Parenthood. Nothing in this world prepares you for it. You can read all the books on saving for college, check out all the blogs, and google until your fingers are numb, but until you’re trying to use that rare combination of force and tenderness, holding down your flailing toddler while you’re struggling to stop his third nosebleed of the night, you just have no idea.

And as you plop back into bed drenched in sweat and your child’s DNA, you start to regret all the grief you gave your parents growing up. But you also realize that there’s nowhere else you’d rather be and that there’s nothing you wouldn’t do for them.

And there are things you need to think about that you never gave a second thought to before. How will I teach them to be kind? How will I comfort them when someone breaks their heart for the first time? Even how will I keep them from taking on crippling student loan debt? It’s tough.

So here you are… with a little bit of savings and a lot of hope for the future, and you just want someone to tell you what to do to make certain everything turns out alright. Well, I can’t do that. But there are things you can do to give you options when the time comes, and that is about all you can do.

Yep, nothing in this world prepares you for being a parent, but what good things in life are you really 100% ready for? Saving for college? Pshaw. You’ve got this. You’ve caught throw-up in your bare hands!

So Many Unknowns

I have a hard time deciding how many bananas to buy for the week. How in the world do I decide how much my budding family is going to need for college in 18+ years? Or even if any of them will be going to college at all?

In-state public college; out-of-state four-year private college; graduate school; scholarships; financial aid and work-study; even “free college for all” or the tuition rates bubble bursting. It’s enough to make your mortarboards spin. But it doesn’t have to be that complicated.

Fiscal flexibility that’s funny, free and delivered weekly.

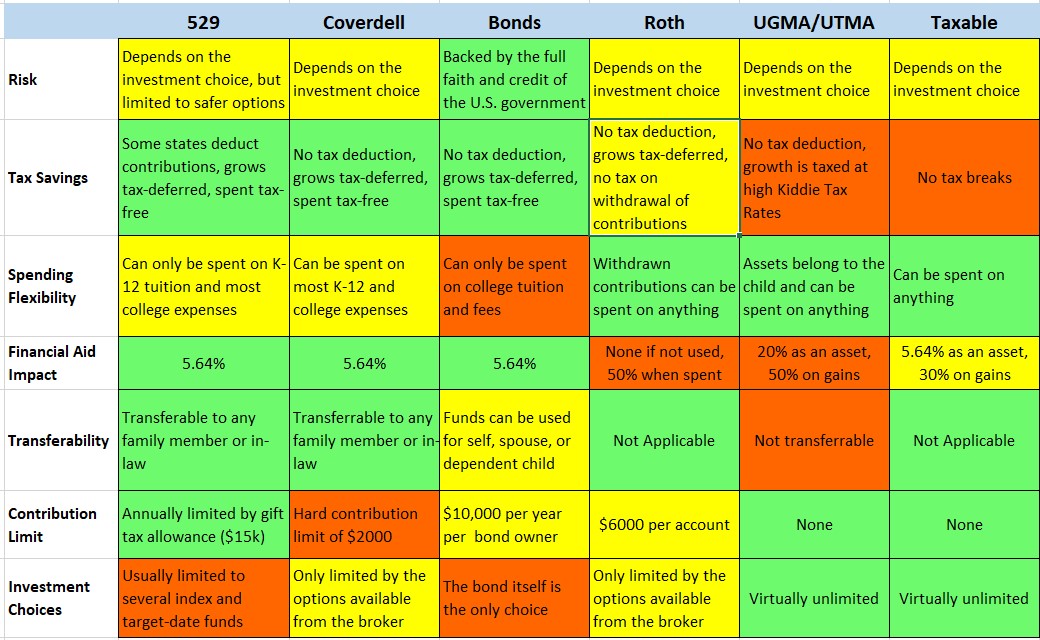

Strategies at a Glance

- Green=strength

- Yellow=neutral

- Red=weakness

Save for Retirement First

Don’t save for college if you haven’t started building retirement savings. Whether it’s your career or your body, one of them is going to stop working eventually. If you get there with nothing saved up, you’re toast… old, cantankerous toast.

Though not ideal, your child can take out loans for college if they have to. Retirement loans don’t exist.

I mean talk about “amortization”! (*rimshot, thank you, I’m here all week at the lender convention). And now rather than the burden of school loans, your kid has the burden of supporting you.

And not to be morbid, but if you “matriculate” to that “ivy league in the sky” on “early decision” in that freaky air-quote mishap, your inherited retirement funds can pay off those student loans right quick.

Saving Something is Better than Nothing

Every penny you save for college is a penny that you’re not going to have to pay interest on in a student loan. Think of loans as negative investment returns.

Even if you pay every tax and every penalty of your college savings account because your child wants to attend the “School of Life” (which is not accredited, FYI), that is only on the gains. No gains, no taxes, no penalties.

Avoiding saving because there’s a chance you might have to pay taxes or penalties on gains is like refusing a free car because you might get a speeding ticket. And, yes, there is an opportunity cost. But for something as potentially beneficial as college, that cost pales in comparison.

Also, no one said you have to save enough to pay for everything. In fact, you probably shouldn’t. With so many variables and plans potentially changing between now and then, it might be better to be a little short than drowning in abundance.

Getting small student loans or your child working part-time wouldn’t be the worst thing to happen.

Every penny you save for college is a penny that you’re not going to pay interest on in a student loan.

Tweet ThisFactors in Choosing How

There are a lot of things to consider when choosing a way to save for college. And each of these things may steer you one way over another.

No one plan is going to have the best of everything or be able to suit all your needs, but you can decide what’s most important to you.

Risk vs. Reward

What’s the point of a college fund if it just sits there not growing? Well, growing your money involves risk, but usually the more risk, the greater the potential reward. Risk is everywhere whether we see it or not. And we make risk tradeoffs all the time without even knowing it.

The obvious one is investment risk. But there are others when thinking about college savings that you should consider. And not all of them are bad.

There’s the risk of your child deciding not to go to college or that they get a ton of scholarships. Also, there’s a risk that your retirement funds aren’t what they should be or that unexpected medical costs arise. There’s even the risk that college education will be free for all in a couple of administrations. You never know.

And depending on your appetite for all the risks, it will likely be the biggest motivating factor of where you decide to put your college savings. The good news is that for all of them there are options.

Tax Favorability

While your college savings is growing, you probably want to also pay as little taxes on that growth as possible. Why not let Uncle Sam foot some of the bill? Your child is going to spend a lifetime paying him back anyway in increased tax revenue.

There are three ways to potentially save on taxes in college savings:

- Contribution Deduction: This means that you can exclude your contribution from taxes in the year you make it, potentially giving you more money to save.

- Deferred Taxes: This means that you don’t have to pay taxes on any investment income while it’s invested. Normally you have to annually pay taxes on things like interest and dividends if they are paid out as your investment grows.

- Distribution Tax Exemption: This means once you “cash-out” your investments, you don’t have to pay taxes on the distributions, including gains.

Some vehicles have some of each of these. Some have none. This is one of the biggest determining factors of how much money you will have for your educational needs.

Spending Flexibility

There are two factors within this category – how and when.

How you are allowed to spend the funds without penalty or taxes can be anywhere from extremely restrictive to completely at your discretion.

Do you only need the funds for college tuition or do you want to be free to spend it on anything, education-related or not? Also, do you want to limit what your child uses the money for?

When the plans allow you to use the funds can also be important. Do you want to be able to start using them as early as kindergarten? Do you mind deadlines for when you can spend it?

If you want to maximize financial aid, can you wait until later in college to use the savings?

Financial Aid Eligibility

Have you ever gotten rejected for a job because you’re “over-qualified”? You’re not going to wave your arms wildly yelling “No, I really suck!” But trying to qualify for financial aid is kind of like that. They say you have too much money, and you nearly jump out of your Gucci shoes claiming that you don’t.

Where your money is makes a pretty significant difference in how much financial aid your child will qualify for. A certain percentage of all the money you and/or your parents have and/or make is considered “available” for college and counts against financial aid.

Here’s a quick-and-dirty rundown of how much they expect of each type of funds.

- Student income: 50% (after income protection allowances)

- Parental Income: 30% (after income protection allowances)

- Student Assets: 20% – this is typically property and accounts in the student’s name

- Parental Assets: 5.64% – this does not include primary residence or retirement accounts

Adding a level of complexity is that for some assets, once you take distributions from them to pay for college, it counts as student income against financial aid.

Transferability

Admit it. You have more than one kid because you need a spare in case you mess up with your first. I’m kidding, of course. But in case you’re not, some plans make it much easier to transfer over your money to the one you actually love the most – or even to yourself.

This is probably the best way to mitigate the risk of your family’s plans changing. If you can transfer the money to another sibling, extended family member, or even yourself, you can potentially avoid taxes and penalties.

Contribution Limits

You may think that given your modest paycheck contribution limits will not apply to you. But you never know what the future holds. And there are savings methods with surprisingly low limits. So, before you commit to a plan, you should know what those are.

Also limiting the amount you can contribute to some plans is your income level. There are phase-out levels where between certain incomes you are allowed to contribute less. There are also income levels above where you are not allowed to contribute at all.

Investment Options

Do you want a wide variety of investment choices or just some basic ones that will do the trick? Do you want to put your ceramic Disney princess collection into your child’s college fund? There’s a plan for that.

Do you want to only invest in government-backed securities so that the only way you’ll lose money is if the U.S. stops being a country and diplomas mean nothing? There’s a plan for that.

Some of the following are strictly college savings vehicles. Some are just methods of general savings.

Depending on how dedicated to college savings goals the plan is, usually the more advantages it will have.

I will describe them from most favorable for college to least.

529 Plans

Tax Benefits and Qualified Expenses

This is the standard by which all other plans will be measured. 529 Plans allow for savings for the cost of college to be tax-deferred, and distributions are not taxed at all if used for qualified education expenses, including housing, meal plans, and computers.

You can also spend up to $10,000 on K-12 tuition and fees. Some states even offer a state tax deduction or credit for contributions.

However if not spent on qualified education expenses, the earnings are subject to regular income tax and a 10% penalty. This includes any leftover funds eventually removed from the account.

Transferability

One way to avoid having unused funds is to transfer the amounts to any family member of the beneficiary, which is fairly simple with 529 plans. And if you’re really good at using ancestry.com and can find a path to your plumber through various cousins and in-laws, through a series of transfers you could even give it to them!

Investment Options

You can typically buy investments within a 529 Savings Plan such as mutual funds and target-date funds with all the risks and rewards associated with them. But generally, the choices are limited to a small group of funds chosen by the institution offering the plan.

Financial Aid Eligibility

529 accounts owned by the parents (even if the beneficiary is the child) only counts as a parental asset at 5.64% against financial aid. If the student owns the account, it counts at 20% against financial aid (so don’t do that).

However, a big benefit is that, unlike other methods, distributions are not counted at all in future financial aid consideration.

Contribution Limits

Lastly, contribution limits for 529 plans are ridiculously high. They are normally set by the sponsoring state, but none are currently lower than $235,000 per beneficiary. And if you do hit the max, you may be able to open another plan in another state and keep going.

To read a more in-depth article about 529 Plans, click here.

Coverdell Education Savings Accounts

Consider the Coverdell ESA like the 529 Plan’s older sibling. They are the same in most ways but because you normally get one through a brokerage or other financial institution, they have some key differences.

As far as taxes are concerned, it is similar to a 529 plan other than the fact that there are currently no plans with a state tax deduction. But in the Coverdell’s favor is that it covers all K-12 qualified educational expenses, not just tuition and fees, with no $10k ceiling.

Also concerning financial aid, whether the account is owned by the parents or the student, it counts at the parental asset rate at 5.64%.

The Coverdell does have age restrictions. For one, you can only contribute to one until your child is 18. Also, all the funds must be spent by the time they turn 30. One way around the age limits is to change the beneficiary to a family member.

The biggest advantage over a 529 plan is that you can invest in almost any commercially available investment option like what you find at most brokerages. This includes individual stocks, bonds, and other securities.

The biggest disadvantage of Coverdell ESAs is with contribution limits. There is a hard annual contribution limit of $2000 per beneficiary from all sources. Also, there is a gross income limit of $195k for joint filers and $95k for single filers.

If you’d like to learn more about Coverdell ESAs, head here.

Education Savings Bonds

This used to be the go-to way for grandparents to help save money for their grandchild’s education, even before the tax exemption for higher education was implemented in 1990.

Just to be clear, there’s no such thing as a bond sold specifically for college. This is a program where if you use the proceeds from certain qualified U.S. savings bonds (post-1989, I and EE series) for higher education expenses the interest earned on them is tax-free.

The program only allows for the proceeds to be spent on tuition and fees, but even if you don’t use them for those, the interest is state tax-free. Plus, there is no penalty.

There are quite a few contribution conditions, however. First, only the parent can be the owner and they have to be over 24. Next, the maximum investment per year is $10,000 for each type of bond.

Lastly, you can only claim the full tax exemption if your income is currently below $117,250 for joint-filing couples and $78,150 for single filers.

There is no issue for transferals since there is nothing to transfer. The parent always must maintain control of the funds and can only use them for themselves, their spouse, or dependent. As such the bond is counted as a parental asset at 5.64% against financial aid.

The one area that savings bonds trump most other college savings plans is in its low risk.

U.S. savings bonds are backed by the strength of the United States government. But just like for my invitations to my family vacation slideshow, the interest rate tends to be quite low.

Roth IRA

But aren’t Roth IRAs for retirement? Well, just like the ad campaign from the 70s declaring that orange juice isn’t just for breakfast anymore, people are using their Roth IRAs to pull double-duty as a makeshift college savings option.

People figured out that since you could withdraw the contribution portions of a Roth IRA for anything at any time with no tax liability or penalties, you could save for retirement and have the option to use the contributions to help pay for school. The gains could remain in the Roth account for retirement.

If used for qualified education expenses, even the gains of a Roth IRA could be used for school. You would owe taxes on the gains, but the 10% penalty would be waived.

There are annual contribution limits of $6000 per account (2019) and income limits of $193k for joint filers and $122k for single filers to contribute this maximum.

The Roth IRA Financial Aid Paradox

How the Roth counts against financial aid carries both good and bad news. The good news is that while the funds sit there in the account, none of it counts against financial aid.

This is because you can exclude retirement accounts and primary dwellings from financial need calculations. But, and this is a big one (to Sir Mix-A-Lot’s delight but few others’), once you start using it for college expenses, it counts as a student’s income against any future financial aid.

One way to avoid that 50% hit is to wait until the second semester of your sophomore year to start using the Roth funds. This has to do with only needing to report income from 2 years prior on the FAFSA form.

The biggest advantage of this method is that if your child decides to forgo college, you still have a fully-funded retirement account. But if they do go to college, you’re potentially sacrificing your future retirement for it.

UGMA/UTMA Accounts

UGMAs (Uniform Gifts to Minors Act) and UTMAs (Uniform Transfers to Minors Act) are custodial accounts that behave like irrevocable trusts for a minor child. This means that whatever assets you put into it are no longer yours and will become the designated child’s at a certain age past 18.

This does two things. It shelters those assets from others and creates a taxable entity, which if you play your cards right, could save you some money in taxes.

However, gains over $2100 are now taxed at the “Kiddie Tax” rate, which is not as cute as it sounds.

These accounts aren’t specifically for education, so your child can spend the proceeds on anything they want once they reach a certain age above adulthood.

Also, you as the custodian could even spend it strictly for the benefit of the child before then.

As far as funding the account, it’s the great wide open. There is no contribution limit and virtually no limit on the type of investments you can use, including property and patents.

For financial aid, it is considered a student asset at the 20% rate. Also, the FAFSA application considers any realized gains, interest, and dividends on the account as income at the 50% rate.

With the application of the Kiddie Tax rules to UGMA/UTMA accounts the only real reason anyone would get one is if they’re pretty certain that college is not in the tea leaves for their child. It might come in handy if tea leaves are in your child’s future in the form of working as a barista, though.

Read our comprehensive article about UTMA/UGMAs here.

Taxable Investments

This is just about everything else. We’re talking about regular savings accounts, brokerage investment accounts, individual CDs, individual mutual funds, or that alpaca farm you’ve always wanted. As far as college savings are concerned, you treat them the same way.

As the name gives it away, there are no tax breaks for these. However, there’s some relief in the difference between short and long term capital gains.

And though in almost every other way this method has the most favorable status, it defeats the purpose of having a separate college savings fund. It’s like 10,000 spoons when all you need is a knife.

And wouldn’t it be ironic if you came to the end of this college savings article just to put your money back into a simple savings account?

You can spend it on anything… give it to anyone… put in as little or as much as you want… limitless investment options. All this and it still only counts as a parental asset at 5.64% against financial aid.

Though any income (interest, dividends) from these investments would count at the parental 30% income rate.

Summary

There is no one right way to save for college, and each has different advantages and disadvantages relative to each other. Which plan fits you best? If you want a little more help in choosing the right plan check out CollegeBacker. The key is knowing what matters most to you and what things you can live with.