- Is Renting Better Than Buying

- Monthly Rent Costs You More

- It’s the Principal

- How Does Escrow Work?

- Opportunity Costs

- Tax Benefits

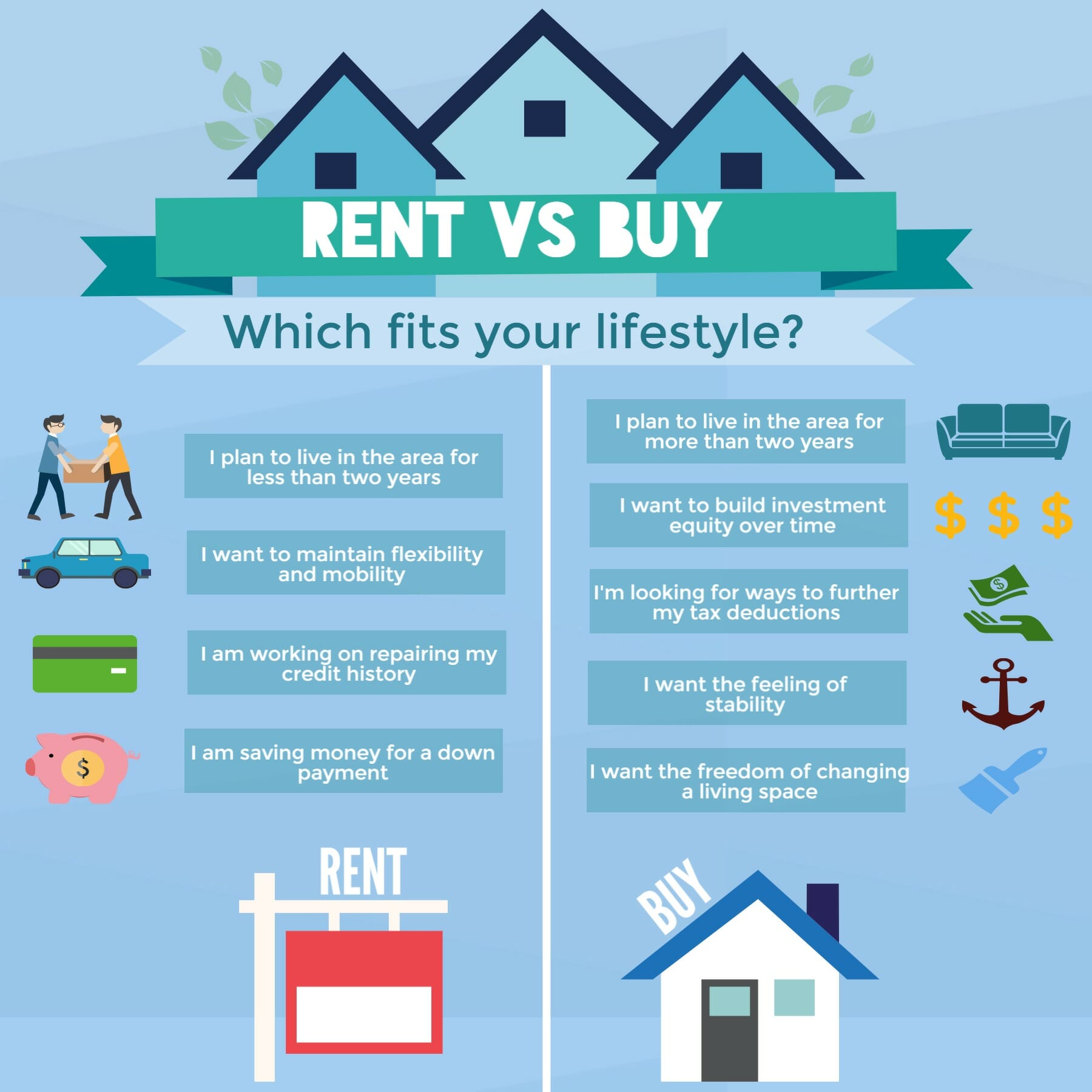

- Flexibility: Renting vs. Owning

- Price-to-Rent Ratio

- Why You Should Rent Instead of Buy

- Your Net Worth

- Location Location Location

- It’s Not Always About Money

- Bottom Line

- Show Notes

We’ve all heard the old saying that renting is like throwing money away. But is that really true? The rent vs. buy decision is one of the biggest money choices you’ll make. It’s not just about monthly payments – it’s about your lifestyle, your future, and your financial goals. Let’s dive in and see what makes sense for you.

Is Renting Better Than Buying

Owning a home was once the ultimate American dream—it meant you’d made it. But with high interest rates, low housing inventory, and intense competition, buying a home is harder than ever. Many people are choosing to rent instead, valuing flexibility, lower upfront costs, and fewer financial risks.

As of the fourth quarter of 2024, the U.S. homeownership rate stands at 65.7%. However, for those under age 35, the rate of ownership is significantly lower at 36.3%. This is about 55% of the overall homeownership rate in the US. While not at historic lows, these figures still highlight a notable gap in homeownership between younger Americans and the general population.

Millennials aren’t ignoring homeownership—they’re just adapting. With rising costs and changing lifestyles, many are choosing to rent. It’s not that they’ve missed the memo on the American dream; they’re just prioritizing flexibility and making smart financial choices.

Monthly Rent Costs You More

Many people argue that buying is better because one day you’ll pay off your mortgage and own your home outright. That’s true—but it doesn’t mean your home suddenly becomes free to live in.

Even after the mortgage is gone, homeowners still face ongoing expenses, including:

- Property taxes (which often increase over time)

- Maintenance and repairs (especially as the home ages)

- Homeowners insurance (which has been rising in cost)

- Possible HOA fees (for condos and planned communities)

As of 2025, homeowners spend thousands per year on these non-mortgage costs, which sometimes add up to nearly as much as a mortgage payment.

When you rent, these extra expenses aren’t your responsibility—your monthly payment covers most costs. However, rents can increase, while a fixed-rate mortgage stays the same.

The affordability of buying versus renting varies widely by location. In some cities, owning is the better deal, while in others, renting can save you thousands per year.

At the end of the day, the best choice depends on your financial situation, long-term goals, and lifestyle priorities.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

It’s the Principal

Your mortgage payment covers more than just the principal—it includes interest, and the bank isn’t lending you money out of generosity.

At the start of your loan, most of your monthly payment goes toward interest, not principal.

Here’s an example:

- A $200,000 mortgage with a 30-year fixed rate of 6.76% (current average rate) has a monthly payment of $1,299.

- First payment: $1,127 goes to interest, while just $172 reduces the principal.

- After 20 years: The balance shifts, with $662 going to principal and $637 to interest.

Other costs also impact your monthly mortgage payment. Most lenders require you to pay into an escrow account for property taxes and homeowners insurance, which can further reduce how much goes toward the principal early on.

How Does Escrow Work?

Your home isn’t just your investment—it’s the bank’s too. To protect their financial interest, lenders often require an escrow account to handle property taxes and homeowners insurance. Each month, a portion of your mortgage payment goes into this account, ensuring these important bills are paid on time. This prevents issues like tax liens or uninsured property damage, which could put both you and the bank at risk.

If you don’t pay property taxes, the government could place a lien on your home and even sell it to recover the unpaid amount. Without homeowners insurance, the bank has no protection if your home is damaged by a fire or natural disaster. Escrow helps prevent these scenarios by making sure the money is set aside and paid when due.

If your down payment was less than 20%, your lender might also require private mortgage insurance (PMI). This protects the bank if you default on your loan. PMI is added to your monthly mortgage payment, which means less of your money goes toward paying down the loan’s principal balance early on.

Keep it Flowing

For many people, their home is their most significant investment. But it’s not a liquid investment. A liquid investment is something that can be quickly converted to cash, like stocks or bonds, which can be sold right away.

If you need to get money from your home, you have a few choices. You could borrow against your home’s value with a second mortgage or a home equity line of credit (HELOC), or you could sell your house. But none of these are quick fixes. Getting a loan against your home usually takes 2 to 6 weeks.

Selling your house takes even longer, about 4 months on average. That includes about 2.5 months to find a buyer and another month to finish all the paperwork. Keep in mind, though, that how long it takes can change a lot depending on where you live, what the housing market is like, how you price your home, and what shape it’s in.

If you had to sell your home, you would have no control over the market. Imagine having to sell your largest investment in a down market.

Opportunity Costs

Opportunity cost is what you give up when choosing one option over another. Think of it like this: if you decide to eat out instead of seeing a movie, you miss the movie—that’s your opportunity cost.

When buying a home instead of renting, you face opportunity costs too:

- The money used for a down payment can’t be invested elsewhere.

- You lose the flexibility to move easily for new jobs or experiences.

- You spend time on home maintenance instead of other activities.

Recognizing these trade-offs helps you make informed decisions about what truly matters to you.

Tax Benefits

When it comes to tax breaks, homeowners still have more advantages than renters, but there have been some changes:

- Mortgage interest deduction: Homeowners can deduct interest on mortgages up to $750,000 for first and second homes combined. If your mortgage was taken out before December 16, 2017, the old limit of $1 million still applies.

- Property tax deduction: There’s a $10,000 cap on combined state and local tax deductions, including property taxes.

- Home equity loans: Interest on home equity loans is only deductible if the loan is used to buy, build, or substantially improve the home securing the loan.

- Origination fees: These aren’t usually tax-deductible, but points paid to lower your interest rate may be deductible over time, often spread across the life of the loan.

For renters, federal tax breaks are limited, but 23 states now offer renter’s tax credits or deductions. These often depend on factors like income, age, and how much rent you pay.

Tax laws can change, and individual situations vary. It’s always best to consult a tax professional for advice tailored to your circumstances.

Flexibility: Renting vs. Owning

Renters have a clear advantage when it comes to flexibility. If you need a bigger or smaller place, want to save money, or relocate for a new job or lifestyle, renting makes it easy. Most leases last a year, but if needed, you can often move sooner—though breaking a lease might come with penalties.

On the other hand, homeowners face more obstacles if they need to move. Selling a home takes time, involves costs, and depends on the housing market. This makes relocating much harder than simply ending a lease and finding a new one.

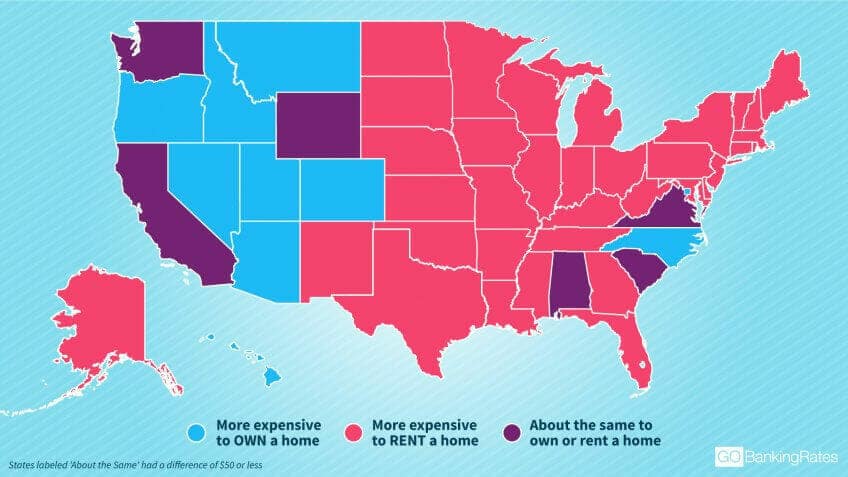

Price-to-Rent Ratio

The price-to-rent ratio helps compare the costs of buying vs. renting in different areas. To calculate it, divide the median home price by the median annual rent. For example, if a $100,000 home rents for $1,000 per month, the ratio is 8.33 ($100,000 ÷ $12,000).

This ratio factors in homeownership costs (mortgage, property taxes, insurance, HOA fees) and renting expenses(monthly rent plus renter’s insurance). It also considers tax benefits for homeowners.

How to interpret the ratio:

- Below 15: Buying is typically more cost-effective.

- Above 15: Renting might be the smarter choice.

Here are some real-world price-to-rent ratios in major U.S. cities:

- San Francisco, CA – 37.3, making renting the more affordable option.

- San Jose, CA – 37.6, one of the highest in the country, favoring renting.

- Houston, TX – 15, suggesting that buying could be a better financial decision.

These numbers fluctuate based on market conditions, so always check current housing data before deciding whether to buy or rent.

Why You Should Rent Instead of Buy

For many, a home is their largest purchase, but is it a good investment?

Why Renting Still Makes Sense

- Lower Costs – No down payment, closing fees, property taxes, or maintenance expenses.

- More Affordable – As of early 2025, buying is 34% more expensive than renting on average.

- Flexibility – It is easier to relocate without the hassle of selling a home.

Why Buying Could Still Be Worth It

- Home Values Are Rising – Prices increased 3.9% annually in late 2024. Over the past 25 years, U.S. home prices have experienced an average annual increase of approximately 4.4%.

- Long-Term Investment – Homeownership builds equity over time.

- Tax Benefits – Mortgage interest and property tax deductions can reduce costs, but limitations may apply based on your tax profile and whether you itemize deductions.

The Bottom Line

- Mortgage rates remain high at 6.76%, making homeownership costly.

- The S&P 500 has delivered 10.39% annual returns (1926 to 2024), historically outperforming real estate.

- The decision depends on your financial situation, goals, and market conditions.

A good investment puts money into your pocket, while a liability takes money out. Homeownership incurs expenses like property taxes, maintenance, and insurance even after paying off your mortgage. These ongoing costs can make owning a home more of a liability than an investment.

The New York Times has a helpful rent vs. buy calculator if you want to run the numbers yourself.

Your Net Worth

Your net worth is the difference between what you own and what you owe. When buying a home, aim to keep its value below 30% of your net worth. This helps spread your wealth and lower financial risk.

Diversification matters. Just as you wouldn’t invest most of your portfolio in one stock, avoid tying too much of your wealth to a single asset, like your home. A balanced approach helps protect against market shifts and strengthens your financial foundation.

When determining how much of your net worth should be invested in your primary residence, financial experts often recommend that your home’s value comprise between 25% and 30% of your total net worth. This approach promotes diversification, reducing the risk associated with having too much wealth tied up in a single asset. Maintaining this balance enhances your financial flexibility and resilience against market fluctuations.

It’s important to note that these percentages can vary based on individual circumstances, such as age, income, and overall financial goals. For instance, first-time homebuyers might initially have a higher percentage of their net worth invested in their homes, but the aim should be to diversify over time. I’d like to point out that regularly assessing your asset allocation makes sure that your investment strategy aligns with your evolving financial objectives.

Location Location Location

The price-to-rent ratio is a good starting point when deciding whether to rent or buy, but it’s only part of the picture. The local job market matters—if the area depends on a single industry and that industry struggles, you could be stuck with a home you can’t sell and fewer job options.

School districts also play a big role. Even if you don’t have kids, homes in good school zones tend to hold their value better and attract more buyers when it’s time to sell.

Think about everyday convenience, too. Proximity to grocery stores, healthcare, public transportation, and recreation can improve quality of life and boost long-term property value.

Future development is another factor. New roads, shopping centers, or zoning changes can either enhance an area’s appeal or make it less desirable.

By considering these factors alongside the price-to-rent ratio, you can make a well-rounded decision that supports both your financial future and lifestyle.

It’s Not Always About Money

We’re all about money at LMM, but not every decision should be based solely on financial factors, including deciding whether to rent or buy a home. If we only looked at numbers, no one would ever have kids since raising them is rarely a financial win!

There are plenty of valid reasons people want to own a home—establishing roots, raising a family, avoiding the uncertainty of renting (which has become a growing issue in some cities where landlords prioritize short-term rentals like Airbnb), or simply wanting the freedom to customize a space in ways renting doesn’t allow.

There’s nothing wrong with any of those reasons. However, you can’t ignore the financial side of homeownership. You can buy a home, but that doesn’t mean you should max out your loan or purchase the most expensive house you qualify for.

In 1973, the average new single-family home was about 1,660 square feet, and the typical household size was 3.01 people. Household sizes have shrunk to about 2.63 people, but homes have ballooned to an average of 2,687 square feet. That’s over 1,000 extra square feet per home! Buying more space than you need increases costs and often encourages unnecessary spending just to fill the extra room.

Ultimately, homeownership should be a balance between financial responsibility and personal goals. By making an informed decision, you can ensure that buying a home aligns with your lifestyle and long-term financial well-being.

Bottom Line

Buying a home to live in isn’t always the best investment, but owning real estate as a landlord can be a smart way to build wealth. Renting out a property while continuing to rent your own place generates passive income and avoids the financial burden of homeownership.

By treating real estate as an investment, you gain property appreciation and rental income while keeping your finances flexible. You’re not tied to one location, giving you more freedom to live where you want. In 2025, real estate remains a powerful wealth-building tool with long-term financial stability.

Show Notes

5 Year Adjustable Rate Mortgage: This is the mortgage that Andrew is leaning towards.

I Will Teach You To Be Rich: A great personal finance book.

The Simple Dollar Book: Long is considered a PF classic.

Betterment: The easy way to invest.