Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

If you read any personal finance blogs or listen to any personal finance podcasts, you’ve probably heard of the FIRE movement. LMM has written and talked about it in the past, but some in the personal finance world devote their blog or podcast to the FIRE movement entirely.

The concept of FIRE (Financial Independence, Retire Early) is not a new one. It has simply been repackaged cleverly by a few insightful individuals. Notably, pioneers such as Mr. Money Mustache and the Mad Fientist have achieved significant success and recognition as leading advocates of the FIRE movement. They are among the most famous and successful figures in this area. Additionally, Reddit hosts several subreddits devoted to the FIRE philosophy, reflecting its growing popularity and community engagement.

The FIRE concept’s popularity is no mystery, as the idea of retiring early with financial security is widely appealing. However, the journey to financial independence demands a mindset quite different from that of early retirement, creating an interesting contrast within the FIRE movement. Nonetheless, the catchy acronym has helped propel its widespread appeal.

But there are indeed downsides to setting yourself on FIRE, particularly for young people. Living a life of extreme frugality can mean missing out on a lot of the pleasurable aspects of your life. And early retirement can be downright dangerous to your health.

Most of the people who make a living selling FIRE don’t talk about those downsides because it’s damaging to the brand. So is FIRE a matter of your money or your life?

We set about finding the truth about the FIRE movement.

Breaking Down FIRE

Part of the slick packaging of the movement is the cool acronym. FIRE stands for Financial Independence, Retire Early.

Give Me an F, Give Me an I

The F and the I in FIRE stand for Financial Independence. I guess some people have grandiose notions of that like being able to buy a helicopter because you’re bored or having a garage full of Lambos. But that kind of stuff takes a lot of money, way more than most of us are going to see in our lifetimes.

So let’s be a little more realistic and define Financial Independence as having enough money to make big life decisions based on what you want to do instead of what you must do.

You want to quit your job to go back to school or start a business. Do you have the money to do that? Maybe you like your job well enough but would prefer to cut back from full-time to part-time. Do you have the money to do that?

Maybe living in the city has become too much, and you want to buy a big piece of real estate in the middle of nowhere and build a house. Do you have the money to do that?

Notice what I left out? Dreaming of quitting your job to just watch TV and play video games all day? Even if you’ve got the cash, it’s not gonna fly. We’ll get into why that is.

Give Me an R, Give Me an E

The “R” and “E” in FIRE represent “Retire Early,” which is where potential issues with the FIRE movement emerge. Many interpret early retirement as the end of work forever, an appealing prospect at 70, but what about at 35? While retiring early might sound ideal, consider the implications of being retired for several decades.

The R and the E in FIRE stand for Early Retirement. This is where the problems with the FIRE movement can arise. Lots of people define early retirement as never having to work again. Which can sound great if you’re 70 but what if you’re 35? You want to retire early but do you want to be retired for several decades?

First of all, you’re going to get bored. Have you ever had a period of unemployment? It’s great for the first few days and maybe even the first few weeks, but once the novelty wears off, you have days and weeks to fill. And in the case of early retirement, you have years and decades to fill.

For all the bitching a lot of us do about work, not always unjustified, work serves a lot of purposes. It gives us routine, purpose, friends, or at least the ability to socialize. And then there is the small matter of keeping us alive.

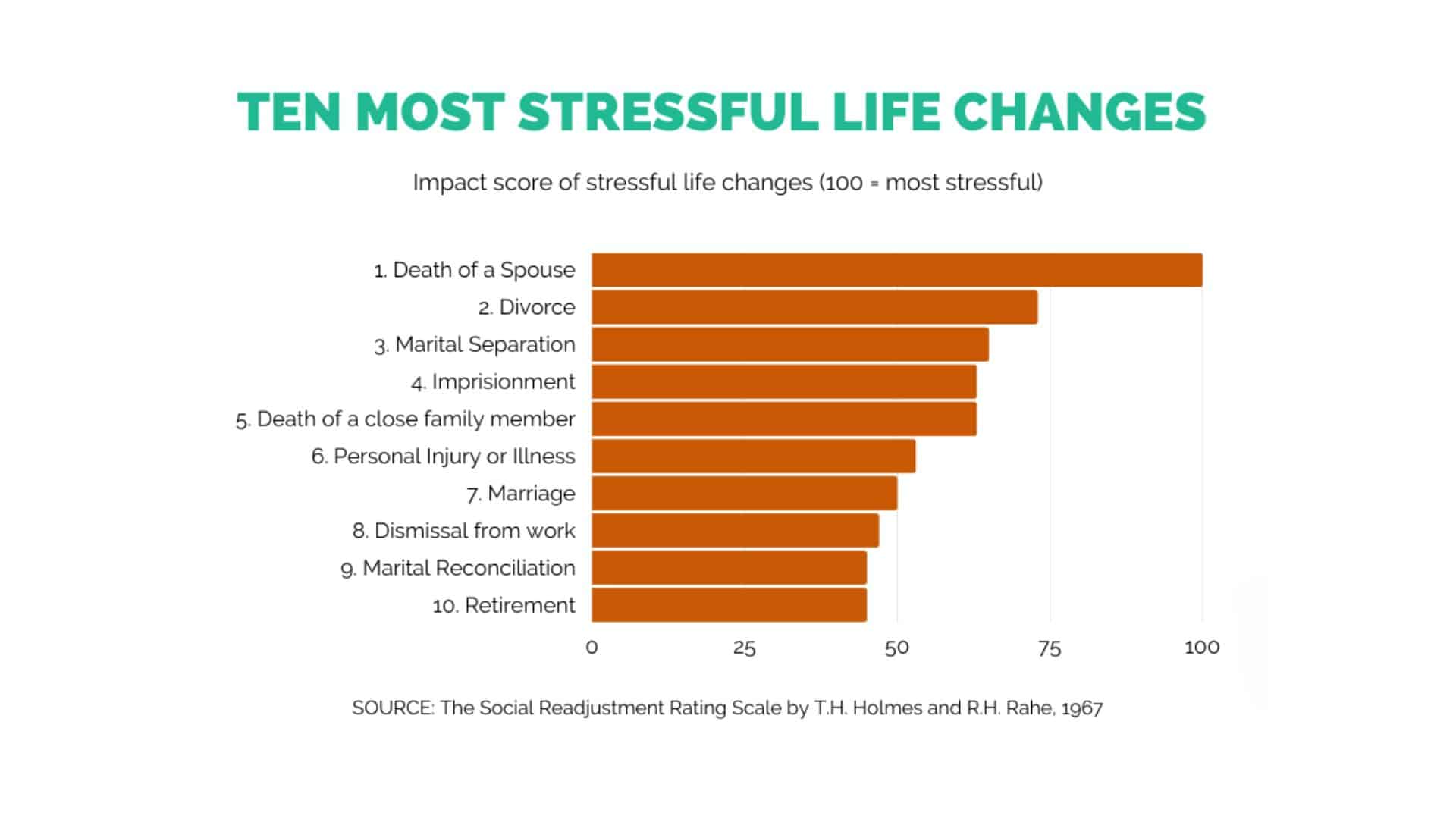

The study found a strong correlation between people who begin claiming their Social Security three years early (at 62) and death – particularly men, whose mortality risk jumped about 20%. Retirement is ranked 10th on the list of life’s 43 most stressful events for a reason. If your social life was entwined with your work, then leaving that day job with your regular friends can be depressing and challenging.

We also have to consider what could happen to those very young early retirees when a bear market comes calling. We’ll cover that separately.

Kinds of Fire

There is more than one way to skin a cat (don’t skin a cat anyway), and there is more than one type of FIRE.

LeanFIRE

LeanFIRE appeals to those aiming for extremely early retirement, around the ages of 35 to 40. Achieving this requires significant sacrifices, and adopting a minimalist lifestyle.

Those who follow LeanFIRE embrace extreme frugality, with some even choosing to live out of a van. They drastically cut back on common indulgences such as dining out or taking vacations, and heavily invest in DIY activities, ranging from growing their food to making their own clothes.

LeanFIRE followers also tend to be childfree which is understandable given that it costs about $331,933 to raise a child to 18. LeanFIRE is probably not realistic for most of us. Although the idea may seem appealing to some, most people would find it challenging to maintain such a lifestyle for an extended period.

But if you want to prove me wrong head over to Early Retirement Extreme, the leader in the LeanFIRE niche.

FatFIRE

FatFIRE frankly sounds awesome! It’s having your cake and eating it too which is always the ideal situation but rarely possible.

That’s pretty much the case with FatFIRE. It definitely can be achieved but by a pretty small segment of people. It means being able to not only retire early but to live like a baller. FatFIREs want to live in expensive cities, eat at expensive restaurants, wear expensive clothes, and take expensive vacations.

To FatFIRE, you’ll need a pretty well-paying career before your early retirement and a relatively but not extremely frugal lifestyle during your working years. Once you retire early, you’ll need to have a lot of money in retirement savings and a big fat investment portfolio.

But probably most crucially, you’ll need a couple of income streams, and most or all of them will be passive income streams. And I’m not talking about earning passive income by answering surveys. You need to have things like income from dividend stocks and real estate investments.

Unsurprisingly, doctors make up a significant portion of the FatFIRE movement. Physician on FIRE spells it all out.

ListenMoneyMattersFIRE

LMMFIRE is the brand of FIRE we recommend. Financial independence means largely divorcing your time from your income. That’s what passive income does. You have a way (ideally more than one) to make money that requires little effort from you.

Initially, setting up this income stream may involve some effort, or perhaps even a considerable amount, but once the groundwork is laid, you continue to earn money regardless of whether you’re sleeping, hungover, on vacation, or even in a coma.

LMM is a form of passive income. The ads on the podcasts and the affiliate links in the articles allow them to generate revenue without any additional effort once they’re recorded and written.

Rental property is another form of passive income.

Our proven, data-driven approach to building a portfolio of income-producing rental properties that perform in the long-term.

LMMFIRE requires a side hustle though. You can’t just sit back and watch the passive income roll in no matter how much it is. Why? Because part of having a fulfilling life is having a sense of purpose and creating things.

Mr. Money Mustache, the frugal king, has a whole slew of businesses. If you follow his blog, you get the impression he’s addicted to creating things.

Why keep working when you don’t need the cash? Because you love what you do. For many, it’s all about doing something they’re passionate about, not just making money (although the money helps). It’s about feeling good, staying busy, and loving the grind, even when the paycheck isn’t the main point.

Everyone pursuing FIRE should have a passion project. Ideally, it should generate some income, but generating revenue isn’t necessary if you have sufficient funds from other income streams to sustain your FIRE lifestyle.

BaristaFIRE

I kind of like this one. BaristaFIRE means working just enough hours to get employer-sponsored health insurance. We’re all well aware of how ruinous medical expenses can be when you don’t have health insurance (and sometimes even when you do) and how expensive paying out of pocket for coverage can be, so becoming a BaristaFIRE seems like a good solution.

Plus you have the pleasant aspects of a job, a purpose, a place to go, and social interaction, but you aren’t slogging away for 40 or more hours a week.

Exploring the path to BaristaFIRE requires careful consideration. You and your spouse may decide if one of you should continue working, primarily to secure health insurance coverage for both. This strategy is a crucial aspect of the BaristaFIRE approach, where partially working can complement your financial independence plan by providing essential benefits.

TBDFIRE

A little from Column A, and a little from Column B is what TBDFIRE is about. If you’re going to FIRE, you’ll probably do it this way. TBDFIRE means you create your version of FIRE based on the things that align with your values, whatever they may be.

For example, living the LeanFIRE way to retire at 40 might not be your thing for the long haul, but it could work short term to boost savings. Then, transitioning to BaristaFIRE could be ideal, as completely stopping work too young might lead to boredom, offering a nice balance between saving and staying active.

Little of this+ little of that=TBDFIRE.

Fiscal flexibility that’s funny, free and delivered weekly.

Catching Fire

If you want to achieve FIRE, there are three key components and most people will need to practice all three.

Frugal Until Hurts

Being frugal means something different to everyone. For the LeanFIREs, it means living in a van down by the river. For those following the FatFIRE path, frugality might involve forgoing an eighth vacation in a year. For the rest of us, it means spending less money than we make.

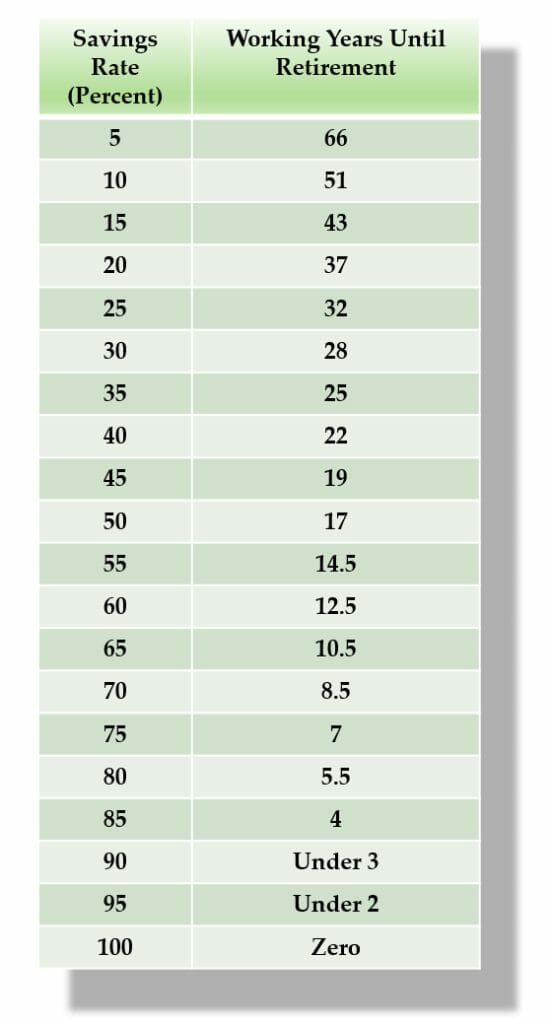

A lot less. Take a look at this chart. If you’re 30 and want to retire at the magical FIRE age of 40, you need a savings rate of 65%. Clipping coupons won’t do it. To save that much money, you have to dedicate yourself to simple living.

Utilize this retirement calculator to pinpoint when you can retire. It assesses your savings, investment plans, and retirement goals to provide a tailored retirement timeline, simplifying your financial planning process.

We’ve done a ton of stuff on ways to live frugally including saving on electric bills, groceries, and date nights. Those things help, but housing is the most significant expense for most people so keeping your housing costs low is the best way to get your FIRE started.

80% of people save money by using Rocket Money to find and cancel unwanted subscriptions! With Rocket Money, you can also effortlessly track your spending, easily lower bills and track your net worth.

Invest, Invest, Invest

To achieve FIRE, simply investing your money in an Index Fund and considering it done won’t suffice, although it’s a solid beginning. Active and strategic investment is crucial for reaching your financial independence and early retirement goals.

Yes, you need to max out your retirement accounts because they’re tax-advantaged. But just because you retire doesn’t mean you can access the money in those accounts. You can’t take money out of those accounts until you reach a certain age (currently 59 1/2) unless you’re willing to incur a penalty (you’re not).

There are some exceptions to this, but by and large, money invested in retirement accounts should be left untouched until you reach the penalty-free withdrawal age. If you can’t touch your “old age” nest egg, you need money in investment accounts that you can access to pay your annual expenses.

We did an episode on dividend aristocrats. They’re perfect for FIRE folks because they can supply a steady income stream. We’ve already mentioned rental property, but if you don’t want to own houses and all that comes with them, you can still invest in real estate through REITs and Fundrise.

How do you know when you have enough invested to FIRE? There are a lot of ways to calculate it, and lots of them are super complicated. We like to keep it simple, so we like the 4% rule. Decide how much money you want to spend on annual expenses and multiply it by 4%.

While the 4% rule can serve as a useful starting point for retirement planning, it’s important to tailor your strategy to your specific financial situation, potentially consulting with a financial advisor for personalized advice.

Say you have $500,000 saved, you could withdraw $20,000 a year and never run out of money. If you’re a LeanFIRE, that might do it. A FatFIRE, you’ll be needing much more.

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.

Always Be Stashing

To kindle your FIRE, you must always be stashing away money, and always saving. It starts with an emergency fund. It’s important for anyone, but it’s critical for FIREs. The gold standard is six months’ worth of expenses. FIREs probably want even more than that.

A rebellion against the unbridled materialism of the Baby Boomer generation (and against the willingness to enslave oneself to debt to achieve it) is long overdue.

Tweet ThisOnce you achieve FIRE, it’s critical to continue saving and investing. Without the consistent income, a traditional job provides, maintaining and growing your savings through smart investments becomes more important than ever to sustain your financial independence.

What If?

It’s no coincidence that the FIRE movement took off right around the financial meltdown of 2007-8. People saw the writing on the wall. You cannot count on having the same job for thirty years and retiring with a pension.

That scenario wasn’t true well before 2007-8, but it was thrown into stark relief during that time.

While the desire for an “escape route” from traditional work and stock market growth might play a role, the reasons people pursue FIRE are diverse. FIRE’s appeal goes beyond just potential investment returns, encompassing the desire for financial independence, control over time, and potentially a simpler lifestyle.

Since the bull market began on March 9, 2009, the S&P 500 has soared more than 498.73%.

Even if stocks do return 8-12% over time, it’s going to suck living on a LeanFIRE budget and watching your nest egg decline in value by 30-50%.

When this happens, those FIREs who haven’t made the correct calculations are going to stream back into the job market after an absence of many years. Not ideal.

Those FIREs who adopted the LMMFIRE approach, a bit of frugality, a ton of investing and saving, and a couple of solid side hustles, will come out okay.

Can Anyone Do It?

Probably not and this is where the FIRE community gets a lot of flack. It’s easy to promote the wonders of FIRE when you’re high-earning DINKs (double income, no kids) but a lot harder when you’re a single parent making $40,000 a year.

Well, not everyone can play in the NBA either, but that doesn’t mean you can’t join a pickup league.

The principles of FIRE work for everyone.

Live frugally, save, invest, and have multiple income streams.

Not everyone can achieve FIRE, but everyone can improve their financial situation using FIRE principles.

Which Fire Are You?

We’ve detailed a couple of different types of FIRE, which one should you aim for?

Let me use the weight loss analogy because losing weight and personal finance have a lot in common.

If you want to lose weight, you have to eat properly and exercise. There are a million ways to eat well and exercise. Which ones do you choose?

You choose the methods you can sustain. That means you have to find a diet and mode of exercise you enjoy or at least kind of like. You don’t have to go full wanker and proselytize your diet and spring out of bed amped to do your workout. But you can’t hate and dread them either. You have to embrace them.

The same thing is true for the FIRE method you choose. It has to be the one that is sustainable and realistic. LeanFIRE is probably not sustainable for most people nor is FatFIRE realistic for most of us.

But those two methods are extremes on opposite ends. The ones in the middle, most of us can do one or the other of those.

But really, LMMFIRE is the best one. Do that. See you around the CampFIRE.

Show Notes

Side Squeeze by Gun Hill Brewing: A farmhouse ale

Hip to the Lingo WeldWorks Brewing: A New England Style IPA