There are a lot of personal finance terms thrown around that many of us don’t understand so when we hear them, we just nod and smile. But LMM is all about education, so we’re going to devote this episode to understanding economic bubbles.

Our episode on cryptocurrencies got us thinking about economic bubbles. It’s an interesting subject and Bitcoin might be the next one, so we wanted to delve further into bubbles.

What is an Economic Bubble?

A bubble is a fast rise in an asset’s price followed by a contraction. Bubbles happen when the price is not justified by the asset itself but rather by the over-exuberant behavior of investors. When there are no more investors willing to pay the overinflated price, people panic and sell and the bubble bursts.

Peter Kugis of Stanford University defines bubbles more simply,

“A bubble is where investors buy an asset, not for its fundamental value, but because they plan to resell, at a higher price, to the next investor.”

Economic bubbles rely on the greater fool theory. The people who enter the bubble early may not necessarily believe what they’re buying is useful but what they do think is someone in the future will pay them more for it than what they paid themselves. Somewhere out there is a bigger fool, but at some point, there is the last fool.

Kind of sounds like a Ponzi scheme doesn’t it? There are some similarities, but a Ponzi scheme is a deliberate fraud. The money people think they’re investing is never actually invested. Instead, it’s used to pay “returns” to earlier “investors.” The scheme has to grow fast to keep paying the early investors.

When the growth finally slows down, those investors are no longer getting the expected returns, and the whole thing collapses. Bernie Madoff was the most recent and probably most spectacular example of this.

Fraud can be part of a bubble, but fraud isn’t necessary for a bubble and bubbles do involve real investments.

Historic Economic Bubbles

Bubbles are nothing new. The first bubble may have happened nearly 400 years ago.

The Housing Bubble

The most recent bubble was the 2008 housing crisis. Banks were handing out mortgages like Halloween candy. Investors got so greedy they ignored how much risk they were taking. Mortgage companies like Country Wide were churning mortgages. They only held the mortgages for a short time before selling them off which means they were assuming none of the risks. That’s why they were giving million dollar mortgages to waitresses.

When people who could never afford those mortgages started to default the companies who were overexposed in the sub-prime mortgage market like Lehman Brothers collapsed. Lehman going down wasn’t the first domino to fall but it caused a massive chain reaction.

The whole thing is too complicated to cover as part of another show but if you want to understand it better, watch or read The Big Short. TL: DR, greed caused this.

Dot-Com Bubble

In the 1990’s there was a ton of money from venture capitalists looking to fund the next Facebook or Amazon. Investors in their greed lost their sense of caution and threw cash at startups.

At the peak of the market, some big tech companies placed big sell orders on their stocks which made investors panic and start selling off. Many of the startups began to fail, and the Fed hiked interest rates several times. At the end of 2001, most publicly traded dot-coms went under and all of that venture capital investment money disappeared into the ether. Greed caused this one too.

Stock Market Crash of 1929

This bubble is the big one; it’s what helped cause the Great Depression. The market was rising, and people thought it would continue to do so despite signs that the economy was starting to slow. The Fed warned of excessive speculation which caused investors to start selling. The warning prompted a mini-crash, and some financial institutions stepped in to shore up the market. It worked, and people got cocky again.

The London Stock Exchange crashed causing another panic that several banks stepped in to quell. It worked temporarily, but it was too late. The crumbling foundation of the market was exposed, and it all came tumbling down. Over a four day period starting on October 24th, the Dow Jones lost $30 billion in market value. In today’s money (using the CPI adjustment) that is $396 billion. The cause of all this? You guessed it, greed.

Tulip Mania

Tulip mania may or may not be an urban legend sort of thing. If it did indeed happen, it was the world’s first financial bubble. Way back in 1637, tulips suddenly and inexplicably became trendy. Excessive speculation on the price of tulips drove the cost of a single bulb to ten times the annual income of a skilled craftsman.

The price plunged in a single week which left many tulip holders bankrupt. Greed was again the cause.

Fiscal flexibility that’s funny, free and delivered weekly.

Bubble Causes

Well, greed as we saw in all the examples of financial bubbles. But there are causes beyond pure greed.

The Fools

Fools are always causing bad things to happen, and they contribute to economic bubbles too. The fools are those from the greater fools theory. When there are no greater fools, the bubble bursts. Bitcoin may be an example of the greater fool theory. The demand has skyrocketed because the price is going up so quickly.

When we did our cryptocurrency show , the price per Bitcoin was just over $6,000. Bitcoin peaked at over $64,000 in November of 2921 and as of December of 2023 it was back down to just over $43,000. Charles Kindleberger, a historian of financial bubbles perhaps explained the mad rush for Bitcoin when describing various bubbles,

There is nothing so disturbing to one's well-being and judgment as to see a friend get rich.

Tweet ThisExtrapolation

Extrapolation is projecting past data into the future on the same basis; if prices have risen at X rate in the past, prices will continue to rise at X rate forever. Extrapolation causes investors to overbid risky assets in an attempt to capture the same return rates.

The overbidding will result in reduced rates of return, and then the price deflation starts. When investors are no longer making money by holding risky assets, they will begin demanding a higher return on their investments.

The housing crisis is an example of extrapolation. People believed that “housing never goes down.” They were wrong, and the world economy paid the price.

Herding

Herding is an aspect of behavioral finance. It is the tendency humans have to do what the rest of the herd is doing even if as an individual, they know what they are doing is irrational. The dot-com boom is an example of herding.

People knew in the back of their minds that shoveling money at companies who sometimes didn’t have a business plan, or even a product, merely an idea for a product, was irrational.

But everyone else was doing it, and humans have FOMO. So many investors went against their own better judgment and made what were pretty clearly bad investments.

In his book Devil Take the Hindmost: A History of Financial Speculation, Edward Chancellor talks about how the herd mentality takes shape during history’s great financial bubbles:

“In financial markets, one might say they are prepared to ignore bad news because they still hunger after the immediate profits of speculation. A description of the speculators in William Fowler’s circle during the 1860s illustrates this behavior. They were engaged, wrote Fowler, ‘in bolstering each other up, not for money, for we thought ourselves impregnable in that respect, but my argument in favor of another rise. We knew we were wrong but tried to convince ourselves that we were right.’”

Moral Hazard

Moral hazard means that if someone is protected from risk, they behave differently than if they were fully exposed to the risk. That our behaviors have consequences helps us to make rational decisions. You would love to smack your annoying co-worker, but you don’t because the consequences of doing so are all bad.

A moral hazard occurs when the risk-return relationship is altered, usually because of some government interference. The National Flood Insurance Program is an example of moral hazard. Insurance companies will sell policies to cover flood damage to homes in flood-prone areas because there is no risk in it for them.

The government subsidizes the policies, so if a homeowner makes a claim, the government, not the insurer pays it out. These policies are nearly pure profit for the insurance company with no risk. Homeowners make a claim, and the company merely handles the paperwork.

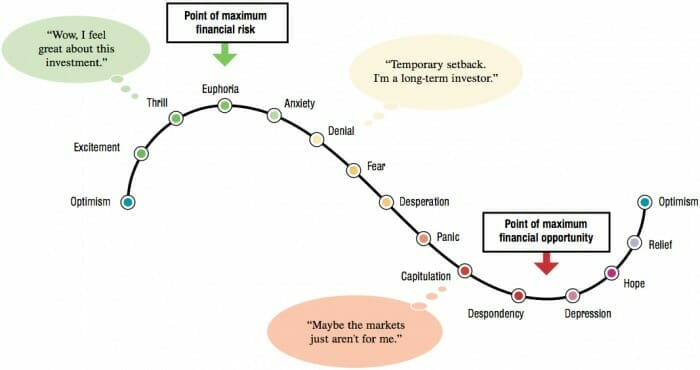

Human Psychology and Economic Bubbles

What’s really at the heart of financial bubbles is human behavior. There are four distinct psychological phases of financial bubbles.

Stealth Phase

The stealth phase is the very early days of an asset when only relatively few people are aware of it and can see the value. It’s like that one annoying friend everyone has who just listens to the most obscure, underground bands from Eastern European countries. The true believers.

Awareness Phase

Now big money comes calling. Institutional investors take an interest. There is some selloff during the awareness phase by the initial true believers but not enough for anyone to notice. The true believers are starting to think the band is changing, trying to go mainstream to sell out.

Mania Phase

The media picks up on what is going on and shouts it far and wide. Average investors catch wind that something big is happening and they want in. The price starts to go up, and inexperienced investors think it will keep going up forever. Your parents are now listening to the band.

Blowoff Phase

The blowoff phase is the bubble part. The selloff accelerates driven by fear. The fire sale plunges the price of the asset. There are now no greater fools. The band is currently doing a weekly show in Branson, Missouri.

Spot the Bubble

Is your idiotic brother in law who has filed for bankruptcy seven times and once tried to strike it rich panning for gold in the desert telling you to buy a particular stock? That’s a good sign that its part of a bubble.

In an interview, financial theorist, neurologist, and financial adviser (how’s that for a CV!) William Bernstein laid out his criteria for spotting bubbles, and it has more to do with sociological factors than economic indicators.

- Everyone around you is talking about stocks (or real estate or whatever the fad asset of the day is). And you should start worrying when the people talking about getting rich in certain areas of the market don’t have a background in finance.

- When people begin quitting their jobs to day trade or become a mortgage broker.

- When someone exhibits skepticism about the prospects for stocks and people, don’t just disagree with them, but they do so vehemently and tell them they’re an idiot for not understanding things.

- When you start to see extreme predictions. The example Bernstein gives is how the best-selling investment book in 1999 was Dow 36,000.

They’re Not Hard To Spot

With all these signs, you think people would see financial bubbles coming a mile away.

- Unusual changes in single measures, or relationships among measures (e.g., ratios) relative to their historical levels. For example, in the housing bubble of the 2000s, the housing prices were unusually high relative to income.[35] For stocks, the price to earnings ratio provides a measure of stock prices relative to corporate earnings; higher readings indicate investors are paying more for each dollar of earnings.

- Elevated usage of debt (leverage) to purchase assets, such as purchasing stocks on margin or homes with a lower down payment.

- Higher risk lending and borrowing behavior, such as originating loans to borrowers with lower credit quality scores (e.g., subprime borrowers), combined with adjustable rate mortgages and “interest only” loans.

- Rationalizing borrowing, lending and purchase decisions based on expected future price increases rather than the ability of the borrower to repay.

- Rationalizing asset prices by increasingly weaker arguments, such as “this time it’s different” or “housing prices only go up.”

- A high presence of marketing or media coverage related to the asset.

- Incentives that place the consequences of bad behavior by one economic actor upon another, such as the origination of mortgages to those with limited ability to repay because the mortgage could be sold or securitized, moving the consequences from the originator to the investor.

- International trade imbalances, resulting in excess of savings over investments, increasing the volatility of capital flow among countries. For example, the flow of savings from Asia to the U.S. was one of the drivers of the 2000s housing bubble.

- A lower interest rate environment, which encourages lending and borrowing.

Bubble Benefits

Like anything else, financial bubbles aren’t all bad. Some good does come from them. The housing bubble created a lot of new homes. Before the bubble burst, the houses were unaffordable but after, they were much cheaper. People who thought they could never afford a home were now able to buy one. Infrastructure also sprung up around all these new homes, things like parks, schools, and improved local services.

The housing bubble also created jobs and increased wages, temporarily anyway. Construction and real estate industry workers prospered during the boom that preceded the burst.

Bubbles can drive innovation. Startups who do have a good product or service get an influx of cash that allows them to bring their idea to the market. For every one hundred Pets.com, we got an Uber.

Beware the Next Bubble

What is the next big bubble? A lot of people think it’s Bitcoin and it’s not hard to see why. Less than a decade ago it was worth $0 per coin, and now it’s worth almost $16,000, and your grandmother knows what it is. In our interview with J. David Stein, he disputes this because Bitcoin has no valuation.

I think the next bubble to burst will be student loans. Once Congress changed laws surrounding discharging student loan debt, the floodgates opened. Lenders started handing out student loans to anyone with a pulse and colleges hiked tuition to obscene amounts.

But the students graduating, those who even did, weren’t able to find a job, or they were “underemployed,” doing a job they wouldn’t have needed an expensive degree to do, and that did not pay well.

There is $1.6 trillion in outstanding student loan debt in the US. Of that, 14.3% is in default. Consumer spending drives the economy. One-quarter of the population are Millenials, and they are the group most impacted by student loan debt.

If they don’t have money to spend, the economy suffers, and that affects everyone whether they have student loan debt or not.

Beware of bubbles. We know it can be hard to take the emotion out of investing, but you can’t make investment decisions with your feelings. Mind the bubbles.

Show Notes

Super Going: A dry-hopped ale with orange zest.

Woodchuck Cider: An amber cider.

Tool Box: All the best stuff to manage your money.

Investable: Research and evaluate rental properties.

Why do stock and housing markets sometimes experience amazing booms followed by massive busts and why is this happening more and more frequently?