- Discover it Secured

- Capital One Secured Mastercard

- Petal Visa Credit

- Capital One Platinum Credit Card

- Discover it Student Cash Back

- Bank of America Travel Rewards Credit Card For Students

- Chase Freedom Unlimited

- Spark Classic From Capital One

A credit score is essential; well, a good credit score is vital. No credit score is a problem. And one of the best ways to build credit is the responsible use of a credit card. But it can be tough to be approved for a credit card if you have a thin credit profile. We have a solution. These are 6 credit cards for people with no credit.

Credit cards get a bad rap. What’s the first thing that pops into your head when you hear the words “credit card?” Credit card debt, probably. And for good reason.

The average American has a credit card balance of $4,293, according to the latest Experian data. Total credit card debt is also at its highest point ever, surpassing $1 trillion, the Federal Reserve found.

But used correctly, a credit card is excellent for building credit. And like it or not, you need to have a credit history and a credit card to do things like borrow money for a car or a home and rent a car or hotel room.

Credit cards aren’t handed out quite so freely as they were just two decades ago when anyone with a pulse could be approved for a whole stack of them. It’s more difficult to get a credit card, but you’ll have a better chance when you apply for credit cards for people with no credit.

What is a Credit Score?

A credit score is a three-digit number used by banks and other financial institutions to determine how responsible you are with money. Your credit score is based on your credit history, which is contained in your credit report.

Your credit report is a list of your various accounts, past, and present, like student loans, credit cards, personal, car, and mortgage loans. It can also contain information on accounts that were sent to collections agencies for things like unpaid utility or medical bills.

Your credit report tells potential lenders how well you managed these accounts. Did you pay your bills on time or were you often late? How often?

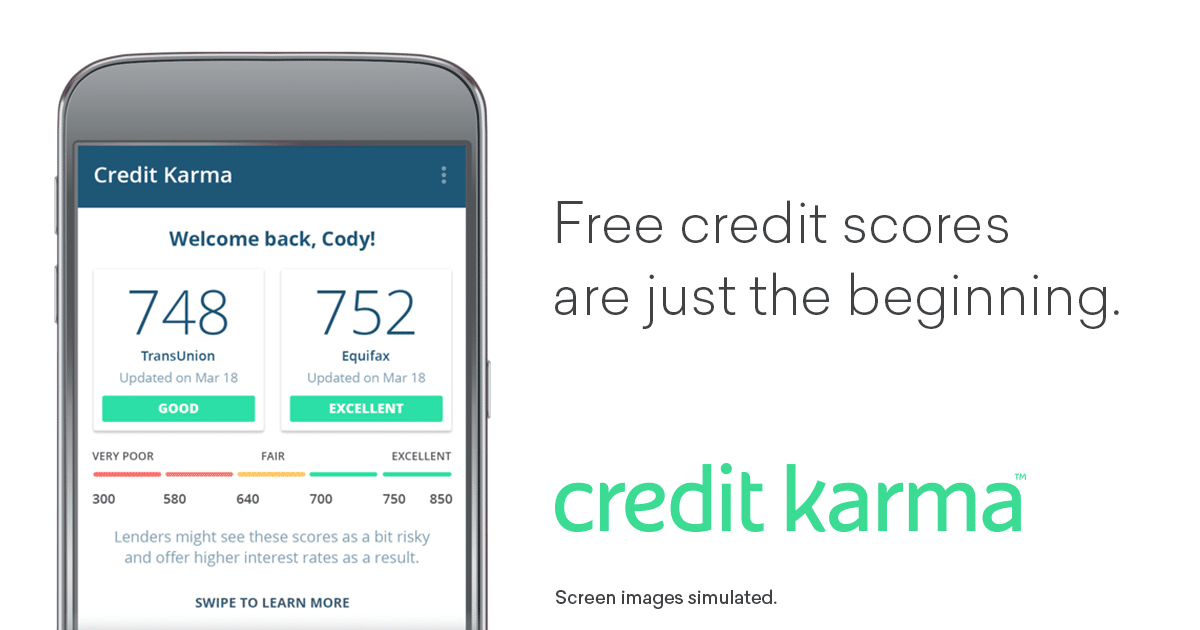

There are various formulas used to turn this data into a credit score, and the range of credit scores can vary by method, but the differences are small. Essentially, credit scores look like this:

~300-630 is Bad or poor.

~630-689 is Fair.

~690-719 is Good.

~720-850 is Excellent.

If you don’t know your credit score, you can get free online access at Credit Karma on desktop or the mobile app for free.

The credit bureaus calculate your score based on these components:

-Payment History: Whether or not you pay your bills on time. Even one late payment can hurt your score, and you may face a late fee and interest charges. Never miss a due date!

-Credit Card Utilization: How much of your available credit is being used. Ideally, this number is under 30%.

-Derogatory Remarks: Accounts that have been sent to collections, bankruptcies, and civil judgments.

-Length of Credit History: How long you’ve had credit averaged over all accounts.

Total Accounts: How many credit accounts you have and how many different types. Credit cards are one type, a mortgage another, a car loan, another, etc.

Why You Need a Good Credit Score

The most important reason it’s essential to have a good credit score is that it makes borrowing money cheaper, a lot cheaper. If you borrowed $100,000 to buy a home with an interest rate of 3.92% on a 30-year mortgage, the total cost of the loan is $170,213. If you get an interest rate of 3%, not even a full point lower, the total cost is $151,777. That seemingly small difference saves you more than $18,000.

How good? A score of 760 or higher is enough to get the best interest rates on borrowed money.

Interest rates are the best reason to have a good credit score but not the only one. Some insurance companies offer lower rates to those with good credit, most landlords will run a credit check and may not rent to those with poor or no credit, and there are specific jobs that require applicants to have a good credit score.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

The Best Credit Cards for People With No Credit

Not all credit cards have the same approval requirements. A really good rewards credit card like the Chase Sapphire Reserve is not going to approve an applicant with a limited credit history or no credit history.

And each time you apply for a credit card, it shows up on your credit report and lowers your credit score by a few points. So you don’t want to apply for cards you have no hope of being approved for.

A rejection is nothing more than a necessary step in the pursuit of success.

Tweet ThisAnd not all credit card offers are the same; you want a card that works for you. Choose one of these 6 best credit cards for people with no credit. Let’s find your first credit card!

Best Secured Credit Cards

A secured credit card requires users to pay a cash, sometimes refundable security deposit. For some cards, the deposit is the line of credit, but some cards give users a higher limit. A secured card reduces the risk for the credit card issuer. If you don’t pay your credit card bill, the issuer keeps your security deposit.

The point of having a secured card is to open one that reports to at least one credit bureau and to use the card responsibly enough to transition to a non-secured credit card eventually. A debit card or prepaid card is not the same thing and offers no credit building benefits as the activity is not reported.

Discover is one of the friendlier credit card companies for people with no credit, and the Discover it Secured card comes with some excellent benefits a lot of other secured credit cards don’t have.

There is no annual fee, your payment history will be reported to all three of the major credit bureaus, and your account undergoes automatic reviews in the eight-month. With responsible card use, you may qualify to upgrade to an unsecured card.

But it gets even better! Many secured cards don’t come with any sexy perks, but the Discover it Secured card is a cashback rewards card. Card members earn 2% cashback up to $1,000 at gas stations and restaurants each quarter and 1% back on all other purchases.

Discover also matches all of your cashback earnings at the end of your first year of membership. Users will get a free FICO score each month so you can watch your credit score grow.

If approved, you’ll secure your credit line with an equal security deposit, a $200 deposit is a $200 credit limit, $500 is a $500 limit, and so on. The minimum deposit is $200, and the maximum is $2,500. When you close your account and pay your balance in full, you get the deposit back.

The Capital One Secured Mastercard has no annual fee, your payment history will be reported to all three of the major credit bureaus, and you can get a higher credit line after making your first five monthly payments on time without having to give an additional deposit.

This card doesn’t use your security deposit as your credit limit. You can get a $200 limit with a deposit as little as $49.

Best Unsecured Credit Cards

An unsecured credit card or “real” credit card doesn’t require users to put down a security deposit or any other collateral for approval. Traditional credit cards are unsecured and can be hard but not impossible for people with no credit to get.

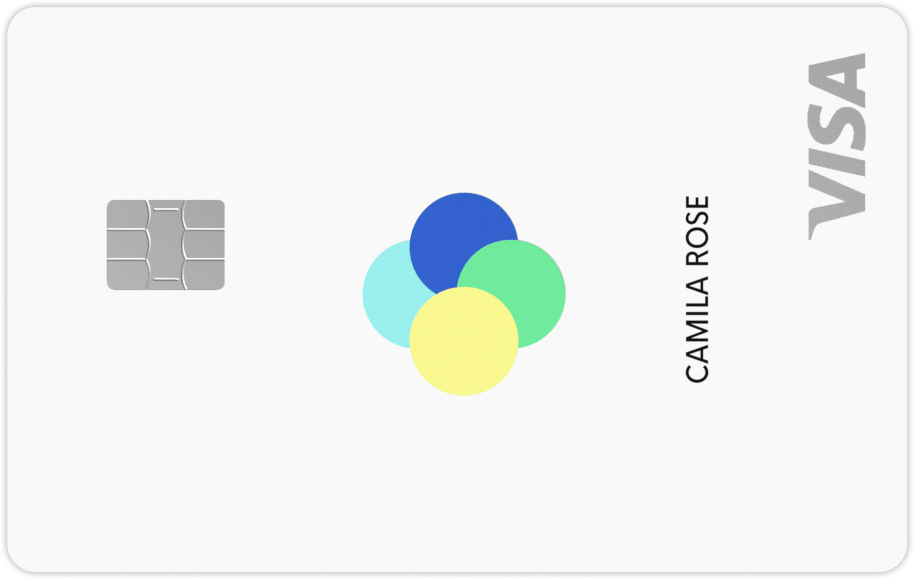

Petal understands that not everyone has a credit history, so it uses the information that your bank account shows to approve you for this unsecured credit card.

Applicants give Petal permission to see their banking information, including their checking account. Petal uses this information to determine what your cash flow looks like.

The Petal Visa Card comes with no annual fee, reports to all three major credit bureaus, and gives users cashback. You’ll earn 1% back immediately, 1.25% back after making six on-time monthly payments, and 1.5% back after making twelve on-time monthly payments.

Users can get a credit limit between $500 and up to $10,000 depending on the information gleaned from your bank account. When Petal sees a jump in your income, it will increase your credit limit.

This Capital One Card has no annual fee, reports to all three major credit bureaus, and may offer users an increased credit limit after five months of on-time payments. The minimum credit limit for new account holders is $300. Depending on your income, that limit can be as much as $1,500 to start.

This Capital One Card doesn’t offer any rewards, but many of its other cards provide cashback. The Capital One Quicksilverone Cash Rewards Credit Card requires users to have average credit and offers 1.5% unlimited cashback on all purchases.

There is a $39 annual fee, but users can recoup that in cashback if they spend at least $2,600 on the card each year. If you’re looking to “graduate” early, you can go from the Platinum Card to the Quicksilverone pretty quickly while continuing to build your credit.

Best Student Credit Cards

If you are a college student, choose a starter credit card aimed at students rather than any of the other credit cards for people with no credit on this list. These student rewards cards not only have credit building benefits but offer perks that will appeal to those in college.

This offering from Discover has no annual fee, reports to all three major credit bureaus, and offers great rewards. Users get 5% cashback in categories that change quarterly, including gas stations, Amazon, grocery stores, and restaurants, and 1% back on all other spending. Additionally, members will get double the cashback they earned at the end of their first year of card membership.

Discover wants to pay students for their good grades too! For each year you have a GPA of 3.0 or higher for up to five years, students get a Good Grades Rewards $20 statement credit.

Discover provides Social Security number alerts. If your Social Security number is found on any of thousands of dark web sites, you’ll be notified. You’ll also be notified of any new credit cards, mortgages, or other accounts that are opened on your Experian credit report. Discover offers $0 fraud liability; cardmembers are not responsible for fraudulent charges on the card.

A travel rewards card is great for students who attend college an airplane trip away from home, but most travel rewards cards require a good or excellent credit score, so they miss out. But this card from Bank of America lets students get in on those free flights and hotel stays.

The card has no annual fee, no foreign transaction fee, reports to TransUnion, and has an excellent sign-up bonus, something most credit cards lack for people with no credit.

As an intro offer, users will get 25,000 points after spending $1,000 in the first 90 days of opening the account. The points can be redeemed for a $250 credit on travel spending. You’ll continue to earn points, 1.5 per $1 spent on all purchases.

Best Rewards Credit Cards

Rewards credit cards have great perks, including cashback and travel rewards, but they’re usually reserved for those with good credit and at least some credit history. But these cards give people with no credit a chance to build some while scoring rewards at the same time.

This Chase card has no annual fee, reports to all three major credit bureaus, and has a 15 month 0% intro APR period on purchases and balance transfers, great for those who may have already opened a credit card and gotten behind on payments.

The balance transfer fee is 3% of the amount transferred with a $5 minimum. After the intro APR, the card reverts to a regular APR of 16.99-25.74%.

Another of the credit cards for people with no credit that has a sign-up bonus! Users will get $200 cashback after spending $500 in the first three months of opening the card.

Users also earn 3% cashback on every dollar they spend in the first year up to $20,000 in spending and an unlimited 1.5% back on all purchases after that.

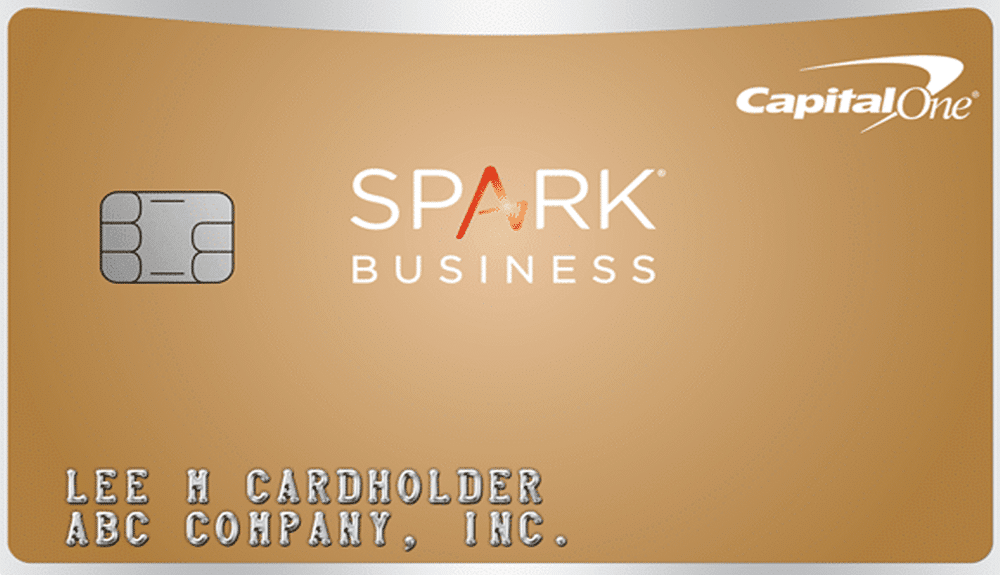

Even if you have a credit history, when you start a new business, the business does not. And for tax reasons, you want to keep your personal and business expenses separate. And if you have a lot of business expenses, it can be beneficial to find a good cash back card.

The Spark Classic has you covered on both counts. This Capital One card has no annual fee, reports to both business and personal credit bureaus, and allows the cardholder to get additional cards for employees at no cost. Card members also earn 1% cashback on all purchases (those made on employee cards, too).

Other Ways to Build and Improve Credit

Whether you have no credit or bad credit, a credit card account isn’t the only way to build credit or improve credit. If you have student loans, be sure to pay them on time. Student loan payments are reported to the credit bureaus.

An auto loan is typically easy to get and is reported. Be responsible, don’t buy more car than you can comfortably afford and make your payments on time.

Some banks and credit unions offer credit building loans. These loans work much like secured credit cards work. You provide a security deposit and borrow against that amount and pay it back through monthly payments. Be sure the lender reports payments.

Your rent is probably your most significant expense, and the one you’re least likely to pay late, so why not use that to help you build credit?

Most landlords don’t report on-time rent payments, but some companies will report them for you. Some companies provide this service, including PayYourRent, RentalKharma, and Rent Reporters.

These companies charge various fees, and you may need your landlord to agree to verify your payments to them. And when rent payments are listed on your credit report, they may not always be factored into your credit score. Check with the company before joining.

Faster Than You Think

How long does it take to build credit from scratch? Not long.

According to Experian, one of the major credit bureaus, it takes between three and six months of regular credit activity for your file to become thick enough that a credit score can be calculated.

And once you build up a solid credit score, keep it. It’s much harder to repair bad credit than to establish a credit history.

![A Good Credit Score Saves You Money and Here’s How [UPDATED]](https://www.listenmoneymatters.com/wp-content/uploads/2014/07/LMM-Cover-Images-29-768x432.jpg)

![Chase Credit Journey: A Free Credit Monitoring Service [REVIEW]](https://www.listenmoneymatters.com/wp-content/uploads/2020/03/chase-credit-journey-featured-768x432.png)

![What Is Credit and Why It’s Essential to Your Financial Health [UPDATED]](https://www.listenmoneymatters.com/wp-content/uploads/2020/02/what-is-credit-featured-768x432.png)