! Fundrise lets you invest in real estate for as little as $500.

If you have considerably more than $500 and have considered being a landlord but don’t want all the responsibility for leaky sinks and deadbeat tenants, check out Roofstock.

It’s a turnkey

Listen to Dave Ramsey

We don’t agree with the Dave Ramsey philosophy on all things personal finance, but he does have good ideas about how to pay off your debt and what to do once you’re debt-free.

The first thing to do is to save up a good, healthy emergency fund. The reason you got into debt in the first place might be because you didn’t have an emergency fund.

An emergency fund is money set aside to pay for unexpected expenses like a car or home repair or a period of unemployment and you can save it in a high-interest savings account. When you don’t have this cushion, you fall back on credit cards, and the debt cycle starts.

Aim to have an emergency fund containing three to six months’ worth of essential expenses, the things you have to pay for like housing, food, insurance, a car payment, and groceries.

This amount is several thousand dollars so it’s another one of those personal finance things that won’t happen overnight.

But now that you aren’t paying out all that money on your debt, it will happen faster than you think. You should keep your emergency fund in your bank account, checking or savings. This money needs to be somewhere that is both safe and easily accessible.

Don’t Do It Again

Even when you pay off your debt the lazy way, it still takes some effort. But you paid it off, and you have a good credit score now. Don’t forget the lessons you’ve learned. Pay off your credit card balances in full every month. Keep your living expenses low. Whatever you were doing to bring in extra money, keep doing it.

Because being lazy and being debt-free is what we all want.