Lending Club’s returns are great! I’ve made over 18% returns doing what banks have done for ages – lending people money. A strategy few experts talk about.

Banks lend you money because it’s extremely profitable. A major share of a compan like Bank of America come from mortgages and credit cards – loans to individual people. The rates that most of these loans go for are pretty solid and always based upon fixed payments.

Imagine lending someone $200 at 18%+ like a crazy profitable bank. You would earn $36 a year. Yes, that’s nuts. Guess what, now you can get in on the gravy train too and this particular gravy train is called Lending Club.

This is my

What is Lending Club ?

Simply put,

Borrowers use

Personally my investment focus is on Small Business loans as the returns are excellent and they are often made by people willing to work hard – something I always invest in.

Lenders show up and participate in

Lending Club is geared towards helping the lender as much as possible because without them the system wouldn’t work. They have a vested interest in lenders being more successful here than other investment opportunities.

How It Works

Lending Club functions similar to a mortgage company in that they help broker deals for amortized loans. Amortized loans are just loans that are front loaded with interest payments and are structured such that overpayment simply reduces the overall term of the loan, not the monthly payments.

Loans like this are stacked in the lenders favor as the lender will receive a higher portion of interest earlier in the loan allowing the lender to not really care too much if the borrower pays the loan off early. The one major difference between

The primary objective of

As a borrower you will have to make monthly payments to

If you’re an investor it’s even easier. You link your bank account, transfer the funds over to your personal

The beauty of the treasure trove of data which

How to Invest with Lending Club

There are a ton of different strategies to investing with

Since

In order to get 12% returns or higher, I turned to Lending Club’s data (login required) to make my decisions. Remember, our goal is to shoot for the average optimized portfolio although I think that if we’re thoughtful about our investments we can do even better. Based at no more than 5 minutes at the summaries on their data portal we we can tell that the highest portfolios:

Are Grade E with an interest rate of 11.04%.

Have higher return rates the more money you invest. This is interesting and I’m guessing because as you get more and more diverse, each bad loan hurts less.

Have more than 100 individual investments ($2,500+)

Yup, that’s it, statistically, if you do that you’ll exceed our 12% goal. Now we could just blindly pick all loans that match these categories or we could be more thoughtful and try to add a few more restrictions. I don’t want to be giving a loan to any deadbeats who likely won’t pay me back. Worst case, if a loan does go sour, I can always try and sell it before it goes completely bad. I can do this through FolioInvesting but that’s going to be annoying and there will be no guarantee I’ll actually be able to sell them. Instead, I’m going to try to proactively avoid these bad loans.

That begs the question, who is the type of person we want to lend to? We’ll I want them to be decent debt handlers and have decent credit, no delinquencies in the past 2 years, and no major derogatory marks. I want them to have a relatively reasonable amount of credit utilization because I don’t want the loan I invest in to be too much for them. Finally, I’ll be a total dick and judge them on their job and gross income ;) The best part is if they lie on their loan application,

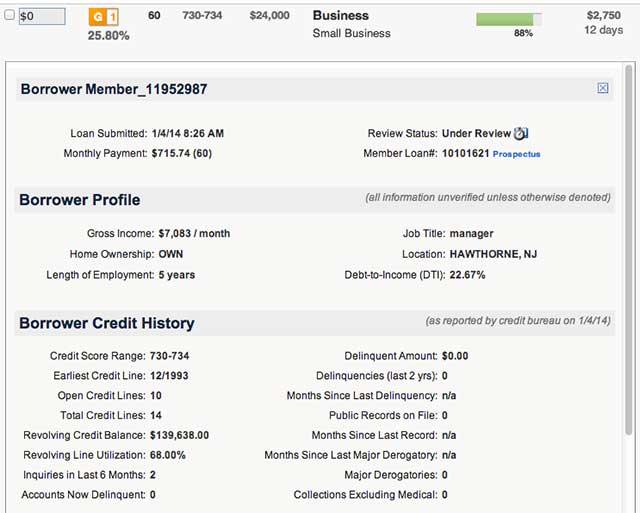

This is an example loan that I invested in right before I wrote this article (I always reinvest loan income). Now, it meets our core requirements of having a decent credit score and a solid credit history but you’ll notice one crazy thing. Look at that Revolving Credit Balance! It’s $139,638! That’s a crazy high number but if we look at the Debt-to-Income ratio, it’s 22.67%. Woah, that means his yearly income is $615,960.

How could this be? Figure the guy or girl got their first credit card as soon as they turned 18 (like most of us did) then that means if their first credit line was in 1993 they must be 39. Ok, now it’s sounding a little better. Also, they are opening up a small business loan. So, maybe this money is going into an existing business for an experienced guy who knows what he’s doing and really doesn’t have much debt. If so, I’m in luck!

Of course you can’t always get lucky so sometimes you have to give loans out to people who much more normal. In fact, some of the best ones I invest in are for Credit Card Refinancing. That’s a cause I can get behind and something I definitely recommend using Lending Club for.

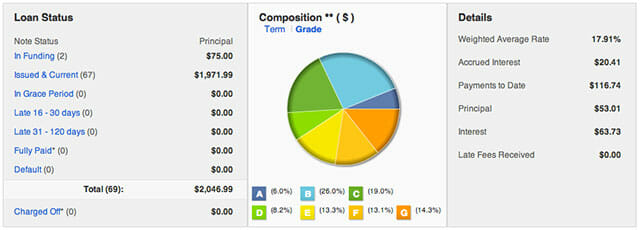

This is an example of what I invest in – not always according do the core rules and definitely skewed towards higher interest loans.

Since it’s hard to just look at loans as rates of return, I like to personally classify them by type of investment. I figure this may tell me a few interesting things over time and since it takes only an extra minute with each order, I decided to set it up.

Take Aways

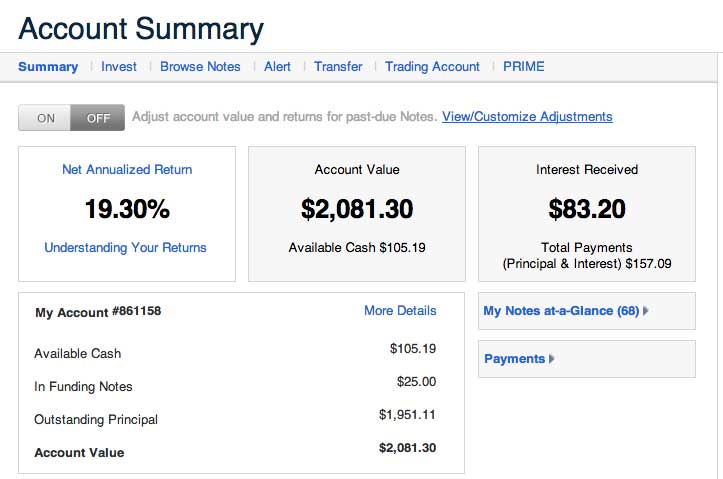

So, will this all work out? I have no idea but based on the data it looks like 92% of the people who have 100 notes or more worth $2,500 or more make a return of at least 6%. Since that’s not far from the market average I figure it can’t be that bad. Right now my Net Annualized Return is 19.30% so I’m off to a good start!

Are you thinking about using Lending Club? Do you use it right now? Let us know in the comments!

UPDATE: Lending Club reached out to me and whispered that they will be launching a “Small Business product soon”. I would be lying if I wasn’t really excited. As soon as I hear anything I’ll be updating this post so check back!

Featured Image Photo Credit: “Left Hand – Kolkata” by Biswarup Ganguly

Fiscal flexibility that’s funny, free and delivered weekly.

Current Project: Making bloggers money with Lasso.