Not all of us make six figures which means paying off debt can be tough. But it’s not impossible. We’ll show you how to get out of debt, even on a low income.

At LMM we tell you that your debt is an emergency. And like any emergency, the longer you wait to deal with it, the worse it gets.

So you can’t wait for the next big raise, the next new job, the winning lottery numbers to help you tackle it and show you how to get out of debt.

You can tackle it right now. Don’t let the emergency get worse. You don’t have to be making big money, or even more than you are making right now to at least start paying off debt.

Cost of Debt

If you already have debt then probably one of your biggest monthly expenses is dealing with that debt. That sucks and you’ve gotta do something about debt management ASAP.

The best way is to just get the people you owe money to forgive some of what you owe. Sounds crazy but it works surprisingly often – to the tune of billions of forgiven dollars a year.

Imagine if you owed $10,000 and told your credit card company that you can only pay back $3,000 or you’ll have to declare bankruptcy and in turn pay none of it.

They would rather get something over nothing and will either flat-out agree or come up with a counteroffer like $6,000.

Either way, it’s a free debt reduction and all you need to do is call your credit card company. Or, if you’re unsure of your negotiation skills just bring in someone like National Debt Relief.

Their cost is roughly 25% of the amount of debt they get forgiven so it’s a pretty low-risk deal since it costs you nothing if they can’t help.

Credit card companies will forgive some of your debt if you’re in trouble. Get a $10,000 bill reduced to $4,000 just by asking. National Debt Relief negotiates on your behalf.

Cutting Costs: The Big Stuff

If you’re buried under thousands of dollars in debt, merely making coffee at home and packing your lunch for work won’t suffice to rectify your financial woes. While these are valuable habits, they’re not the complete solution. It’s crucial to focus primarily on reducing your major expenses.

Reduce your interest rate

If you have credit card debt, your interest rate may be above 20%. In that case, you can easily refinance with Upgrade and get a low rate.

It’s shockingly easy so if you’re a hardcore procrastinator then just give yourself 15 minutes to create some breathing room in your monthly budget.

Upgrade offers personal Loans up to $50,000 with competitive and low fixed rates and fast funding. A personal loan can help you eliminate high-interest credit card debt, streamline your credit or upgrade your life with a fixed-rate loan instead of a high-interest credit card.

Housing

The rule of thumb is that your housing expenses should be no more than 30% of your income. But not all of us are adhering to this rule. More than a quarter of Americans are paying 50% of their income on housing. If you’re among them, it will be almost impossible to get out of debt and start saving for your future.

Even if you are at 30% or under, if you have debt, this needs to change. You have a couple of options; find a cheaper home, get a roommate, move in with your parents, or move to a place with a lower cost of living.

Moving towns may not be practical for everyone, but if you’re living in an area where housing costs are prohibitive, and you’re in a profession where you’re not ever going to be making enough money there to get under that 30%, it’s something you need to consider.

I know it’s fab to live in New York City or Los Angeles or San Francisco but if you’re going to be forever in debt and never able to retire, it’s not worth it. I know it takes money to move so you can choose from our other options; finding a cheaper place, getting a roommate, or moving back in with your parents until you’ve saved enough to make a move.

If your debt is not that high or if you’re in debt now but your career and salary will advance within your field, you don’t have to do anything as drastic as pick up and move, but you still need to cut housing expenses so consider those options mentioned above, but you can also consider another.

If you’re in a desirable location, rent your place out to Airbnb. Even if you just crash with a friend for one weekend a month, you could bring in a couple of hundred extra dollars, and that will go a long way to paying off your debt.

How much you can make with Airbnb varies based on a lot of factors (location, listing type, and pricing strategy), but Airbnb hosts average.

Transportation

Getting from place to place is likely our second most significant expense. Even if you are lucky enough to live in a city with good public transport, it’s still not free.

A monthly Metro Card for the NYC subway is currently $132.00. That might seem like a bargain if you are paying a car payment and the cost of gas in the burbs, but remember, NYC’s cost of living is expensive!

Some employers subsidize the cost of a public transportation pass or allow you to use pre-tax money to purchase one. Ask your HR department if they have any such programs available.

Experiment for one week, if you are a two-car family, have your partner do the same. Write down every car trip you make. At the end of the week, go over the list. Can some trips be cut out by planning errands more efficiently? Any trips that could be made by bike or by foot?

How many trips could you and your partner combine? Can you carpool to and from work?

If you’re a two-car family who is struggling with debt, cutting down on one car can make a big difference. It might be painful but your debt is an emergency.

It’s convenient to have two cars but how is it necessary? What would you do if one car was totaled and couldn’t be replaced right away? Do that and sell the other car. Not only will you get rid of a car loan but the cost of insurance too.

Walking or biking to work has benefits beyond just saving money too. More exercise, less pollution, less aggravation. When I worked in an office, I always walked to and from work. Sometimes as much as 45 minutes each way and in all kinds of weather. Such was my mania to avoid giving the MTA one cent I didn’t have to give their crummy service. And to save money of course.

Food

If you keep a budget, and you should, you’ll probably see this category as one of your biggest money hemorrhages. If you aren’t tracking your spending, start now. You’ll likely be surprised and maybe horrified at how much you spend here (take a look at Mint for budgeting).

An excellent free budgeting tool. I use it, and if you're getting started, you should too. If you don't track your spending, you'll never know where you're wasting money.

Maybe you don’t like to cook; some people don’t. How have you been eating out a lot? You probably also don’t like cleaning, doing laundry, or running errands. But you still do it because it’s part of being a grown-up. Think about it; you could outsource those other things like you’ve been outsourcing feeding yourself.

Eating habits aren’t so different; it’s time to make a change! While I won’t insist you must always eat healthily, though it’s beneficial, you can still choose affordable options. Stock up on frozen dinners during sales, grab some Ramen, or whatever fits your budget. The key is to begin preparing meals at home and bringing your lunch to work.

Once you’ve eaten your kitchen clean, you’ll need to go food shopping, and you’ll need a meal plan. Planning out your meals for the week not only keeps you from buying things you don’t need, but it’s what makes it possible to batch cook.

Batch cooking just means cooking a lot of food at once, so you have leftovers for work lunches and for later in the week.

Before you plan your menu, sign up for Ibotta. Ibotta brings coupons into the 21st Century. It’s an app that gives you cash rebates right from your phone. They have partnered with stores all across the country to offer products at discounted prices.

Once you’ve purchased the selected products from participating stores, simply take a photo of your receipt and upload it to the app. The app will then match the items you purchased with available rebates and deposit the cash back into your Ibotta account within 48 hours.

We’re trying to save money but if you don’t already have one, buy a slow cooker. They make batch cooking easy because once the food goes into the stove, you don’t have to do anything else.

Of course, you are going to go out to dinner sometimes, and that’s okay as long as you have budgeted money for it. Use the app Seated to make reservations. Each time you complete a reservation, you get a $15 credit for Uber, Amazon, or Starbucks.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

Understanding The Whole Picture

First things first: it’s crucial to take stock of your financial situation. Sit down and calculate precisely how much you owe, your outgoing expenses, and your incoming funds. If you haven’t yet created a Personal Capital account, doing so is a wise step. It offers the simplest method to gain a comprehensive overview of your finances.

Personal Captial has free financial software and tools to track your personal finances. You can easily manage your entire financial life in one place and reach your financial goals faster.

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.

Their software will help you develop your long-term financial strategy, calculate your net worth, set a budget, manage investment accounts, and plan for retirement.

It might be a little scary to tally up how much debt you owe, but it’s the first step in eliminating it. Compare how much is going out (all of your monthly bills and expenses) and how much is coming in (all of your income) just using the minimum payments on the debts, not the totals.

Cutting Costs: The Small Stuff

This is only for those people in debt. If you’re just looking for more money to invest or save, I don’t like to advise people to watch every cent and never buy little things like coffee on the way to work. But if you are in debt, emergency.

So you’re going to have to watch those little purchases that add up. Go through the expenses in Mint, as mentioned earlier. It’s this little stuff that can add up and that can be eliminated when you have a debt to pay off.

Daily Habits

The habit of buying coffee daily often receives criticism, and in my opinion, it’s justified. Don’t you have a coffee maker at home?

So I don’t understand people who swear they can’t function without coffee but manage to shower, dress, and leave the house before they buy some of the way to work. No more Starbucks (unless it’s from Seated).

Even if you’re a coffee snob, buy the best machine, beans, or whatever else you require, and make it at home. You will still be spending less. But really, Café Bustelo makes a tasty cup of coffee and the price is reasonable. Get over yourself!

Coffee is an easy target for this kind of spending, but it manifests in lots of other ways. Magazines at the checkout line, drink when you get gas, a new lipstick. None of these things alone will break you, but chances are, more money than you realize is going into this sort of stuff. Money that should be going into debt.

Shopping

Nearly everything available can also be purchased second-hand, often at a significant discount. If you live near affluent neighborhoods, consider visiting their thrift stores. Wealthy individuals frequently donate items, some of which may be unused, unworn, or still in their original packaging.

From clothing and appliances to kitchen gadgets, thrift stores are treasure troves of affordable finds. Admittedly, finding what you need may require more time as you sift through assorted items compared to the convenience of shopping at stores like Target. However, the savings you’ll enjoy are well worth the extra effort.

You shouldn’t be doing any clothes shopping, but if there is a wedding or similar event and you don’t have anything to wear and need something nicer than you can find in a typical thrift store, you can check out Poshmark which sort of online thrift store. You’ll find higher quality items, but the prices are still affordable.

You can also save money when you join Swagbucks, you can get cash back when you buy online from more than 1,500 retailers including places you probably already shop like Amazon, Target, and Starbucks. You earn points for each dollar you spend and also get exclusive coupons and deals exclusive to their shoppers.

You can redeem your points for gift cards or get cash back through PayPal. We did an in-depth review of Swagbucks. There are other ways to make money on the site too.

Receiving automated refund checks is great, it’s like finding money on the ground. As it turns out, stores owe you money all the time, but they don’t pay if you don’t ask. That’s where Dosh comes in. Dosh gets you automatic cash back at thousands of places when you shop, dine, or book hotels. No coupons or receipt scanning. Simply download the app or find us in your favorite ways to pay.

Dosh gets you automatic cash back at thousands of places when you shop, dine, or book hotels. No coupons or receipt scanning. Simply download the app or find us in your favorite ways to pay, like Venmo or Jelli. It’s awesome.

Subscription Services

You might be spending money and not even realize it. That old gym membership, the magazines still being delivered to your last address because you never updated it, the fruit of the month club. It’s a hassle to cancel all those things, but it’s worth it.

You don’t have money to be throwing away even if it’s $8 here and $15 there. But now, you don’t have to do the work to save the money! Create an account with Rocket Money. They will identify subscriptions to stop unnecessary payments and cancel unwanted subscriptions.

The Medium Stuff

Some specific products and services have so many providers that we probably aren’t getting the best deal we could. It pays to shop around.

Utilities

How many television shows do you watch? It’s probably just a handful sprinkled across just a few channels. But you’re paying for dozens and dozens of channels if you’re paying for cable.

Become a cord cutter.

There are all kinds of internet services you can use to watch the shows you like, Amazon, Hulu, Netflix, and Sling TV, and at a fraction of what you’re paying for cable.

If you have auto or homeowner’s insurance you should shop around for the best price. There are so many insurance companies competing for your dollar that you probably aren’t currently getting the best deal you could. You can use Policy Genius to shop around.

Interest Rates

If you have student loans, you may be able to get a lower interest rate by refinancing. Credible is a platform that uses technology to bring low-interest loans to high-potential people. They look at things like your savings patterns, investments, and career trajectory—to give you the lower rate you deserve.

If most or all of your debt is credit card debt, you know how hard it can be to ever make any progress when the interest rates are so high. Getting that interest rate down will save you money and enable you to get out of debt more quickly. There are a couple of options for getting your credit card interest rates lowered.

The best option is a balance transfer credit card. You open a new credit card that has a period of 0% interest; some offer that rate for as long as 24 months. You transfer the balance from your current high-interest cards onto the new card. You have that period to pay only the balance on the card with no interest charges.

You must pay off the entire balance before the 0% APR period ends though. If you don’t, the remainder will be subject to the new interest rate which could be higher than the price you were paying on the previous card.

Not everyone will be approved for a balance transfer card but if you are, indeed buckle down and get that balance paid off.

If you can’t get a balance transfer and get a debt consolidation loan from Credible.

People lend you a lump sum that you can use to pay off your credit cards. A loan like this does have an interest rate (that’s how the lenders make a profit), but it will be far less than the interest rate on your credit card.

If you’re not eligible for any of the above, call up your credit card companies and ask for a reduced interest rate. Be honest, tell them you’re struggling with the payments, but you have a plan to pay off your debts but could use some help in the way of a lower interest rate. Not all of them will agree, but you might get lucky, so it doesn’t hurt to ask.

Fees

There is so much competition between banks that you should never pay any bank fee; a low balance fee, maintenance fees, ATM fees, or overdraft fees. Part of the way banks make money is by nickel and diming customers with these little charges.

Bust the banks by switching to an online bank like Chime. Chime has virtually no fees. When you join Chime, you’ll be sent a Visa-branded debit card which is connected to your Chime spending account.

Not only do you avoid annoying bank fees, but the Chime card is also a cash-back rewards card. Rewards are something traditional bank debit cards don’t offer so all the more reason to switch to Chime.

Make Some Extra Money

It’s easier to cut spending than make more money but making more money usually generates more significant numbers and if you’re in a lot of debt, working only one job unless you have significant family commitments is not an option. You need to have at least one additional income stream until you are out of the woods.

Work Some Overtime

This won’t be an option for everyone but if you’re paid hourly, speak to your boss and see if you can pick up a few extra hours. Or if you’re job has shifted, check if the less desirable shifts pay a bit more per hour. Working nights isn’t fun, but it could make you some extra money without doing any more work. Maybe less if there’s no one watching!

Take A Part-Time Job

Do you have weekends free or a few hours in the evening? This might not be realistic if you have a family, but if you’re single, put your social life on hold for a few months and pick up a part-time job. Even if nothing is available now, lots of retailers take on extra workers around the holidays.

Start A Side Hustle

This doesn’t have to be anything complicated. If you want to grow your own business, great, but if you just need some extra cash, you have lots of options. These kinds of side gigs offer a lot of flexibility that a traditional part-time job doesn’t.

Do you like kids? Make babysitting your side hustle by signing up with Sittercity! Parents post jobs on Sittercity for everything from a full-time nanny to the occasional date night sitter. You can apply to the postings, meet the family, and get hired. The average pay for a sitter is a little over $12 an hour.

Drive for Lyft. The hourly pay after expenses varies from city to city, but you can expect to make around $15.57 an hour. In larger cities, it will often be much more, and in smaller cities, sometimes a little less.

The appeal of Lyft is that you can set your schedule and there is no commitment. You can work your regular job and make your $100 in just a few hours on a weekend or some evenings.

Selling your extra stuff, stuff you buy cheap at garage sales or discount stores, or selling things you make is a great way to make extra money. You don’t have to go to the trouble of having your garage sale. You can do it all online.

Shopify is a site that makes selling stuff easy. They have ready-made templates, so you don’t have to spend time designing your store. They also have a lot of tools to help you do things like create coupons and promotions, process payments, handle returns, and share your store on sites like eBay, Google Shopping, Facebook, and several price comparison sites like Nextag, Bizrate, and PriceGrabber.

Just spending a few hours a week on your Shopify store can pay off.

Hustle in Your Downtime

When you’re paying off debt $2 here and $3, there can help. Don’t turn your nose up at those little amounts. These are some great ways to make a few extra dollars or save a few extra dollars in your spare time. And you have a lot of it since you’re not going out spending money.

Want to get paid for your opinion? With Survey Junkie you share your view to help brands deliver better products and services. Once you build your profile, they will start matching you to surveys.

When you complete the surveys, you will earn virtual points that can be redeemed for PayPal or e-giftcards. You can take online reviews anywhere, anytime, and on any device.

Most of the surveys are pretty easy, and you are not required to sign up for other services so no annoying spam mail. For starters, it’s entirely free, and you earn 25 free points just for creating your account. We did a full review of Survey Junkie.

Mechanical Turk is an Amazon site that pays small amounts of money for completing simple tasks like looking at an image and describing it in fewer than ten words. It takes some time to find jobs worth doing, but you can check it out while you’re sitting around watching Netflix.

Grow Up And Budget

To create a personal budget, start by ensuring your income exceeds your expenses. How much money remains at the end of each month? This surplus is what you initially have available to start reducing debt. Your goal should be to increase this amount, and you will, but it’s helpful to know if there are some extra funds available after covering all expenses.

What if there is more going out than coming in? We’re going to fix that. That can happen when you start relying on credit cards and is probably at least part of the reason you’re in debt.

Keeping Track of Your Budget

Now that you’ve gathered all the necessary numbers, you’re ready to dive in. You’ve identified the total debt, outlined your expenses, and listed your income. The next step is to consistently monitor your budget, ensuring we stay on track with your financial goals.

Your Debt – Make sure to account for the minimum payments on your debts, which ideally, you’ve been managing to pay. If you’ve fallen short of making these minimum payments, it’s crucial to incorporate them into your budget immediately (remember your credit score).

Discretionary Spending Allowance – Additionally, it’s important to allocate funds within your budget for discretionary expenses, such as dining out, movie nights, or enjoying a few drinks during happy hour.

Getting out of debt – This is your main goal, and your budget is the way to achieve this while still living life. Strict cost-cutting non-stop isn’t realistic—we’re human, not robots and occasional treats prevent burnout. By allocating a small part of your budget for fun, we maintain motivation without derailing our primary objective. Alongside, we’ll identify savings and earning opportunities to accelerate debt repayment, ensuring a balanced approach to reaching financial freedom.

Don’t Let It Happen Again

Now that you’ve got a handle on what’s coming in and what’s going out, aim to spend less than you earn. It’s a simple but powerful way to keep your finances in check and save up for the future.

Stay on Top of Your Debt!

If you’re worried about overspending on your credit card, Cushion offers a solution. It simplifies the way you organize, pay, and build credit using your current bills and Buy Now, Pay Later plans. With Cushion, all your recurring payments are managed from one dashboard, giving you unparalleled control.

Here’s how it works: By securely linking your accounts to Cushion, its AI technology will automatically detect and arrange all your bills for easy management.

You can set financial goals and monitor your progress directly through the platform. Should you choose to increase your monthly payments, Cushion illustrates how this decision could expedite your payoff timeline and the amount of money you might save in the process.

80% of people save money by using Rocket Money to find and cancel unwanted subscriptions! With Rocket Money, you can also effortlessly track your spending, easily lower bills and track your net worth.

Now Make Your Plan

You know how much is coming in and going out. You’ve reduced some of your expenses, and you have some extra money coming in. Set up your budget in Mint and stick to it. Check it every week to see how much you have left to spend in each category.

In your initial budget, you allocated only the minimum payments for all your debts. Now, it’s time to develop a strategy for paying them off. Randomly distributing money across the balances isn’t an effective way to eliminate debt.

Paying Down Your Debt

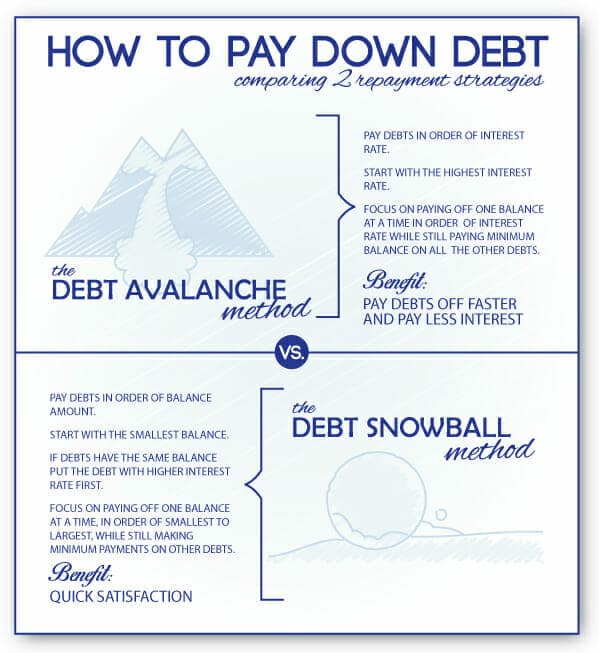

Two efficient methods for paying down debt quickly are debt snowballing and debt stacking (also known as debt avalanche) techniques. There is a full explanation of both methods here.

Debt Snowballing – Paying debts from smallest to largest. Pay extra on the smallest debt, minimum on others. Once a debt is paid, its payment goes to the next smallest, speeding up the process. It’s motivating because you see quick progress.

When one credit card balance is paid, you take the money you were paying for it and start paying it on the next on the list until it’s paid off. You continue doing this until all the debts are paid.

Debt Stacking (avalanche) – Tackling debts from highest to lowest interest rate. Pay extra on the highest interest debt, while making minimum payments on the rest. Once the highest interest debt is cleared, focus on the next highest, saving more on interest and reducing debt faster.

Which Method is Better?

Picking how to tackle your debt—stacking (going after high-interest debts first) or snowballing (knocking out the small debts first)—is really up to what feels right for you.

Stacking saves you cash on interest, but snowballing gives you quick wins that feel awesome. Either way, you’re taking it one debt at a time, which makes everything seem way more doable. It’s like losing weight bit by bit instead of all at once.

How Do I Track This?

- Decide which method you are going to use – Make an Excel spreadsheet or Google Sheets (or a good old notebook) to list all of your debts and each payment you make. It’s pretty rewarding to watch those numbers drop with each payment you make.

- Set a realistic deadline for paying off your debt – While you aren’t going to clear $20,000 in two months on a modest income, avoid stretching the timeline too far. Giving yourself too much time, like ten years, isn’t practical either. Aim for a balance that motivates progress and is achievable.

- In your spreadsheet/notebook –

- Set up a weekly payment schedule in your spreadsheet

- After each payment, update the balance to track your decreasing debt, which helps maintain motivation.

- Don’t schedule payments for future debts yet; this approach gives you the flexibility to possibly pay off each debt earlier by adjusting as you progress.

- Regularly review your progress – Adjust your repayment plan as needed, and don’t be afraid to change how much you pay towards each debt based on your situation.

How Much Should I Pay?

- Calculate your available funds (from your budget) – This is your “extra money“.

- Use the entire “extra money” to pay the debt.

- Flexibility and Consistency are key – Remember:

- Minor adjustments are acceptable: You can customize the snowball and avalanche debt repayment strategies by adjusting extra payments as needed, depending on your motivation and how you’re progressing.

- Be prepared for unexpected events: Expect the unexpected so it’s okay to hit “pause” or tweak your extra payments when unexpected costs pop up. Just make sure to keep up with the minimum payments on all your debts.

- Consistency is key: Making at least the minimum payments consistently, even if small, is crucial for avoiding financial hardship and maintaining progress.

Paying off debt is motivating, but avoid using credit cards while doing so. Don’t close credit cards as this can hurt your credit score. Instead, keep them active by putting a small, recurring payment (like a utility bill) on each and setting up automatic payments. This helps you avoid debt and keeps your credit score healthy.

It Won’t Take Forever

None of these strategies seem particularly enjoyable or effortless. The idea of downsizing your living space, skipping your daily coffee run, and dedicating many weekends to working isn’t appealing. But remember, you are treating this as an emergency.

You’ve crafted a plan, you’re embracing sacrifices, and you’ve found ways to bring in additional income. Stick with it. Encountering a rough day or week is no reason to throw in the towel. Accumulating debt didn’t happen overnight, and paying it off will also require time.

Ultimately, it boils down to hard work, but rest assured, you will conquer the debt that’s been weighing you down!

80% of people save money by using Rocket Money to find and cancel unwanted subscriptions! With Rocket Money, you can also effortlessly track your spending, easily lower bills and track your net worth.