Are you guilty of one of the seven debtly sins? Or maybe you’re an all or nothing kind of person and you’re guilty of all seven. What up party people?

The problem is, sinning is only fun while you’re sinning. The hangover is pretty bad. If the sins are debtly rather than deadly, the hangover is financial, not physical and can last for years. If you’re only making the minimum payments on your debts, it can seem like those numbers never get smaller no matter how long you’ve been paying them down, especially if it’s high-interest debt like credit card companies charge.

When you’re struggling with debt payments, you don’t have extra cash to start building an emergency fund, to start investing, or to start working towards any of your other financial goals. Having a lot of debt can negatively affect your credit score and when you try to borrow money for a house or a car, you’ll be offered the highest interest rate on the loan or you may not qualify for a loan at all.

See? Years and years. But it doesn’t have to be this way. You can be absolved of your sins. Find out how sinful you are and how to get out of debt and overcome consumerism once and for all. Can we get an amen?

The Seven Debtly Sins

None of us are perfect so we’re probably guilty or have been guilty in the past, of at least one of these.

Lust

Let’s start with lust, possibly the most fun of the sins! Lust is when you long for something to perhaps an unnatural degree. A new car when you have a perfectly good one for example. Lust is a good metaphor for American consumerism. We live in a consumer culture and we all suffer from FOMO. We want the things we see other people showing off on social media.

We want all those shiny consumer goods the advertising industry has convinced us we need.

Gluttony

Gluttony is over-consumption to the point of waste. Conspicuous consumption is an ingrained part of American society. Look at how damn fat we are.

The prevalence of obesity was 39.8% and affected about 93.3 million US adults.

And it isn’t just food we overconsume. A lot of the crap we buy in order to prop up the way of life we’ve become accustomed to in the United States and much of the Western world is contributing to climate change.

Greed

Greed is wanting more, more more. You have ten million and you want eleven. It’s natural for human beings to want more but when you have enough and your pursuit of more harms others, that’s greed. Also, you’re a dick.

When you have more than you need, build a longer table, not a higher fence.

Tweet ThisTake a look at Black Friday to see American consumer society and the greed it engenders. People have died for Chinese-made crap in Walmart. Disgusting.

Sloth

Sloth is being lazy. We spend 35.5 hours a week slothed out in front of the TV but even if we’re in so much debt we can hardly breathe, we can’t be arsed to get a second job. We have a gym membership that we spend money on every month but we haven’t walked further than from the couch to the fridge in months.

Wrath

Wrath is anger. A lot of our overconsumption of goods can be blamed on emotion, anger being only one of them. We fight with our spouse so we shop to make ourselves feel better. Maybe we had a bad day at work. We shop to make ourselves feel better.

When we make decisions based on emotions, they’re almost never good decisions.

Envy

Envy can make you buy a flat-screen because your friend has one. Keeping up with the Joneses is a big problem for some people. You don’t know how deep in hock someone might be for all the accouterments of their flashy lifestyle.

Pride

Pride can make you think you’re a special snowflake who deserves only the best. But a Honda Civic gets you from Point A to Point B just as well as a BMW.

So which are you, a personal fiance saint or sinner? If you’re a sinner, let’s see what we can do to wash away your sins. We’ll show you how to get out of debt and exorcise your consumerism.

How To Get Out of Debt

Depending on how much debt and what kind of debt you have, you may not need to follow all of these steps but whatever debt you have, we have a solution.

What Gets Measured, Gets Managed

This might be the hardest step. When we have what seems like an insurmountable problem, burying our head in the sand is appealing. But you can’t devise a plan to solve a problem if you don’t know exactly how bad the problem is.

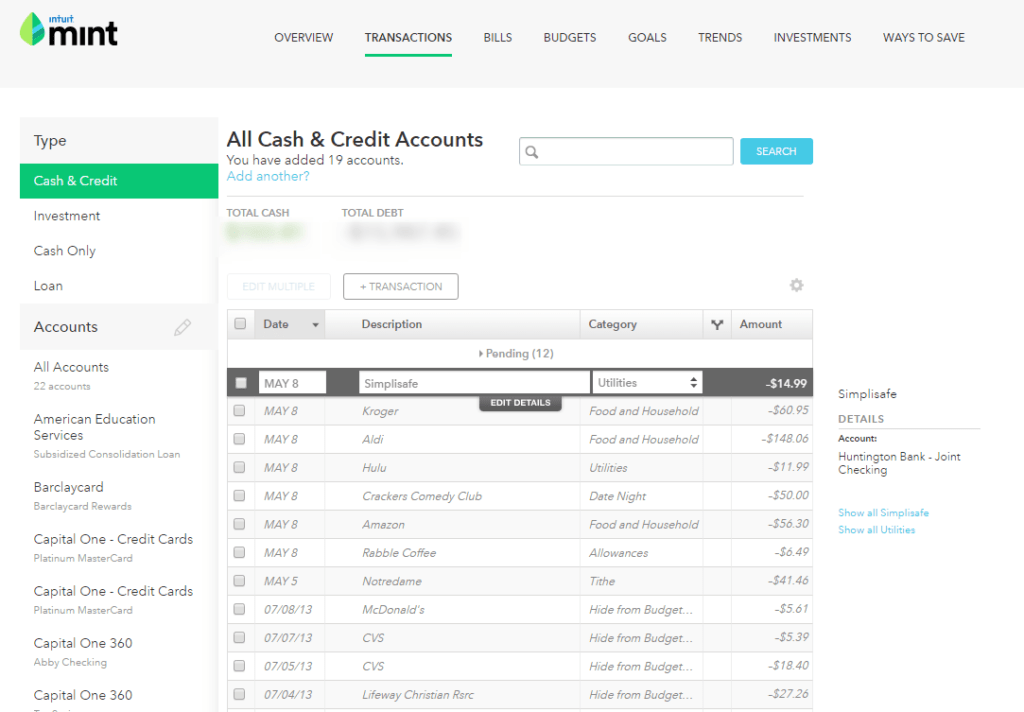

So take a deep breath, open a bottle of wine, and gather all of your debt-related financial statements. Let technology make things easier. If you don’t use Mint, you should start. We’re going to need it eventually as part of our debt management system so you might as well create an account now.

You can enter all of your account information into Mint and your transactions and totals of how much money you owe on each account. The damage may be worse than you thought or not quite as dire as you thought. Either way, you must know the number in order to move forward.

Mint will show how much money you owe but it won’t show the interest rates on those debts. This is vital information to know when making a plan to pay off debt so collect this information while you have all of the statements in front of you. You might want to create a spreadsheet listing where the money is owed, how much money is owed on each debt, the interest rates, and the due dates.

Triage

Not all debt is created equal and not all debt is necessarily “bad” debt. Once you have all of your debts listed, we’re going to triage them. Decide which debts are the worst and should be paid off first. Generally, the high-interest debt, like payday loans and credit card debt will top the list. An example list might look like this:

- Payday loan

- Credit cards

- Student loans

- Car loan

- Mortgage

Of course, there is no interest rate on an overdue utility bill but there is probably a late payment fee, your utility might be shut off, you’ll have to pay a fee to get it turned back on, and maybe make a deposit too. If you have a situation like that or your car is about to be repossessed leaving you without a way to get to work, those bills go to the top of the list.

Create a Budget

Personal finance 101 is to have a budget. While budgets aren’t just for “poor” people, if you’re in debt, having a budget is essential. We can almost guarantee that you are spending money you’re not really aware of. A budget shows you where all of your money is going.

We said you’d need a Mint account and this is why. Mint is easy to use and free. YNAB is great but it has a learning curve and it isn’t free. You don’t have the time or money for that right now so Mint it is. If you didn’t create an account already, do it now.

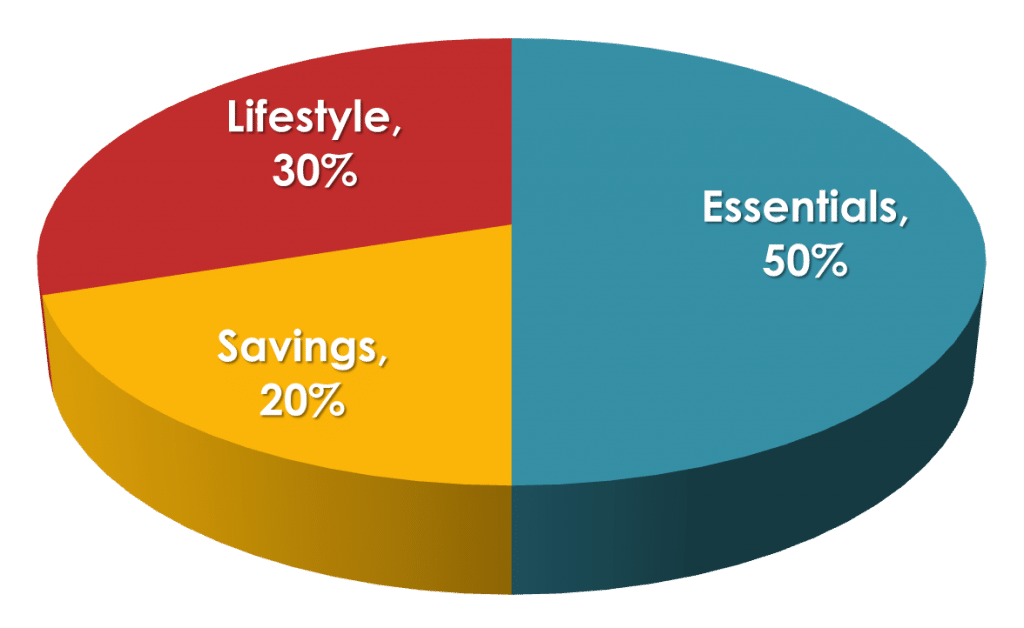

Now to budget your money. Don’t worry about making any cuts just yet, we’ll get to that. An easy way to allocate your money is the 50/30/20 rule. 50% of your net income goes to essentials, 30% goes to discretionary spending, and 20% goes to saving, investing, or debt repayment.

Things will be a little different if you have a lot of debt to pay off. And you do because you’re reading this. But for now, allocate your money this way.

Making Cuts

Okay, this part is going to suck but it will be worth it. I think it’s easier to make money than to save money but you have to do both to pay off debt. And making cuts is something you can do immediately.

Go through your budget and see what can be cut. Not what you don’t mind cutting, what you can cut. I promise there are even things in the 50% essentials category that you can live without. Rocket Money will automatically cancel things like your gym membership, meal box, and music subscription services.

Most of your discretionary spending should be cut or at least vastly scaled back if you have high-interest debt. Most investing and saving should be suspended until the bad debt is gone. You’re not going to get a higher return in the market than you’re paying on your high-interest credit cards. There are two exceptions to this.

Ideally, an emergency fund contains 3 to 9 months of bare-bones expenses but $1,000 is a great start and can really make a huge difference to your debt management plan. Do what you can to get that $1,000 and keep it in your bank account, preferably your savings account.

The other exception is a 401k if your employer offers to match your contribution. That is free money. Contribute just the amount you need to get the full matching offer.

Make a Plan

When you focus your attention on one debt at a time, you’ll be able to get out of debt faster. There are two good methods for debt repayment; debt snowball and debt stacking.

If you choose debt snowball, you list all of your debts according to dollar amount, smallest to biggest. You throw every extra dollar you can at the first debt on the list while making only the minimum payments on the others. Once the first debt is paid off, you take the monthly payment you were paying on it plus every extra dollar and start paying off the next while paying only the minimum payments on the others. So on down the list until all of the debts are paid.

The stacking method works the same except you list the debts in order of interest rate, highest to lowest and pay them off in that order.

Which method is better? The one that works for you. Stacking saves you the most money because you’ll pay less interest over time. But the snowball method can be more satisfying if some of your debts are relatively small because you can pay them off pretty quickly. That can help give you the momentum to keep paying off more and more.

Note, this method is for high-interest debt. You don’t want to throw every extra dollar you have at low-interest debt like your mortgage instead of investing because you can make more investing than you’re paying in interest on the mortgage.

Personal Loan

A personal loan is a great option when you’re up to your eyeballs in debt. If your credit score is good enough, you can get a loan through a company like Upgrade or Credible and use it to pay off some or all of your high-interest debt. If you belong to a credit union, that may be another good place to apply for a personal loan. Like online lenders, credit unions often offer lower interest rate loans than do traditional banks.

Yes, you still have debt but the debt has a lower interest rate than your credit card debt.

Balance Transfer Credit Card

Again, if your credit report is in good shape, you may be eligible for a balance transfer credit card. Even better than a low-interest personal loan, these cards have an introductory period with 0% interest.

You transfer the balance from a high-interest credit card to the new card. For a period of time, usually 6 to 18 months, every dollar you pay is going toward the balance. Make extra payments when you can before the introductory period runs out and the regular rate goes into effect which could be higher than the rate on the old card.

Make More Money

At some point, if you’ve done what we suggested earlier, you’ve made all of the cuts you can make. You still have to pay your rent or mortgage, still have to make your car payment, still have to eat, still have to pay for health care. So for our debt payoff plan, you need to make more money.

In the past, a second job is something mostly those in the working class had to consider. But thanks to the economic system and consumerist society we live in, it’s something more and more people in the middle class have had to do.

And it’s easier than ever to manage a second job thanks to the internet. There are tons of side hustles that allow you to make money from home and on your own schedule. Get one or two or three.

Ask for a raise, but go in fully prepared. People rarely get raises just for asking. You have to show why you deserve a raise. If you don’t get a raise, start looking for a better paying job. A new job almost always gives you a bigger pay increase than just getting a raise at your current job anyway.

Sell some of your stuff. Your house is full of stuff you don’t use that someone else will be happy to pay for. Don’t just throw it away when you go all Marie Kondo on your place. Landfills are full of consumer products that are perfectly salable. Make some money and do your part against climate change.

Use Found Money

Found money can come from lots of places. Money you got for a birthday or Christmas, your bonus, the money you won in the office betting pool, your tax refund. All of that money goes to paying off your debt, not to doing your part to spur economic growth.

Stop Spending!

OMG. Do we have to say this? When you start to see those credit card balances go down you might be tempted to run them back up. No! No, no, no! We’ll get to dealing with your overspending once you’re out of the red zone but in the meantime, do what you have to do to remove the temptation those credit cards represent.

Cut them up, give them to a trusted friend for safekeeping, remove the numbers from all of your online shopping accounts. Don’t cancel the cards though. Doing so hurts your credit score which is already probably in the toilet. And credit cards used well are not evil. They can provide things like cash back, consumer protection, and travel benefits.

If you’re struggling to stay within your budget, you can employ the envelope system. It’s not the most convenient method of budgeting but it is effective.

How You Doing?

We understand that knowing how to get out of debt and actually doing it are two different things and we know getting out of debt is hard. But you’re doing great. Just keep at it. Let’s see how we can prevent this from happening again.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

Staying Out of Debt

Once you are finally out of debt, or at least out of the danger zone, you can start to look at why you went into debt and how you can stay out of debt going forward.

What Caused the Debt?

If this is your first time dealing with debt, you get something of a pass. Maybe you went into debt due to a job loss. That’s understandable. You had bills to pay and no money coming in so you paid your expenses on a credit card.

Medical debt is also understandable. Health care is criminally expensive in America and even those with insurance can find themselves struggling.

Most people who experience difficulty paying medical bills have health insurance,” the Kaiser Family Foundation (KFF) reports. And a report from the Consumer Financial Protection Bureau showed that 43 million Americans have overdue medical bills on their credit reports, with half of all overdue debt on credit reports coming from medical bills.

But maybe you peg your well-being to consumerism, buying lots of stuff you don’t need and going into debt to do it. Understand where your debt came from. Whatever the reason, there are steps you can take to make sure you stay out of debt once and for all.

Have an Emergency Fund

Debt from a job loss or medical issue can be avoided or at least lessened when you have a fully-funded emergency fund. Fully funded means 3 to 9 months worth of expenses. The $1,000 we talked about earlier is a good start but once you’re out of debt, growing your emergency fund should be your priority.

If your job is relatively secure and your expenses relatively low, 3 months is probably good enough and you can leave that money to chill in your savings account. If your job is less secure or your expenses high, 9 months is a better goal.

That’s a lot of money to leave in a savings account making bunk interest though so consider one of the short-term accounts where your money will grow a bit more.

Change Coping Strategies

If you spend money in response to stress or unhappiness, you need to find a better way to soothe yourself. Remember the good feeling that came from spending all that money? Now think back to how you felt when you totaled up your debt. It was infinitely worse.

Make a list of things that make you feel better that don’t involve spending money. Seeing a friend, going for a run, taking a bath, cooking something, spending time on a hobby. When you feel stressed or unhappy, do one of those things rather than logging onto Amazon or heading to the mall.

Buy Real Happiness

Life is tough and sometimes we take happiness where we can find it. And you can buy happiness but if you’re buying stuff, you’re doing it wrong. Rather than buying stuff, buy an experience. Doing so has been proven to make us happier.

I don’t live in NYC anymore but when I did, nothing made me happier than going to the Met by myself and spending a few hours wandering around looking at art. Some of the things in that museum were thousands of years old and for some reason, I found that comforting. Those things had survived disasters untold and yet here they were, resilient, ever-lasting, bringing beauty to generations of people. Gives me chills writing that. I had a membership so a trip to the Met cost me exactly $0.

Central Park had a similar effect. So find a free or inexpensive experience that will make you feel happy and peaceful. If you can’t think of any, you’re not trying hard enough. Take your dog for a walk, buy yourself a luxurious but affordable treat like one of those ridiculously expensive French macarons. Go to a free concert in your city’s park, bring a friend and a picnic. You’ll remember and get more pleasure from any of these things than you will from another pair of shoes.

Watch Your Money Grow

You know what’s better than seeing the amount of debt you have go down? Seeing the amount of money you have invested going up. It’s like a million times better. The second you pay off the last dollar of your high-interest debt, open a

Compounding interest was working against you when that debt was piling up but when you’re investing, compounding interest is working for you.

We Don’t Want to See You Here Again

You did it and we’re so proud of you! Getting out of debt is not easy. Remember how much it sucked. Remember every vacation you couldn’t take, every happy hour you missed out on, every minute you lay awake at night unable to sleep because your debt was weighing on you like a lead blanket.

Make a solemn promise to yourself never to be in that place again. Because debt sucks and we don’t want to see you here again.

Show Notes

Keegan Ales Mother’s Milk: A dark, creamy, milk stout.

Buffalo Sweat Sweat Oatmeal Stout: A sweet, smooth stout.