It’s difficult but not impossible to pay off student loans before graduation. And there are three good reasons for you to do so. Being in debt sucks so let me tell you how you can pay off student loans before you get your diploma.

Any of you who regularly read the blog or listen to the podcast will know that Listen Money Matters is firmly anti-debt. While having a mortgage can be smart in some cases (though you shouldn’t have most of your wealth invested in your home), consumer debt and student loan debt are a big no-nos.

That puts me in a problematic position. As a sophomore in college, I’ve already taken on nearly $11,000 in student loans, and I estimate that by the time I graduate I’ll have a total of at least twice that (not including interest).

“What’s the big deal?” you might ask. “That’s not that much debt. And going to college is a good investment anyway. Why worry?”

And in some ways, you’re right. It’s not that much debt. It’s below the national average, and it’s way less than what some people have.

As far as college being a good investment, in general, the data still supports that claim. In theory, I stand to make more over the course of my lifetime than someone without a degree.

Although that could have just as much to do with the life circumstances that allowed me to go to college as the actual value of the degree itself. And less expensive alternatives do exist.

Ultimately, though, the relative amount of my debt and the predicted value of my degree are not the point. The point is that I’m in debt. The point is that I’d rather not be.

That’s why I’ve set the ambitious goal of paying off all my student loans before graduating. I even put the goal on my Impossible List to hold me accountable.

Crazy? Definitely.

Needlessly ambitious? Possibly.

But hear me out …

My Motivations

Three main things motivate me to pay off my student debt before graduating -the peace of mind I’ll get from being debt-free, the brutal reality of compound interest and the freedom graduating with no debt will give me. I’ll go into a bit more detail about each one and why it’s such a strong motivator.

Peace Of Mind

I owe many people debts that I can never repay:

- My parents, for encouraging me to think for myself and being my first teachers.

- My high school English teachers, for teaching me the skills that allow me to write posts like this one.

- Mentors such as my professors and LMM’s own Thomas Frank, without whose teaching and inspiration I would never have started a blog and wouldn’t be writing this today.

Yeah, I owe a lot of people a lot of things, but unlike student loans, none of these debts are monetary.

The people who have helped me get where I am today didn’t expect anything directly in return for helping me, and I know I can “repay” my debt to them in the form of emails wishing them well or just by pushing myself to excel in my work, school, and life.

The student loan relationship, on the other hand, is a bit more cut and dry. They want their money, not my good wishes. True, I am grateful that my loan provider helped me pay for school, but I’m not going to show my thanks by paying interest or holding onto my debt for any longer than necessary.

I can’t remember where I heard it, but this quote always sticks with me:

“Being In Debt Is Immoral.”

That’s not always true, but in my case it sure feels like it. I’m not saying that being in debt keeps me up at night, but it does make me a bit uneasy when I remember how much money I owe, how my net worth is currently deep in the red and will be until I pay those loans off.

I’ll have enough things to worry about when I graduate. I’d rather pay off loans not be one of them.

Compound Interest Sucks

If you’ve listened to any of the LMM episodes on investing, you know that compound interest can be a powerful tool for building large amounts of wealth over time.

Unfortunately, compound interest can also work against you when it’s accruing on your debt.

In the same way, your wealth can grow exponentially over time, so can your debt.

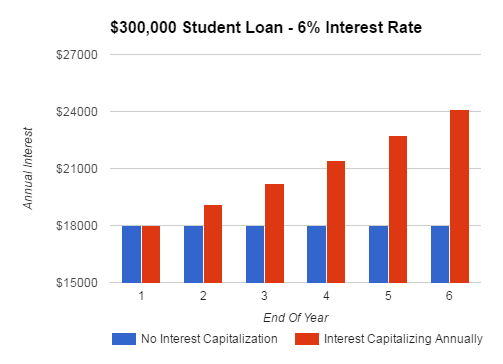

Using the calculator available from my loan servicer, I learned that for one of my unsubsidized loans the interest accrues at about a dollar a day. If you have any unsubsidized loans, the same is likely true of yours.

That’s fucking depressing if you ask me, and it’s a process I want to mitigate as much as possible.

At the very least, you should try to pay down the interest on your loans while you’re in school since often the interest that accrues on your loans while you’re in school is capitalized once you graduate. This means that the interest is added to your loan principal, at which point interest is accruing on interest.

The result is that you end up paying interest on a higher amount than you originally borrowed, and that sucks.

If you’re still in school and have student loans, check to see if interest accrues on them while you’re enrolled and whether or not the interest is capitalized once you graduate. If nothing else, you should be aware of how much money you’ll have to pay.

Sweet, Sweet Freedom

More than anything, though, the reason I want to graduate college with no debt is the freedom it will give me. I don’t want to feel pressured to take a shitty job because I need the money to pay off my debt. It may sound entitled, but wouldn’t you avoid taking an awful job if you could? Right now, while I’m in school, is just such a chance.

And even beyond the job, graduating with no debt will give me the freedom to do my own thing and not necessarily worry about making a lot of money. I’m not saying that I don’t want to do well, but I’d rather not have any external pressures.

Crazy things such as traveling the world or starting an online business (or whatever your dreams may be) are a lot easier when you don’t have several thousand dollars in debt hanging over your head.

It’s Complicated

Of course, I also realize that my relationship with debt is complicated. I really identified with what personal finance blogger/cartoonist Stephanie Halligan had to say in her LMM interview.

She points out that while she doesn’t encourage students to take on debt, the journey of how to pay off student loans ultimately led her to start the business that now supports her. Had she never had any loans to pay off, she probably would have just gotten some standard sort of job and never discovered the online business space.

I feel the same way. While I don’t (yet) make enough money online to support myself, the journey to pay off my debt was what got me into online writing and business. If I hadn’t been interested in paying off my debt before graduating, I wouldn’t be writing this article.

And I can’t stress enough the value of the education itself.

While I’ve learned and refined most of my “practical” skills outside the classroom, my undergraduate education has exposed me to perspectives, people, and ideas that I would never have encountered if I had tried to learn the same information online.

Heck, if I hadn’t gone to college where I did, I would probably never have learned about College Info Geek or Listen Money Matters.

Strange how things seem to fall into place in retrospect.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

The Challenge Still Stands

All that aside, though, I still have $11,000ish dollars in debt to pay off before I graduate. Assuming that I’ll graduate on my planned date of May 16, 2017, that leaves me (as I write this) 753 days to pay off my debt.

Graduation’s not getting any farther away, so I need to get on it. The money I earn from writing for College Info Geek is a start, but I need to step things up if I plan to accomplish my goal. I have a few ideas for how I plan to meet this lofty goal. Some of them will work for any college student out there with the same goals as me, while others might not work for everyone.

How You Can Do It

Regardless of where you are in your educational journey, if you want to become free of debt by the time you walk across that graduation stage, try out some of my tips below.

Live Like a College Student

The first step to paying off your student loan debt early is to be as frugal as possible. College student budgets are already tight but so many students tend to spend money unnecessarily.

Think about how much money you drop on a coffee from Starbucks or the local cafe every morning, or how much going out with friends every weekend adds up. Do you really need to buy that deluxe X-large pizza, or can you cook yourself?

You’ve always wanted to try that frozen pizza and kraft dinner combination!

While being “cheap” isn’t always fun, us students trying to figure out how to pay off student loans need to be thinking long-term. When we don’t owe $30,000+ after graduation, we’ll be able to spend our salaries on whatever we want!

Stay committed to living frugally and put that coffee or pizza money toward paying off your loans. You’d be amazed by the difference it makes.

Set Up A Budget

To that end, set up a budget and stick to it to better manage your money. You can use a free app like Mint.com to set up a detailed budget for food, travel, bills and more, then get notified when you’re reaching that budget so you don’t over-spend. This helps you save more money that can be applied to your student loans.

Pay Off Interest First

As I mentioned before, compound interest really sucks, so it’s best to avoid it as much as possible by paying it off early. Log on to your student loan provider’s website and identify which loans are accruing interest while you’re in school and how high the interest rates are. Pick the loan that is adding up the fastest, and focus on paying that one off first.

Once the interest-accruing debts are paid in full, you can move on to the loans that don’t accrue interest until after you graduate. This way, even if you aren’t able to graduate completely debt-free, you’ll have saved yourself as much money as possible by mitigating all that extra debt from interest. There are no penalties for paying loans off early, so there’s no excuse!

Set Up Auto Pay

Almost all loan services allow you to set up auto pay, which automatically takes a specified amount of money from your bank account each month to pay off your loan. You can set up auto pay even before you graduate to make even minor payments of $10 or $20 a month toward your loans.

If you have a reliable income, auto-pay is a great way to make out-of-sight, out-of-mind loan payments. If you find yourself with extra cash at the end of the month, you can still make additional payments to push you even closer to your goal.

Work On Or Off-Campus

Obviously, you cannot pay off student loans without some sort of income, but many students will agree that balancing work while going to school full-time is a challenge. However, most on-campus jobs usually are flexible enough to work with your class schedule, and you might even luck out and find one that lets you do homework while you’re there!

If you can’t work on-campus, look for paid internships or co-op programs that let you work part-time off-campus in a field related to your degree. Check out your school’s career center—they often have internship opportunities that not only pay, but can help you earn college credit and gain valuable work experience for after graduation! It’s a win-win-win!

Make a promise to yourself that most of the money from these jobs will go toward your student loans after you pay for housing and food (this is where auto pay really comes in handy!).

Get A Side Gig

Everyone has a hobby they enjoy and are good at—mine happens to be writing, which helps me earn some side cash by writing blog posts. Yours might be building websites, playing the guitar or taking awesome photographs.

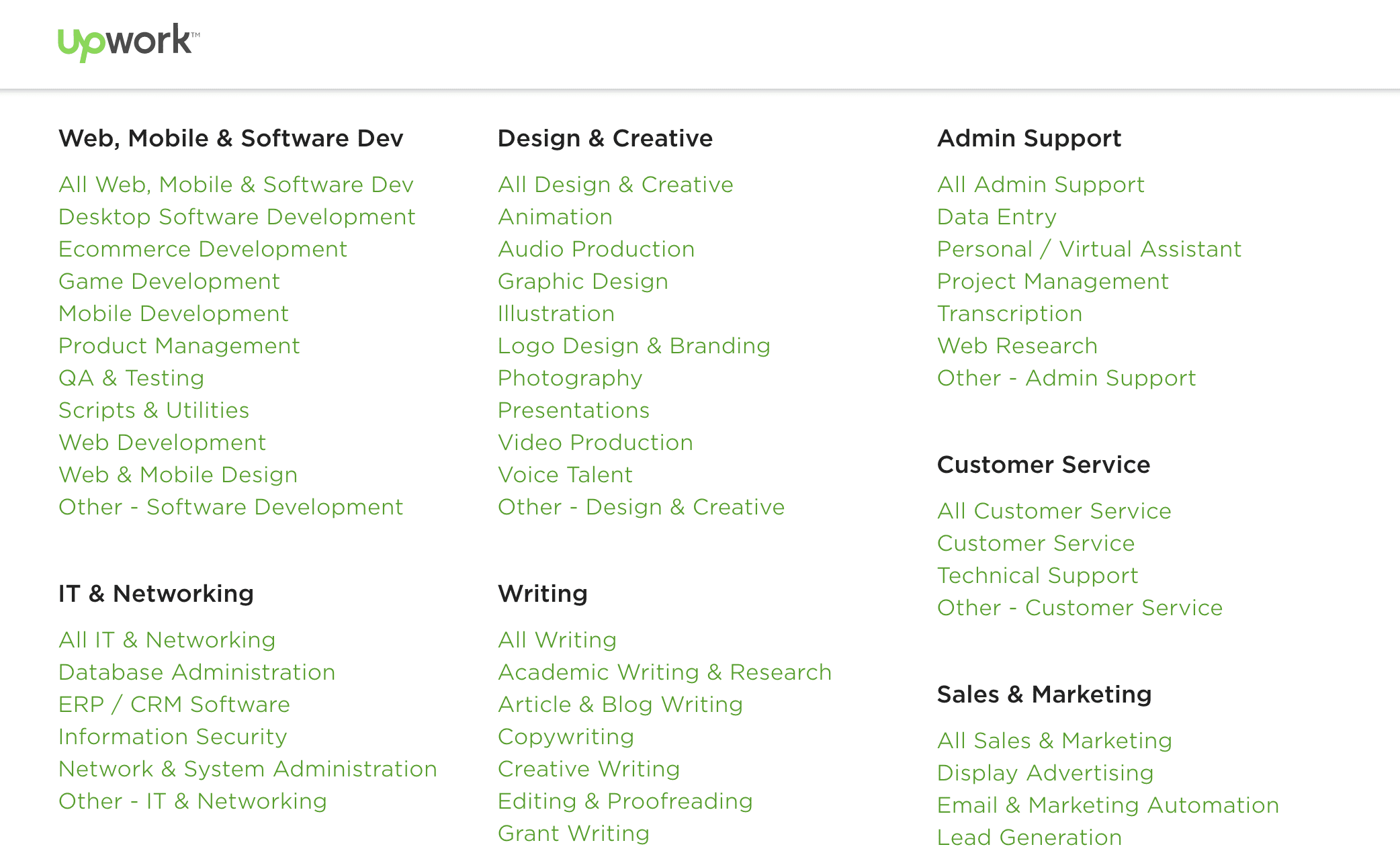

Turn those hobbies into money-making side gigs! Use websites like Upwork to find freelance design, IT, and writing jobs; teach local kids or other college students how to play a musical instrument; or offer to take professional headshots for a fee.

There are hundreds of freelancing categories to choose from.

Aside from earning you extra cash, because these are things you already enjoy doing, it will feel less like work!

If you run a blog, look into using affiliate links that let you earn money for promoting a brand or certain products. Thomas Frank from College Info Geek turned the blog he ran as a hobby into a massive money-making tool that helped him pay off all of his student loans. If you have a hobby you’re passionate about, this could be you!

Apply For Scholarships

While this tip won’t help you pay off your existing loans, it will help you avoid taking on more loans. Most colleges have vast scholarship programs that current students can apply for as soon as they’re enrolled. Look for scholarships specific to your field of study for the best chance at earning one, but also don’t be afraid to apply for as many as possible.

These scholarships can save you thousands of dollars in college tuition, meaning your student loan balance will stay low and you’re able to more easily pay off what debt you do have! While this tip works best the earlier you start, even college juniors and seniors can knock off a few hundred to a thousand dollars with this method.

Once your student loan balance hits that glorious “zero,” keep following these tips and save the money for after graduation. You’ll find that you’ll be able to continue living debt-free due to your four short years of hard work and determination. A debt-free life will feel like this…

Now if you’ll excuse me, I’m off to work on my business and dance moves.