Millions of Americans struggle with the burden of credit cards. Credit card debt is an emergency that needs to be dealt with as quickly as possible. While there is no bad way to pay off credit card balances, there is a right way and a wrong way. Figuring out the best way can be tough, though. That’s where Tally comes in.

The average American has two bank-issued credit cards and carries a total balance of $5,551.

The average interest rate on a new credit card is 19.24% and 14.14% for existing accounts. If you make your monthly payment late, you’ll be charged a late fee. Credit card late fees range from $28 to around $36.

You can see the problem. Between the balance, the interest charges, and late fees, it can seem nearly impossible to get out from under credit card debt. You pay and pay every month, but the balances never seem to get any smaller. Being in credit card debt hell is stressful.

Debt can have grave consequences, not only for financial health but physical and mental health, too. Some 38% of people who have credit card debt say it has negatively affected their happiness. One third said it affected their standard of living and one in five said it even had a negative effect on their health.

When you’re paying off credit card debt, there are things you aren’t able to do. You can’t save an emergency fund, invest, or buy a home. Credit card debt is like an anchor holding you back from achieving your financial goals.

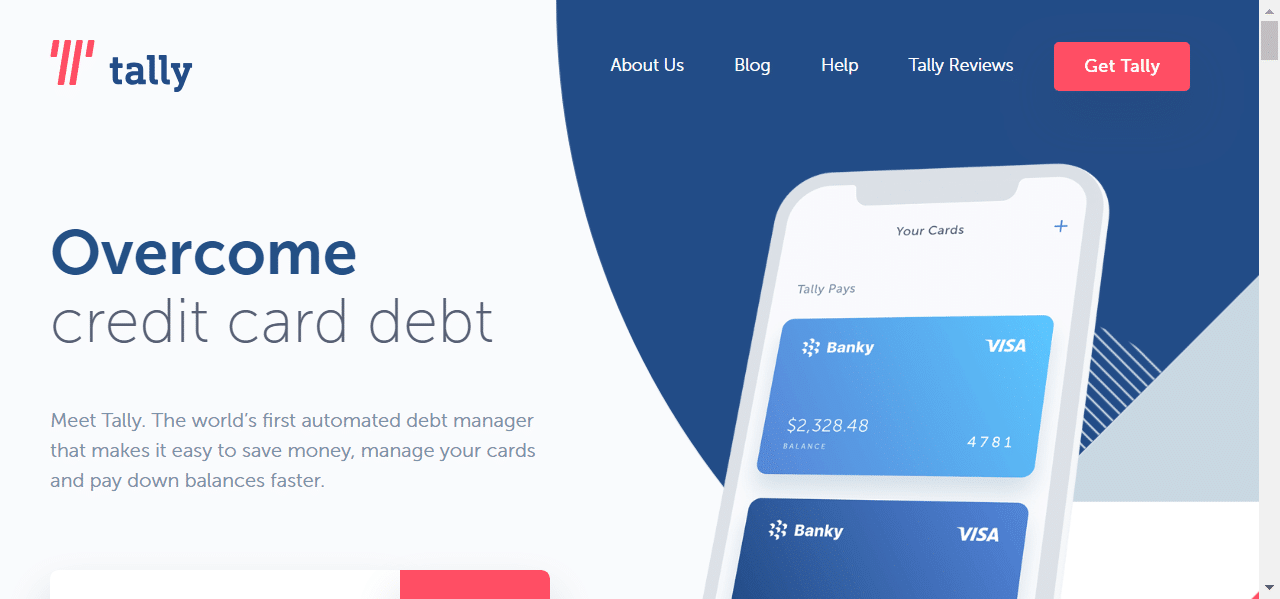

Tally is a new app that wants to help you pay off your credit card debt in a smarter way. Can the Tally app help you tackle your credit card debt once and for all? We did a Tally Review to find out.

What is Tally?

Tally is a mobile app for both iPhone and Android that extends a line of credit to approved members and uses that money to pay down credit card debt. Tally does more than that though. You can consider Tally your own personal debt manager.

Tally looks at your linked credit cards and finds the cards with the highest APR. Using the Tally line of credit with a lower APR, Tally pays down the higher interest card first. This method, the stacking method of debt repayment with the bonus of a line of credit, helps you save money and enables you to pay down your debt more quickly.

Tally can also take over the responsibility of making your credit card payments for you. If you’ve had a problem making at least the minimum payment on time, this feature will make sure you avoid late fees.

How Tally Works

Using Tally is like having a personal assistant who makes your credit card payments for you. Each month you make a payment to Tally and Tally uses that money and your Tally credit line to make your credit card payments at least two days before the due dates. Tally will prioritize paying your credit card with the highest interest rate first. For credit cards with a lower APR than the APR on your Tally credit line, the app will just make the minimum monthly payment.

Tally offers lines of credit ranging from $2,000 up to $20,000. The interest rates depend on your credit score and range from 7.9% to 25.9%. This sounds similar to taking out a personal loan for debt consolidation, but a line of credit works differently than a personal loan. When you get a personal loan, you get the money in one payment. You can then use it to pay off credit card debt or anything else. Each month you pay back the loan in a fixed amount.

What Tally offers is a revolving line of credit. A line of credit allows the borrower to use the money as needed, and there isn’t a fixed payment due each month, the payment depends on how much of the line of credit is being used.

Using Tally

It’s easy to get your Tally account set up. To be approved, you must have a FICO score of 660 or higher. That puts you at the very low end of a “Good” credit score. Tally will take other aspects of your credit history into account too, so your credit score isn’t the sole determining factor.

You’ll need to enter the usernames and passwords to the credit cards you want Tally to help you pay down, and the bank account you wish to pay Tally from so have these on hand when you sit down to create your account. When you apply, Tally only performs a soft credit check which doesn’t affect your credit score.

Add Your Credit Cards

There are two options for adding your credit cards into Tally. If you allow the app to access your phone’s camera, it will scan the cards. You can also enter the card information in by hand. You’ll enter the usernames and passwords for each card.

Tally supports store issued and bank-issued credit cards. The app analyzes the cards you link and your credit history, a soft credit check. You’ll add your checking account by providing your username and password.

Approval

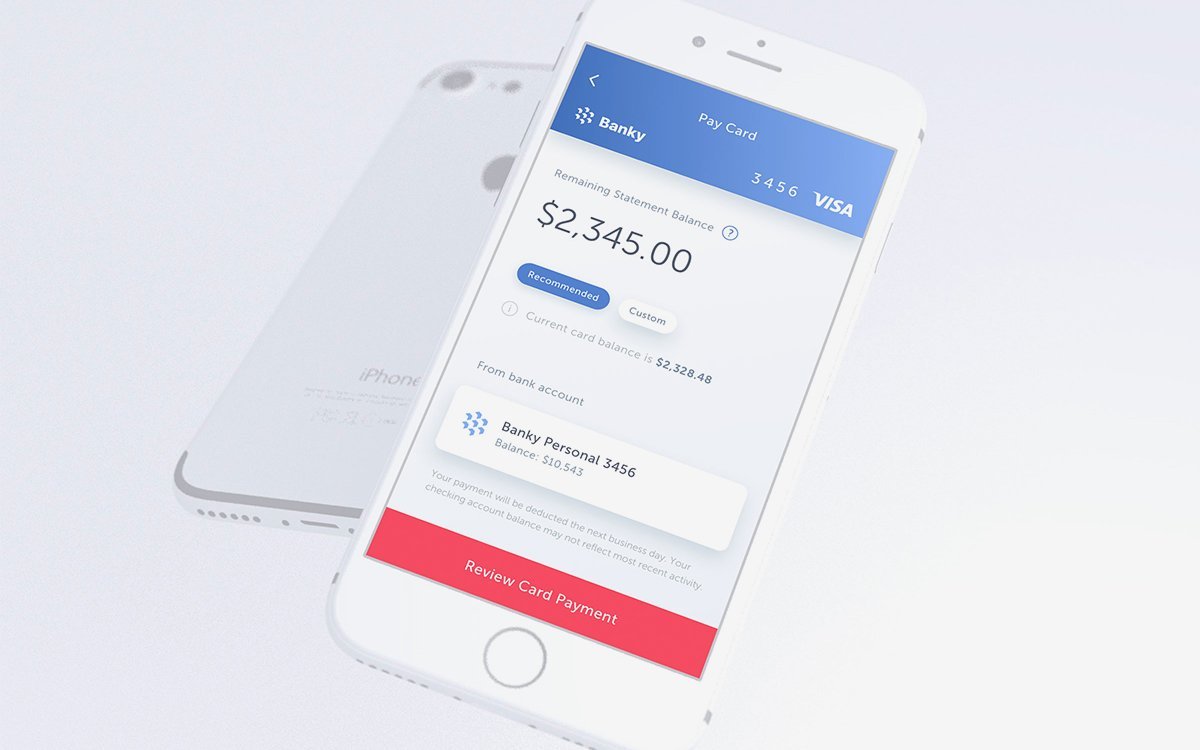

If you’re approved, you’ll see the credit limit for your new line of credit, from $2,000 to $20,000, the interest rate for the line of credit, and the due date to make your payment to Tally which is about a month from the date you create your account.

Tally will use your line of credit to pay off or pay down the card with the highest interest rate. This takes about three business days.

Making Payments

There are two ways to make payments when using Tally; Tally Pays and You Pay, and you can choose either option for each card you’re managing in Tally.

If you use Tally Pays, the app will make your credit card payments using your line of credit prioritizing the cards with interest rates higher than the rate on your line of credit. For cards with rates lower than the rate on your credit line, Tally will just pay the minimums. This is how the stacking method of debt repayment works. You save money in interest when the high-interest cards are paid off more quickly.

Tally sends you a single bill. That payment is used to make the minimum payments, and the amount remaining goes toward paying the principal and interest on your line of credit.

If you opt for You Pay, Tally will send you a reminder a few days before your credit card payment is due. You can make those payments through Tally using your linked checking account or make your payment on the card issuer’s site as you’ve always done.

If you’ve had a problem with paying your credit cards on time, you can enable Tally’s Late Fee Protection feature. Tally suggests making your payment at least a week ahead of the due date. Tally needs time to recognize that you’ve made a payment. If you pay later than that and have Late Fee Protection enabled, it can result in a double payment because Tally will make a minimum payment for you.

What Does Tally Cost?

Tally charges no annual fee, origination fee, prepayment penalty, balance transfer fee, late fee, or over-limit fees. What you pay Tally is just the interest charged when your line of credit is used to pay your credit cards. Your monthly payment to Tally is based on the amount of your credit line. If you use Tally Pays, your monthly bill will consist of those payments, the interest rate Tally charges you, and 1% of the total amount of your credit line.

When Tally pays your credit card payments, your monthly bill will include those payments, the interest based on your APR, and 1% of the total amount of your line of credit. If you pay the cards yourself, your monthly payment to Tally will include the interest and 1% of the total amount of your credit line.

Is Tally Safe?

A lot of people may have strong reservations about giving an app access to their financial accounts. While there is never a way to guard against the threat of hackers completely, Tally uses bank-level encryption.

Where Tally is Available

As of this writing, Tally is available in Arkansas, California, Colorado, Connecticut, Washington DC, Florida, Georgia, Illinois, Idaho, Louisiana, Maryland, Massachusetts, Michigan, Minnesota, Missouri, New Mexico, New Jersey, New York, Ohio, Oregon, Oklahoma, Pennsylvania, South Carolina, South Dakota, Tennessee, Texas, Utah, Washington, and Wisconsin.

If Tally is not currently available in your state, keep checking back. New states are regularly added.

Tally Alternatives

Tally is a great tool to help you become debt-free, but it isn’t the only way, and in some cases, is not the best option.

The best option for paying off credit card debt is a balance transfer credit card. During the introductory period, usually lasting from 6 to 24 months (24-month offers are rare), you won’t pay any interest on the balance you transfer to the card. If your credit score is good enough to be approved for a 0% APR balance transfer card and you can pay the balance in full before the introductory period is over, this is your best option because you won’t pay any interest.

You don’t want to apply for cards you won’t be approved for though because applying for a card negatively impacts your credit score. Create an account with Credit Karma, see your credit score, and a list of balance transfer cards you’re likely to be approved for based on your score.

You can shop for the best rates on personal loans at a site like Credible or Upgrade. Doing so won’t impact your credit score. Shop around and see who is offering the best rate. These lenders may give you a better rate than Tally.

If your credit score rules out these options and Tally, you can still pay off your credit card debt using the snowball or stacking method. You need to have a plan so that you’re paying off the debt as efficiently as possible. Snowball has psychological benefits, but stacking is the method that will save you the most money in interest.

Is Tally Worth It?

Tally is pretty new on the personal finance scene. The company was founded in 2015 but only became available to the public in late 2017. Should you add Tally to your financial toolbox?

Tally Positives:

- Tally uses the debt stacking method: The debt repayment method that saves you the most money by paying off your highest interest credit cards first.

- Tally only does a soft credit check to determine approval: It doesn’t impact your credit score the way a hard check does. When you apply for a balance transfer credit card (or any other kind of credit card) or a personal loan, the lender does a hard check.

- Speaking of credit scores, most Tally users will see a jump in their score: Utilization(how much of your available credit you’re using) makes up 30% of your FICO score. By using a Tally line of credit to pay balances down or off, your utilization goes down, and your credit score goes up!

- There really is no excuse to make late payments on your credit card when it’s so easy to automate the payments: But if this is a problem for you, enabling the Late Fee Protection option can eliminate late payments.

- There are no fees to use Tally including late payment fees: However a late payment will be reported to the credit bureaus, and payment history is the most significant factor in your credit score.

- If you are struggling to meet your Tally payment, reach out: The company is willing to work with customers to set up a payment plan that works for both sides.

Tally Negatives:

- When Tally uses your line of credit to pay off or pay down your credit card balances, guess what?: There is room on what may have been maxed out cards. Nothing is stopping you from charging those cards right back up. If you can’t control your spending, using Tally may land you in even more credit card debt. You can cut up the cards and remove the numbers from your online shopping accounts, but that may not be enough to remove the temptation for some people.

- Tally may not be the best option: If you can get a 0% balance transfer credit card or a personal loan at a lower interest rate than Tally offers you, those are better choices.

- Not everyone can use Tally either because it’s not available in their state or their FICO score is below 660: Tally is expected to be available nationwide eventually, and you can always work on improving your credit score and apply again.

My Tally Experience

I actually have been using Tally before I knew I was going to review the app. Unfortunately, I had credit card debt as a result of some dental work. I know, I know. A personal finance writer who has credit card debt.

Sometimes the cobbler’s children have no shoes.

Tweet ThisSo far, my experience has been great. I hated seeing that balance on my card. I didn’t want to use a balance transfer credit card because I already have too many credit cards and didn’t want to add another. (Due to a short-lived love affair with credit card churning in order to collect obscene amounts of airline miles).

And I didn’t want to take out a personal loan for such a relatively low amount. I was searching for alternatives and found Tally. I had a few snags. When I tried to take photos of my credit card through the app, I couldn’t get it to work, so I had to add it in by hand. Certainly, no big deal but a feature that should have worked didn’t.

The other snag was the amount of time it took for the credit card to be paid off. I think I set up my account on a Thursday and it wasn’t paid off until Tuesday or Wednesday of the following week. This isn’t really a problem; it takes a few business days for this all to happen. But it made me nervous! You can reach Tally customer service via phone or email. I was planning to call but checked my balance one more time before I did it and saw the card had been paid.

Within a few days, my credit score shot up 22 points. I’m only a couple of months into my Tally experience but so far, so good!

Final Thoughts

If you have tried to use the stacking method to pay off your credit card debt in the past and been unsuccessful for whatever reason, Tally is excellent. It does the work of utilizing the stacking method for you. Tally is also great for those with high credit card utilization who are looking to boost their credit scores. If you have multiple credit cards and have trouble managing the payments, Tally does that for you, and you only have a single payment to make.

For those of you who pay off your credit cards in full each month, Tally doesn’t really have much to offer you. You could use Tally to manage your payments, but to use the service, you have to apply for and accept a line of credit. If you have no debt, you do not need a line of credit. Just keep doing what you’ve been doing.

![Chase Credit Journey: A Free Credit Monitoring Service [REVIEW]](https://www.listenmoneymatters.com/wp-content/uploads/2020/03/chase-credit-journey-featured-768x432.png)