- A Global Problem

- Day 1: Write it Down

- Day 2: Make a Debt List

- Day 3: Cut ‘Em Up

- Day 4: Create Your Budget

- Day 5: Plug Your Spending Leaks

- Day 6: Save Money on Necessities

- Day 7: Champagne Life on a Beer Budget

- Day 8: Make It Automatic

- Day 9: Reduce, Consolidate, Settle Focus

- Day 10: Make More Money

- We’re Rooting For You!

Your debt is an emergency so you need a debt reduction plan to regain control of your money and your life. Whether you have a small amount of debt or a mountain of the stuff, we will show you how to reduce your debt and get relief with our 10-day debt reduction plan.

A Global Problem

Debt is a serious problem and not just in the U.S. It brought the global economy to its knees a decade ago.

Unless politicians in Washington sincerely tackle how we as a society are to reduce the national debt, there will be not only episodic financial crises in the years ahead but also significantly diminished economic opportunities.

Debt left unattended can for a time be ignored. But as people, companies, and governments found out in 2008, ignored for too long and that debt can burn down houses, businesses, and economies.

If your home were on fire, would you see that as an emergency?

Your debt is no different. You need to take immediate, meaningful action to put out the fire before it’s too late.

That’s where our 10-day debt reduction plan comes in. It will be the fire extinguisher for your debt. We will give you 10 steps that you can take to pay off your debt once and for all.

This guide will also teach you to face your debt, cut expenses, automate your finances, lower your interest rates, and find debt relief help.

You will learn to find spending leaks and plug them, to get a raise, and to make extra money in your spare time.

It will also help you recognize and address the reasons you ended up in debt.

Within this guide, there are lots of helpful links to articles and podcast episodes that will go into even greater detail on topics that require a deep dive.

He who would search for pearls must dive below.

Tweet ThisAre you ready to take charge of your money and your life? Good, because here we go.

Day 1: Write it Down

Whatever amount of money you’re currently living on, you could live on less. And in order to pay off your debt quickly, you’re going to have to. Your first step is to write down your bare-bones expenses and the cost of each.

And by bare bones, we mean, only the things you absolutely must have.

- Housing Payments – You need a place to live!

- Electricity + Heating Bills – These days I don’t think you can be very effective without power.

- Internet + Cell Phone Bills – The Internet is the greatest tool ever created, you need this. Cell phone is a close second.

- Monthly Grocery Expenses – You need to eat. Notice how it reads “Grocery” and not “Restaurants” or “Take Out”.

- Monthly Commuting Costs – In order to pay for even your bare necessities you need to get to work but there is a lot of potential for savings here.

- Insurance– If you own a home, the mortgage holder typically requires that you have homeowner’s insurance. Some landlords require it of renters. Health insurance is not required but it’s a false economy not to have it.

It’s not a long list, is it? Where’s the cable TV, where’s the Whiskey? They didn’t make the cut. It’s not that you are forbidden from spending on those things but they aren’t essentials.

It’s important, to be honest when making this list. If you’re already sneaking in luxuries in at Chapter 1, you aren’t fully ready to become financially secure and wasting your time.

So, how much of your income should you be spending on the bare necessities?

The actual number will vary for everyone so it’s easier to use a percentage. All of your necessary expenses combined should make up no more than 50% of your take-home income. To see if you’re meeting that rule, you need to know how much income you take home each month.

The other number is your “real income”, how much money you’re actually left with after paying taxes. Include all sources of income, from your job, from any side hustles you have, etc.

General Spending Guidelines

Everyone’s expenses vary but some general guidelines will at least give you a sense of if you’re overspending on necessary expenses. If you are, we’ll show you how to reduce these expenses later in the article.

- Housing – Housing costs shouldn’t exceed 1/3 of your real income. For example, if your Real Monthly Income is $3,000, housing payment shouldn’t exceed $1,000.

- Utilities – The number shouldn’t exceed 1/3rd of your housing payment.

- Internet + Cell Phone– You shouldn’t pay more than $60 a month for Internet and your Cell bill shouldn’t exceed $80.

- Monthly Grocery Expenses – This number is available because the government tracks them. According to the USDA, one adult male can eat for less than $350 a month, an adult female for less than $31,2 and each child (11 or younger) for less than $330. You can easily shave $100 off of those numbers.

- Monthly Commuting Costs – Americans are extremely car-dependent but driving your own car isn’t your only option. People are literally driven into debt by cars. Not only are there lots of hidden costs, but cars are also among the worst investments you can make as they lose value quicker than just about anything at their price point.

- Insurance – It’s tough to shop around for health insurance. It’s all expensive and it all sucks. Homeowner’s and renter’s insurance are different though. The average cost for homeowners is $1,516 per year and renters is $184. There is so much competition that it’s easy to lower your rate.

Got all your numbers? Then, we’re ready to move ahead. Remember, if your numbers are higher than outlined above, that’s ok. We’ll get you on track later in the article.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

Day 2: Make a Debt List

Here comes the scary part. You may have no idea how deep in debt you are. It’s hard to face but what can be measured can be managed. We’re going to make a list of all your debts excluding mortgage debt. Include the financing institution and the interest rate for each debt.

Below is a list of debts that you may have and a summary of how painful it is.

- Payday Loans – This is legalized loan sharking. If you have these we need to get rid of them ASAP!

- Credit Card Debt – Close to but not quite the evilest form of debt. Reducing this is a priority as the rates are high and it compounds quickly.

- Small Business / Miscellaneous Loans – While the rate generally isn’t terrible, it’s usually not great either because these loans are risky for lenders.

- IRS Debt – The IRS strongly encourages timely tax filing and payment to avoid penalties. If you fail to pay your taxes on time, you’ll accrue a monthly penalty of 0.5% on the unpaid amount, with a maximum of 25% of the unpaid taxes.

- Personal Loans – Depending on your credit score when you applied, the interest rate here might not be too bad or it might rival credit card debt. Rates can go Credible so these could potentially be part of how you dig yourself out, but we’ll get into that.

- Student Loans – Typically low rates but you might be able to do better.

- Auto Loan –These rates are typically not terrible

- Home Equity Loans – This is not a mortgage. It’s when you borrow against the existing equity in your home. Interest rates are usually good because the bank has your house as collateral if you default. There is quite a bit of potential here to refinance some of your more expensive debt.

Have you written it all down? I’m going to show you an easier to track your debt. Why did we make you write it down? Because writing it yourself and seeing it on paper brings it home.

Better Than Paper

Writing out a list of debts is important because you see it all there in black and white. But when it comes to tracking and paying off your debt, you need something more advanced than pen and paper.

There is a great tool that will be your ally in the battle for debt reduction. Undebt.it is a free tool that will help you build and follow a plan so you can kill your debt once and for all.

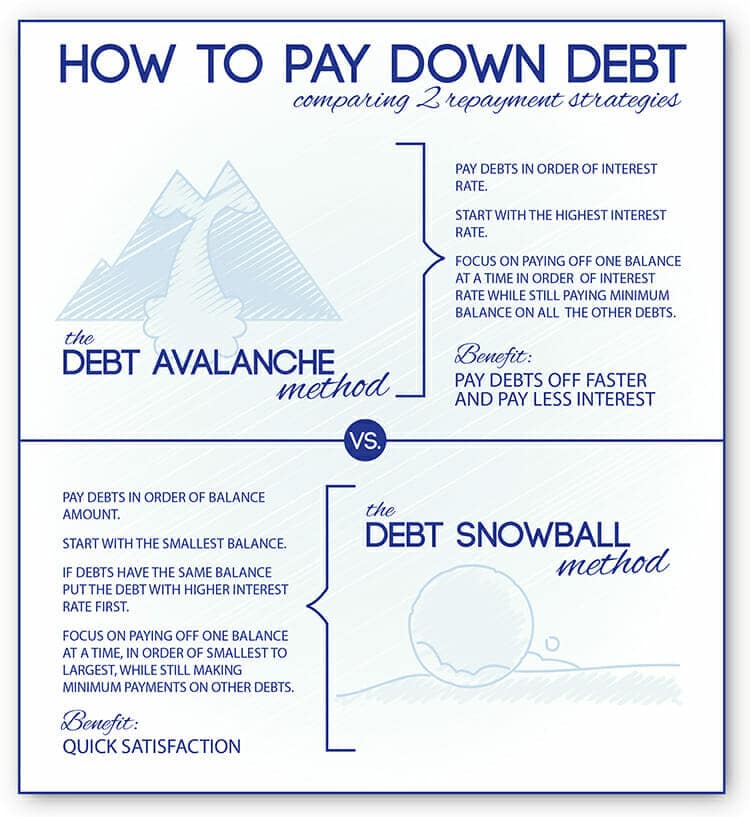

There are a few plans to choose from but the best one is the avalanche or stacking method. This method lists your debts according to interest rate, highest to lowest. You pay as much as you can on the first debt while paying just the minimums on the others.

Setting up Your Undebt.it Account

It’s fast and easy to get set up.

- Create an Account: Enter your email address, create a password, your name, and the total monthly budget which is the total amount you currently have to pay on all debts.

- Add Your Debt Information: See, it wasn’t just a punishment to make you write out a list of your debts because you need it for this! Add each debt including balance, interest rate, and minimum payment. You don’t connect your credit cards or other accounts, simply enter the information.

- Visit the Dashboard: The Dashboard page is your overview. You see when each debt will be paid off and how much interest you paid on each. This page also has a payment manager where you can enter payments and keep track of due dates.

- Review the Debt Snowball Table: This page gives you a view of each month’s payments, how much you’ve paid on each debt, and how much you still owe. It also shows how much interest you’re paying every month which is a big source of motivation. It will anger you to see your hard-earned money going to pay interest.

Key Features

You can switch between the various methods to see what each one will look like but remember, the Avalanche Method is the one you’re going to use because it saves the most money.

If you’re not convinced, check out the Compare Methods page. It shows you the particulars of each method including how much you will pay in total with each and how long each method will take to get you debt-free.

Both of those numbers will be the smallest with the avalanche method although the snowball method has its champions including Dave Ramsey, we want you to use the avalanche for debt reduction.

Sticking with the snow theme, there are also debt snowflakes. Those are extra dollars you can put toward your debt that are in addition to what you entered as your monthly budget when you created your account.

This is another way to motivate yourself towards your debt reduction goal. The more snowflakes you add, the faster the total of your debt goes down.

Once the first debt is paid off, Undebt.it rolls the money you were paying on it to the next debt on the list while paying the minimums on the rest. You continue in this manner down the list until all of your debts are paid off.

They also track credit utilization. Utilization is one of the factors that make up a credit score. If you have a total credit line of $10,000 and your balance is $9,000, your utilization is 90%. Ideally, you want that number below 30%.

If you’re in credit card debt, your utilization is likely not under 30% and it’s hurting your score. With each payment you make, your utilization will go down, boosting your score. Another great motivator.

Creating an account with Undebt.it is non-negotiable. We’ve chosen it as one of the tools in your debt reduction arsenal because it works and it’s free. Remember, what can be measured can be managed and this tool helps you measure and manage your debt.

Now that we know who we owe money, how much we owe, and how painful each debt is it’s time to move forward!

Day 3: Cut ‘Em Up

You might think you can skip this step and still pay off your debt quickly but you’re wrong. We know some of you have gone into credit card debt due to a long-term period of unemployment or medical expenses but the majority of you are just irresponsible spenders.

If you don’t comply with this step, you might as well stop here and give up.

You’re going to take ALL of your credit cards and cut them up into tiny pieces. Throw these pieces in the air like confetti, flush them down the toilet, give them to your cat to play with, whatever, just do it.

We’re in agreement that you have a problem and it’s absolutely critical that we make sure you keep it under control until it’s fixed. That means not adding new debt to the existing mountain.

Going forward, you’re strictly cash/debit card. I recommend using your debit card over cash because you can track debit card spending online but it’s harder to track cash unless you save every receipt which no one does.

It is nearly impossible to drive yourself deeper into debt using these options. I say nearly impossible as you still can overdraw your account so please be conscious of your account balances!

We’re cruising right along, good work so far. If you need to, go take a nap or something because the next chapter is by far the most important of this entire book. You will need to not only read it but absorb as much as you can.

Day 4: Create Your Budget

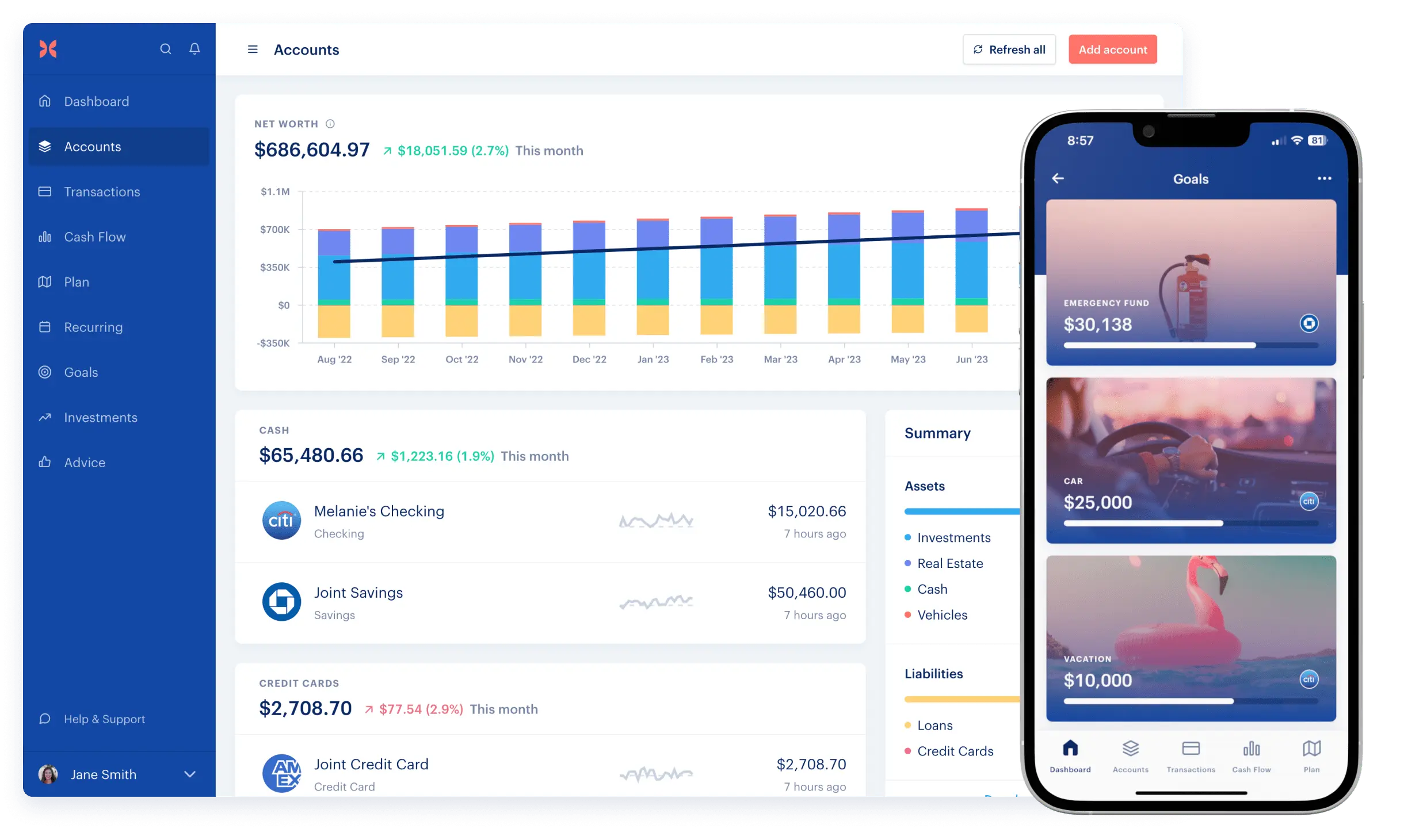

Monarch Money is a budgeting app that allows users to connect their financial accounts to track spending, categorize expenses, set budgets, and receive alerts about unusual spending. Reviews of Monarch Money say that it is easy to use and provides good insights into spending habits. Here is a summary of what Monarch Money offers:

- Consolidation of financial accounts.

- Expense categorization.

- Spending insights.

- Custom budget setting and monitoring.

- Unusual spending alerts.

Getting started with Monarch Money:

- Sign Up: Visit the Monarch Money website and create an account (30-day free trial) using your email address.

- Link Your Accounts: You can connect your bank accounts, credit cards, and investment accounts to Monarch Money.

- Create a Budget: Allocate your expected income towards various expense and savings categories. This ensures all your income is accounted for, and Monarch Money tracks your spending compared to these allocations. It provides visuals to help you understand how well you’re sticking to your plan.

- Track Expenses: You can regularly check your transactions and categorizations, and Monarch Money provides spending insights.

- Track Your Investments: Monarch Money keeps a watchful eye on your investment holdings, allowing you to see how your investments are performing over time.

- Monitoring and Adjustment: Monarch Money offers alerts for unusual spending and allows adjustments to budget categories throughout the month.

- Review Reports: Regularly check financial reports and insights provided by Monarch Money to understand your financial health.

You can use a tool like Monarch Money to streamline tracking your net worth. By pulling together your financial data from various accounts (assets and liabilities), Monarch Money will automatically compute your net worth, offering a clear snapshot of your financial health. This feature is particularly useful for tracking your financial progress over time and making informed financial decisions.

You don’t have to go nuts with budget categories. This will show you the best way to categorize your budget without going nuts.

Budgeting Monthly Homework

Well done! You’ve set up your Monarch account, trawled through your spending, made a budget and lived to tell the tale. The hard work is over, now you just need to keep things going.

Over the course of the month, log in and check to make sure you’re still on track. This should become a lifelong habit, even after you’ve got your spending totally under control. You can even do it on the go with Monarch’s app!

Day 5: Plug Your Spending Leaks

Money is a terrible thing to waste and you’re probably wasting a ton of it without even realizing it. Maybe you pay for HBO but never watch it or signed up for Dollar Shave Club but have decided to grow a beard.

Whatever they are, you have to find these leaks and plug them!

Saving money is vital and the easiest way to do it is to stop paying for things you don’t use or need. Plugging spending leaks is simply a way to optimize your spending and often, it can still include buying the things you want and need.

There are tons of potential leaks and we can’t address them all so let’s go over the most common ones and explain how to detect and plug them.

Enjoy Our High Yield Savings Account. An online savings account with no fees, easy access to your money, and one of the best savings rates on the market.

Watch your savings grow with our exceptional rates

Don't worry about maintenance fees because we don't have them

Enjoy knowing your money is secure and FDIC insured

Detecting Your Leaks

This is one of the reasons you set up a Mint account, it makes it easy to see your spending leaks. Look at your spending for the previous month list your expenses from most expensive to least expensive and look at where your money is going.

Any recurring non-essential monthly expenses that are over $50 should be seriously questioned as should any spending you can’t explain.

Recurring expenses like your cable bill and easily be reduced or eliminated entirely. There is no reason to pay so much for cable when there are so many cheap TV subscription services.

Plugging Your Leaks

When looking for ways to plug your leaks, look no further than the Three C’s; Cancel, Cut, or Commit.

Cancel

Like the example above, cable is a solid Cancel because you can get a similar service for much less. Most of your Cancels will be services you don’t really use or never use but didn’t realize you were still paying for.

Cushion is like having your own financial, personal assistant. The Cushion app automates the process of identifying and negotiating refunds for bank and credit card fees, such as overdraft, late, and monthly service charges. Using artificial intelligence, Cushion seeks to recover disputable fees on behalf of users, aiming to save them money and enhance their financial management through insights into their spending habits.

80% of people save money by using Rocket Money to find and cancel unwanted subscriptions! With Rocket Money, you can also effortlessly track your spending, easily lower bills and track your net worth.

Cut

Cut is like downgrading to a cheaper service than what you pay for currently. Do you need 5,000 text messages a month? If you’re always on WiFi, do you need unlimited data? Any service you don’t Cancel, you should make some kind of Cut to. This is something Rocket Money can help with. More on them coming up!

80% of people save money by using Rocket Money to find and cancel unwanted subscriptions! With Rocket Money, you can also effortlessly track your spending, easily lower bills and track your net worth.

Finally, Commit. A lot of services like renter’s insurance or health clubs will give you a discount if you pay for a year upfront rather than month to month. You know if you work out regularly or not. Don’t Commit to something you’re not 100% sure you’ll stick with.

Look At All That Money!

Hopefully, these exercises and suggestions have shined a light on some spending leaks and given you ways to save some money. You should have at least an extra $100 after that. If you don’t, go back and do it again. You weren’t really trying.

All of this “found money” is to be used for your debt relief.

Day 6: Save Money on Necessities

Now we’re getting down to it. While you have to spend money on necessities, you can reduce their costs.

We had you list your bare-bones expenses and gave you some guidelines for how much you should be spending in each category. If you’re spending more than we outlined, or even if you aren’t, there are ways to bring the cost of necessities down.

And every dollar you save on necessities is an extra dollar you have for debt reduction.

Housing

This is the hardest bare-bones category to cut because the suggestions are drastic but it’s also likely your biggest expense so reducing it can really accelerate your debt repayment. Move to a cheaper place, get a roommate, move in with family for a time, or at least crash on a friend’s couch a few nights a month and rent your place out on Airbnb.

Utilities

You can do all the usual stuff you read about in articles about saving money like using cold water to wash your laundry, putting plastic film over the windows in the winter, unplugging devices that are not in use, etc.

And you should do those things but frankly, the difference they make is negligible. If you want to see a real reduction in your utility costs (including phone and internet here) you have to negotiate better rates.

But that takes time and you’re probably lazy. So let Rocket Money do it for you. 80% of people save money by using Rocket Money to find and cancel unwanted subscriptions! With Rocket Money, you can also effortlessly track your spending, easily lower bills, and track your net worth.

Groceries

There are a ton of ways to save on groceries. Eat only what food you have in the house until you’ve eaten it all. Learn to use a slow cooker, cook in bulk, and build meals around what is on sale at your preferred grocery store for the week. Wasting food is an expensive habit.

Collectively, we throw away a lot of food: 38 percent of food in the United States goes uneaten.

Every time you throw away food, that’s money down the drain. In fact, a four-person family loses about $1,500 a year on wasted food.

And when you’re in the grocery store, use the Shopkick app. You can earn points that can be exchanged for gift cards when you do things like scan barcodes and buy specific products.

Commuting

We get it, some people require a car. But it’s not as many people as those who have cars. I have never driven and I haven’t always lived in places with great public transit. So what did I do? I walked, rode my bike, took an Uber, asked a friend for a ride, and used public transit in cities that offered it. If you can drive, you can add renting a car to that list.

So not all of you need a car, you just want one or maybe you’re just so used to having one that you never gave it much thought. But I’m far from the only person who makes do without a car, a car payment, gas, insurance, and maintenance expenses.

What would you do if your car were totaled tomorrow and you couldn’t afford to replace it? Do that. Or at the very least drive less using the suggestions I made.

Insurance

You can probably pay less than what you’re currently paying for homeowners or renters insurance. There is so much competition that it drives down the price but many people don’t bother to shop around once they have a policy.

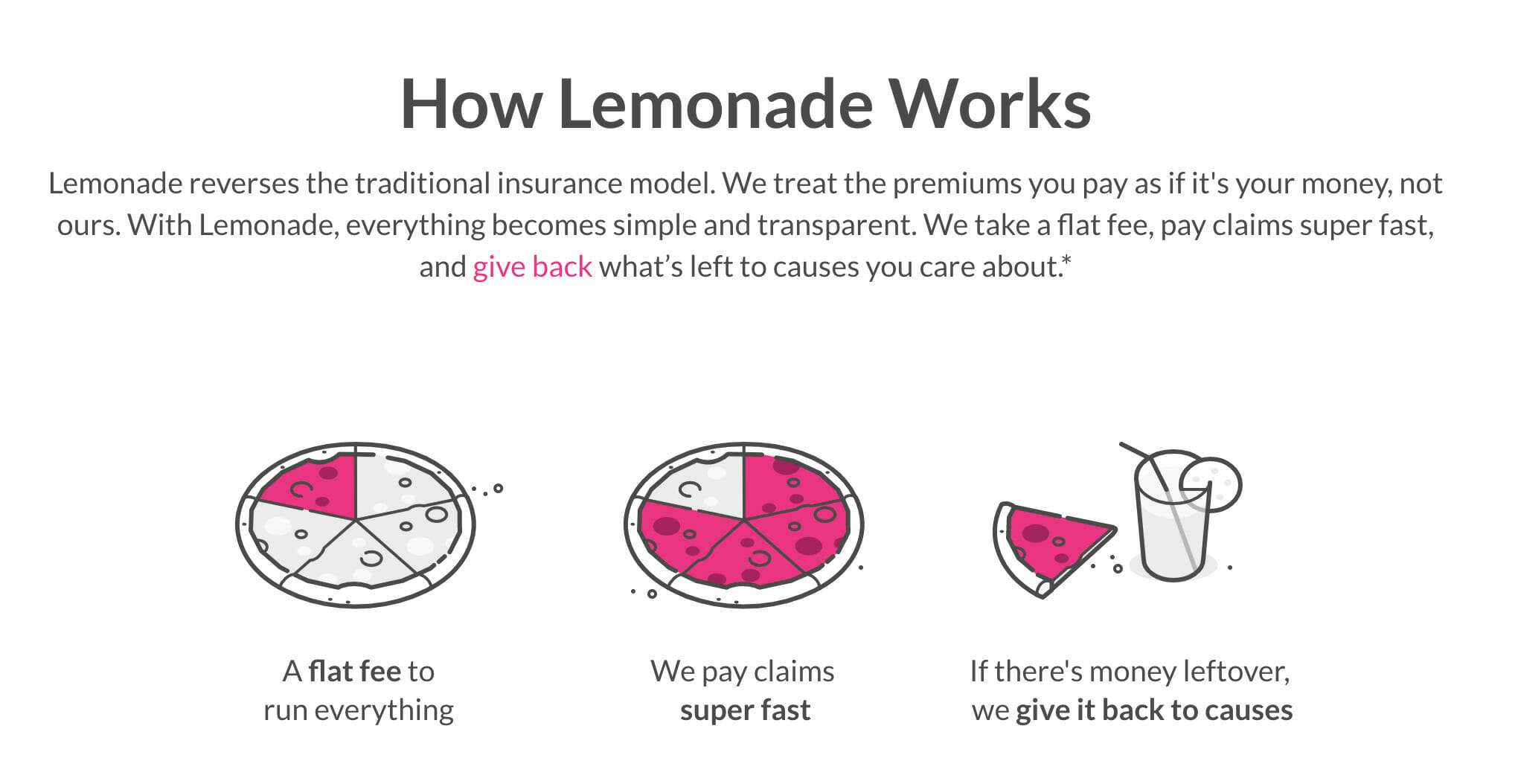

And there is a company that is changing the way insurance works. Lemonade uses the peer-to-peer model which allows them to provide insurance at a great price while giving great customer service.

It’s free to get an estimate so check it out and see what Lemonade can save you.

Day 7: Champagne Life on a Beer Budget

When it comes to being financially healthy, it’s less about what you earn than what you spend. That’s why you hear about people making six figures who live paycheck to paycheck. If you want to pay off debt and grow your wealth, you have to reevaluate your lifestyle.

There is no magic bullet. In this chapter, we’ll start applying what we’ve learned so far to make changes to your spending habits. We’ll distill it down to two actionable steps you can use to fix your broken spending habits.

Check Your Head

Mindset is everything. You’re not necessarily broke because you don’t make enough money and life is too expensive. You’re broke because your head hasn’t been in the right place.

Why did you let your debt get so high? Why do you upgrade your perfectly good iPhone and use a credit card to do it? You have to face up to the problems you’ve created.

Do you spend money when you’re angry, sad, depressed, happy, bored? The next time you get the urge to make an impulse buy, note how you’re feeling. And think of some things you can do when those feelings come up that don’t involve digging yourself into a bigger pit of debt.

Call a friend, go for a run, cook a meal, color in a coloring book, anything that isn’t spending money.

Find Disturbing Spending Trends and Take Action

We showed you how to do this above. Tools like Monarch and Cushion can show you where you’re wasting money. But this is not a one-time action. You need to look for areas of waste every month and if you find them, take action to correct them.

Don’t Upgrade

Do you upgrade your life every time you get a raise or a bonus or your tax refund? Stop doing that. You don’t need a bigger apartment, a nicer car, a newer phone, or a flatter-screen TV. What you have is perfectly fine.

Use that money to pay off your debt and once it’s paid off, use it to fund your retirement.

Make New Friends

Did you get into debt because you were keeping up with your friends? This happens to a lot of people especially if they spend a lot of time on social media sites. You see the things all of your friends have or the things they’re doing and you want those things too.

It turns out, nearly 40% of Millennials have spent money they didn’t have and gone into debt to keep up with their peers, according to a recent Credit Karma survey.

Expenses range from experiences, like travel, parties and nightlife, music and sporting events and weddings, as well as food and alcohol, clothes, electronics, jewelry, and cars.

So you whip out your credit card to pay for them and here you are, reading this guide to getting out of debt.

If your friends are real friends, they won’t care if you drive a ten-year-old car and don’t live in a fancy apartment downtown. If your friends do care about those things, you need to make some new friends, financial friends.

Have Fun For Free

Having fun is only expensive if we make it expensive. Don’t go out to dinner, have a potluck. If you want to go out for drinks, find a good happy hour. Check your area’s paper for free events. Wait to visit a museum until there is a free entry day (or hours). Have fun for free.

Day 8: Make It Automatic

Forgetfulness is a big component of financial destruction. You forget to pay a bill on time or forget to pay it at all, you forget how much you’ve already spent in a certain budget category so have no idea that it’s only two weeks into the month and you’ve already blown through your food budget.

These things happen because money isn’t at the forefront of our minds and we don’t want it to be. Thinking about money is at best boring and at most, a serious source of stress. But you can eliminate this kind of forgetfulness when you set up an automated payment.

LMM talks a lot about automation as a way to make life easier. Sure you could keep a budget on the back of an envelope but Monarch makes it a million times easier. That’s an example of automating your finances.

Automatic Bill Pay

All of your bills need to be automated, not doing so just doesn’t make sense. Not only does it relieve you of the responsibility of remembering all of the due dates, but it saves you time because you don’t have to sit down and pay each bill.

Not to mention the money you save. When you pay a bill late or forget to pay it at all, you might be charged all kinds of fees. Late or non-payments for some bills will negatively impact your credit score as well. And some vendors will give you a discount for setting up auto debit payments. I saved $10 a month on my cell phone bill this way.

Automatic payments can be set for the bill’s minimum, an amount you choose, or the full amount due. Obviously, pay the full amount if you can, if not, still make the largest payment possible.

Direct Deposit

Most employers offer direct deposit. If your employer does, make sure you take advantage of it. It’s the 21st Century, no one should be cashing or depositing a paper paycheck anymore!

Scheduled Savings

The best way to save money is to automate it. We like to call it paying yourself first. Most banks and investment firms offer automatic deposits from your checking account into your savings or investment account.

Set up an auto transfer from every paycheck or at least once a month, even if it’s only $50. If you want to see the power of automatic saving coupled with exponential growth.

Spending Alerts

At its core, a healthy financial life isn’t much more than spending less than you make. Easier said than done and if you’re guessing at numbers, it’s nearly impossible. Luckily, there are ways to automate knowing your numbers.

One of the awesome things Monarch Money does is to send you spending alerts. You set the threshold and when you get close to it, Monarch Money will let you know. Of course, Monarch Money can’t prevent you from going over budget, but you won’t be able to say you weren’t warned.

Day 9: Reduce, Consolidate, Settle Focus

We’ve given you the tools and the know-how to reduce your spending and save money. But you may still have some debt. You have several debt relief options. In this chapter, we’ll show you a strategy to pay it off as quickly and cheaply as possible.

Reduce

The first order of business is to reduce the cost of your total debt. Call each of your creditors and ask for a reduction in your interest rate. You might assume they’ll laugh and hang up but you might also be surprised by how often this works.

The creditors (apart from student loan creditors) don’t get paid if you declare Chapter 7 bankruptcy. They’d rather have something than nothing so if they think lowering your interest rate will help them get that something, they’ll be more willing.

You have to do a little convincing though. Call them up and tell them you’re serious about paying off your debt but it’s not possible at your current interest rate. If you get a “No,” call back until you get a “Yes.”

It’s worth it. If you have $10,000 in debt with an interest rate of 18% that you want to pay off in two years and you can get the rate lowered to 16%, over those two years, you’ll save $240! Do that with three of your credit card companies and you’ll have saved $720 in exchange for maybe an hour of your time.

Consolidate

Perhaps more important than reducing your interest rates is consolidating your debt. Not only does it make it easier to focus your time and money but you’ll likely even further reduce your interest rate and possibly give you lower monthly payments.

When you consolidate your debt, you take out a new loan and use the money to pay off your debts. Doing so means you have fewer payments to make and keep track of and the interest rate on the loan is almost certain to be lower than what the credit card companies were charging.

There are a lot of companies who consolidate expensive debt though so you want to shop around for the best price. Credible allows you to do that. You can borrow as little as $1,000 or as much as $100,000 and the life of the loan ranges from 24 to 48 months.

The interest rate you are offered depends on how good your credit score is. If you don’t know your score, you can get it for free at Credit Karma.

Go to Credible and fill out some basic information. You’ll then see a list of all your loan offerings from lenders including

Select your offer and complete that lender’s application process. This does affect your credit score slightly because the lender does a “hard’ credit check. If you’re approved, you’ll have the money within a few days and you can use it to pay off your existing debt.

The whole process is painless and takes only a few minutes.

Debt Settlement

A debt consolidation loan is a great tool to get some debt relief but you do need a non-terrible credit score to qualify. But what if your score is in the toilet and you can’t qualify? In that case, a debt settlement company is an option you might consider.

National Debt Relief helps those with at least $7,500 and up to $100,000 in unsecured debt. NDR will work with each of your creditors to reduce the total amount of debt you owe.

Why would they agree to lower your debt? Because getting something is better than getting nothing. Working with NDR will stop the stressful collection calls you may have been receiving too.

You open a dedicated savings account and rather than paying your creditors, you deposit that money into the account. The amount will be determined by NDR and is usually lower than the total amount you were paying to all of the creditors.

National Debt Relief will pay your creditors from that account either as a lump sum payment or in an installment repayment plan.

There is no upfront cost to work with NDR and you don’t pay anything on debts they can’t settle for you. The cost varies from 15% to 25% of your total enrolled debt. NDR can save customers as much as 30% on their debt and the process lasts between 24 and 48 months.

Refinance

We used debt consolidation to pay off credit cards because they have a high interest rate so were the priority. If you have student loan debt, the interest rates are lower than credit card rates so it was further down the list.

But you still want to reduce the interest rates on your student loans and pay them off as quickly and cheaply as possible.

Credible is to student loan debt what Upgrade is to credit card debt. Just answer some questions at Credible and it will show you offers from a variety of lenders through which you can refinance your student loans.

You can get offers that will lower your interest rate and change the terms of your loan which can reduce the amount of your monthly payments if you’re currently struggling to make them.

Just like reducing the interest rates on your credit cards will save you money, a lower interest rate same is true of your student loans. And because the amount of the loans can be six figures, even a small reduction in interest can mean thousands of dollars in savings.

Credible will show you a variety of offers and the process is fast and easy and won’t affect your credit score.

Credible's online marketplace connects borrowers with lenders in minutes. Refinance federal, private, and ParentPlus loans. Compare student loan refinancing rates from up to 7 lenders without affecting your credit score for free! Rates range from 5.24% to 12.44% APR

Home Equity Loan

Our first recommendation is for a crowdsourced loan but a home equity loan is another viable option.

Basically, when you bought your home, you had to put money down.

That money is the equity you have in your home and it continues to grow with each mortgage payment made. A home equity loan allows you to borrow against that equity.

You get a great interest rate and consolidate debt. But there is a downside and it’s a big one. If you can’t pay back the loan, you can lose your home.

If that were to happen, it could potentially be more devastating to your finances than even declaring bankruptcy. This is not an option to consider lightly.

Focus

Once you’ve been able to reduce your interest rates and consolidate your debt, life should get easier because you have some breathing room. It feels good but don’t let it make you complacent.

You still have debt after all even if it’s now more manageable and the debt is still an emergency. Don’t lose focus. Set up the new payment on auto-pay so you never miss or make a late payment.

Doing so will cost you money in late fees and damage your credit score (which has probably come up since you used the new loan to pay off your credit cards). And if you were to make a late payment on your home equity loan, you’d have a bigger problem than debt on your hands.

Look at all that extra money you have after consolidating! What are you gonna do with it? Go on a vacation, buy a new computer? No! NO! That’s the kind of thinking that got you into this mess!

You’re going to use that money to build a three to six-month emergency fund and then use it to pay off the new debt. There can be a wicked thing called an “early payment penalty” so make sure you understand the terms of your loan.

Even with the penalty, it can still make sense to pay it off early if doing so saves you more in interest than you would pay in penalties. You’ll have to do the math.

Day 10: Make More Money

Reducing spending and saving money is a major factor in a healthy financial life, it’s more than half of the equation. But at some point, there is nothing left to cut or save (without going the living in a van down by the river eating cup of noodles route) so if you want to pay off your debt more quickly and start growing your wealth, you have to make more money.

We are going to show you how to get paid what you’re worth in your career and make more money in your spare time.

Hop, Skip, and Jump

If you want to make more money you might ask your boss for a raise. And that’s a good idea. But the average raise is a meager 3%. Even if you were already making six figures, 3% isn’t going to do much to move the needle.

There are two ways to get more than a crummy 3% raise. If you like your job and aren’t looking to leave, you’ll need to do more than ask your boss for a raise. Even if he or she tells you yes, it’s probably just going to be a relatively small amount.

Go in knowing what other people in similar jobs in similar places are making. You can find this kind of information on a site like Glassdoor or PayScale. If you’re making less than the comparables, you need to at least ask that your salary be brought up to the correct level.

You also need to prove why you deserve not only a raise but a good raise. What have you done that has made your company more money, saved it money, made things run more seamlessly, or made your boss’s job and life easier?

What if you get shot down? Then you need to start looking for another job. When you change jobs, the average pay increase is between 10 to 20%. That kind of a jump will make a difference. In fact, you should be making that kind of jump every two years.

People who change jobs frequently make 20%-38% more over the life of their career than do those who stay in the same job for many years.

And when you get that offer, the work isn’t done. Know how to negotiate to get the salary and the terms you want and deserve.

A Million and One

That’s my estimate on how many ways there are to make extra money and my estimate on how many minutes you waste each week doing things like watching TV and looking at cat pictures on the internet which do not make you any extra money.

You know the ways. There are articles, websites, podcasts, books, memes, and conspiracy theories dedicated to them. You just aren’t doing any of them. But you’re going to.

We’ll even let you choose. Do you want to make extra money online or in the real world? Online you say? Great, because we’ve got two million and one ways to do that!

Sell stuff on Craig’s List, Nextdoor, Facebook, Poshmark, eBay, or Amazon. I have two friends that make full-time livings selling clothes on eBay and Poshmark so I know you can make a few bucks just doing it in your spare time.

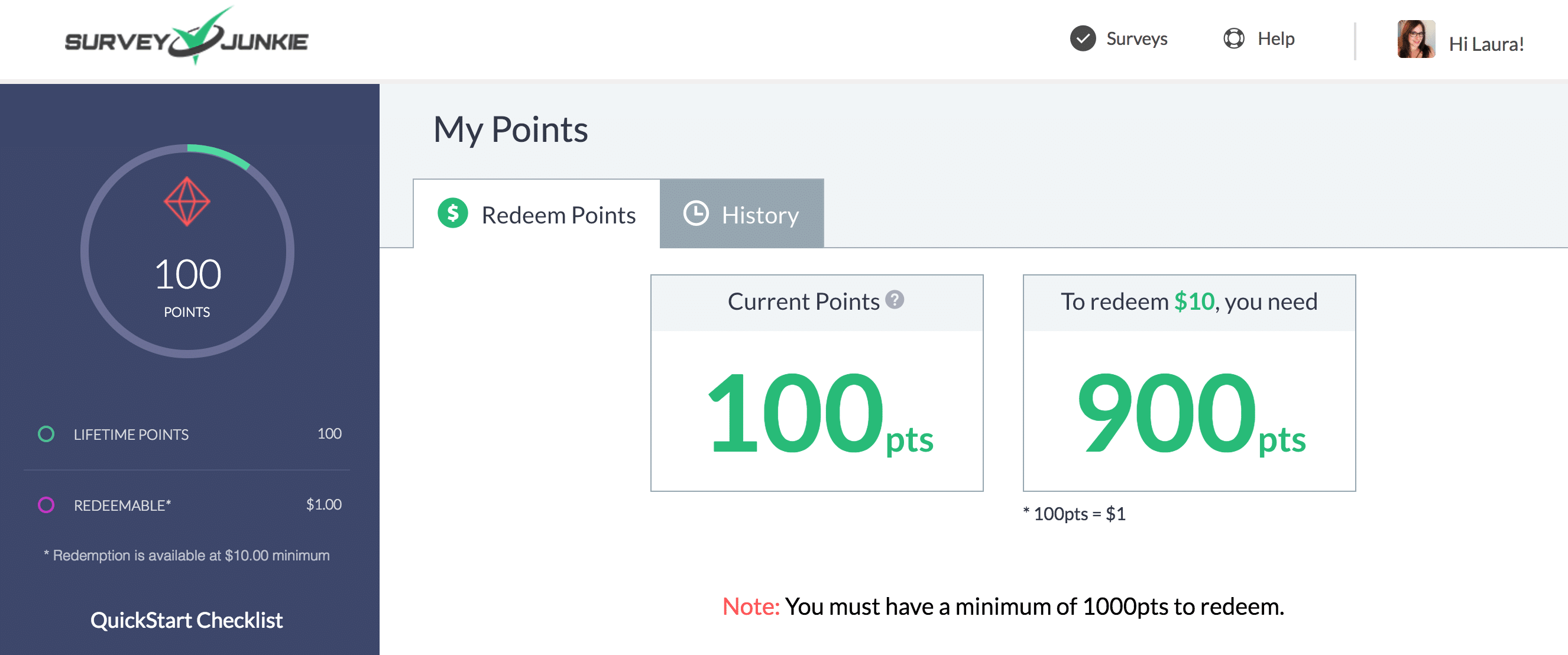

Use the time you need to kill to take online surveys in exchange for cash or gift cards. Survey Junkie is our favorite.

You have at least one skill that someone is willing to pay for on Upwork, a freelancing site. You can write, do graphic design, manage social media accounts, become a virtual assistant, and dozens of other things. Make a profile and start applying.

Oh, you don’t mind 3D life? Okay, you can get out of the house to make your extra money. Drive for Uber or Lyft. Take care of kids, elderly people, or pets through Sittercity.

Rent your house or a room in it on Airbnb. Get a part-time retail job during the holidays. Stores really need extra workers that time of year and are more flexible about scheduling. Or use the time-honored standby method of making extra money, waiting tables, and tending bars at night or on weekends.

We’re Rooting For You!

Phew! This was long, long to read, and long to write. But we wanted to give you everything you need to pay off your debt in one place so it’s as long as it needed to be to do that. And we know you’re serious because you’ve read this far!

We’ve given you actionable advice that you can start following right now to save money, reduce the amount and the cost of your debt, and make some extra money while you’re at it. That’s as much as we can do. It’s up to you to take the action. We really hope you will.

Being in debt sucks, I know because I’ve been there. It feels like scaling a mountain while simultaneously trying not to drown. But all it takes to escape that drowning feeling is to take the first step and then keep stepping.

If you need a cheering section, here we are! Head to the blog and subscribe, head to the podcast, and do the same. Come to the Facebook group and join the conversation. Once you’re out of debt, we have a ton of information on how to start growing your wealth.

Because the end of the line isn’t getting out of debt. It’s having enough money to give yourself complete freedom to live the life you want. We’ll be waiting for you at the end of the line.

Fiscal flexibility that’s funny, free and delivered weekly.

Current Project: Making bloggers money with Lasso.