There are tons of credit cards out there, and while having options is great, it can also get overwhelming fast. We’ve done the hard work and read the fine print, so you don’t have to. Whether you’re after rewards, cash back, low interest, or a credit-building tool, we’ll help you find the right credit card for your lifestyle—and score some great perks along the way.

Credit cards often get a bad rap—and for good reason. If you don’t use them wisely, it’s easy to rack up thousands in debt. And this isn’t rare. Millions of Americans carry credit card balances every month, often paying high interest on everyday purchases.

Used right, though, credit cards can be helpful tools. The key is knowing how to manage them without falling into a debt trap.

More than 48% of all US households carry credit card debt, with the average American household carrying a balance of $6,580. For only indebted households, which excludes people who pay their balances in full every month, the average debt is $10,560.

Credit cards aren’t the enemy. In fact, the right card can be a smart money tool when used wisely. Just like tools in a toolbox, some credit cards are better for certain financial goals. If you’re struggling to pay off a balance, you’ll need a different type of card than someone who spends a lot on travel.

Not every credit card is within reach—approval depends on your credit score and history. And since applying can ding your score, you want to be smart about it. With so many options out there, finding the right card might seem tricky, but it doesn’t have to be. Whether you’re building credit, paying off debt, or looking for rewards, we’ll help you pick a credit card that fits your goals and gets you the most value.

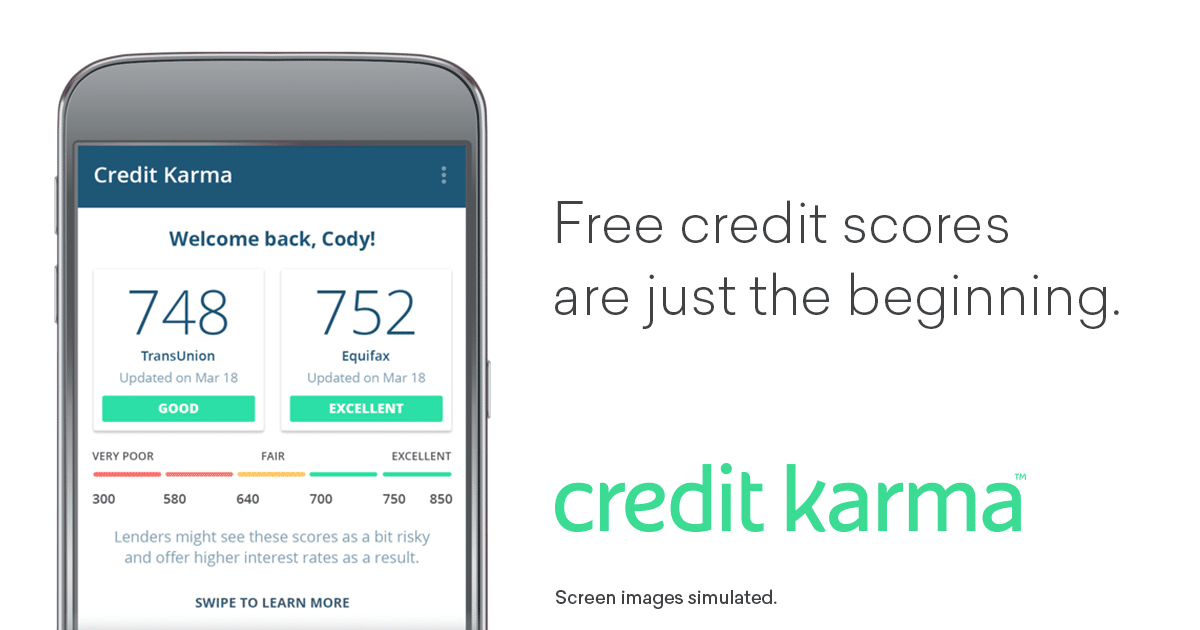

First Things First: Know Your Credit Score

The credit cards you qualify for mostly depend on your credit score. You don’t need a perfect 850, but a good credit score—usually 700 or higher—gives you a strong shot at top-tier rewards cards. Lenders also look at things like your income, payment history, and debt load, but your score is one of the biggest factors. So if you’re aiming for premium perks, make sure your credit is in good shape before applying.

If you don’t know your credit score, you can create a free account with Credit Karma and see your score there.

Improve Your Credit Score

Of course, there are plenty of good reasons to build a strong credit score beyond scoring the best rewards cards. Your credit score affects the interest rates you’ll get when borrowing money to buy a home, finance a car, refinance student loans, pay off credit card debt, or even launch a business.

Borrowers with a credit score of 760 or higher are generally eligible for the most competitive interest rates, though some lenders begin offering top rates around 740. A higher credit score means lower interest rates, saving you money on things like mortgages, auto loans, and credit cards.

If you have bad credit or limited credit history, you can improve or build your credit score with the right steps and consistency.

How to Choose a Credit Card

Not all credit card offers are the same, so it’s important to know what to look for before you apply. Some cards are great for rewards, others for balance transfers—but the key is finding one that matches your spending habits and financial goals.

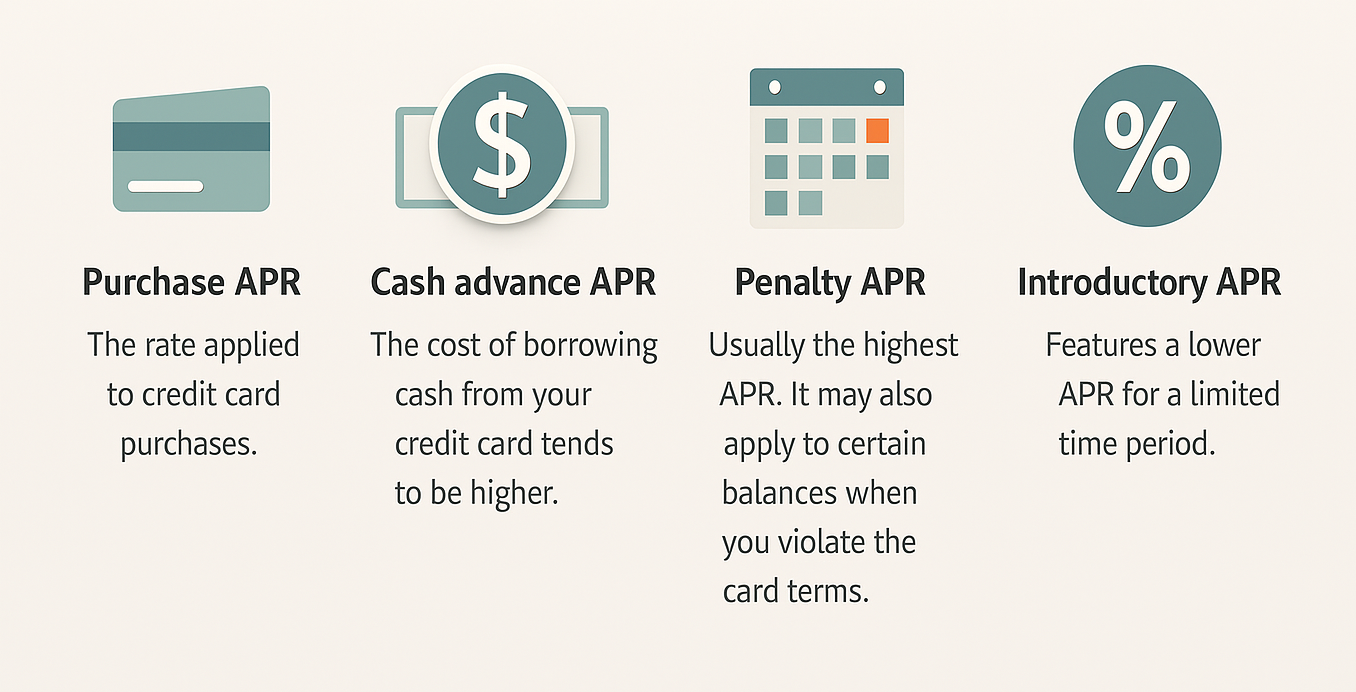

Annual Percentage Rate (APR)

The APR, or annual percentage rate, is the interest you’ll pay if you carry a balance on your card. Credit card interest is calculated using your average daily balance, which means the longer you carry debt, the more you’ll pay.

Lower APRs are always better, but your rate will depend on your credit score and the card issuer. As of early 2025, the average APR on new credit cards is around 22.59%, and even higher for those with fair or poor credit. While you might see teaser rates advertised, make sure to read the fine print so you know what you’re actually signing up for.

Introductory Rate

A credit card with a solid introductory rate can be a smart personal finance tool in two situations: when you have a large expense coming up or when you’re trying to pay off an existing credit card balance.

Some credit cards offer 0% or low introductory APRs on purchases and balance transfers. The best balance transfer cards come with a 0% intro APR, no transfer fee, and a long promotional period. Most offers last between 6 and 18 months, but some cards extend that to as long as 21 months, giving you more time to pay off your balance interest-free.

If you’re planning a big purchase, these intro offers can work like an interest-free loan—as long as you pay it off before the regular APR kicks in. For existing debt, transferring your balance to a new card during the intro period means your payments go entirely toward reducing the balance, not interest. That can save you a lot of money in the long run.

Paying off your full balance before the intro period ends means you’ll avoid interest charges entirely—and that’s money back in your pocket.

Fees

Credit cards can come with a range of fees, and your goal should be to avoid them whenever possible. Some of the most common—and avoidable—credit card fees include the following:

Annual Fee: This is the yearly cost of carrying a specific credit card, often linked to travel or premium rewards cards. Some cards waive it the first year, but after that, it can run anywhere from $95 to $500 or more. If the perks justify the price—like lounge access or travel credits—it might still be worth it.

Foreign Transaction Fee: This fee is charged—typically up to 3%—is charged every time you use your card outside the U.S. or make purchases from international sellers. Many cards have dropped this fee entirely, but double-check if you travel or shop internationally.

Balance Transfer Fee: When you move debt from one card to another, this fee—usually 3% to 5%—applies. Even with a 0% intro APR, the cost can add up. Some cards waive this fee during the promotional window, so compare offers closely.

Cash Advance Fee: If you use your credit card to withdraw cash, expect to pay a cash advance fee—usually around 3% to 5% of the amount or a flat fee like $10, whichever is greater. Plus, interest starts immediately, often at a higher rate than normal purchases.

Late Payment Fee: Miss a payment and you could be hit with a late fee of up to $41. Even worse, your interest rate might go up and your credit score could take a hit. Set up autopay or reminders to stay on track.

Sign-Up Bonus

A good sign-up bonus can score you serious value—like cash back, travel rewards, or free hotel stays. Credit card companies use these bonuses to stand out in a crowded market and attract new customers.

If you have good to excellent credit, don’t overlook this perk. Many cards offer $200 or more in value when you meet the minimum spend within the first few months. Whether you want points, miles, or cash, a sign-up bonus can be a smart way to maximize your new card right from the start.

Churning over at Reddit is on top of this and any other credit card perk related subject. Before you apply for a rewards card, check it out. Somehow they seem to know things like, “Card X has a 30,000 point sign-up bonus now but if you wait until August 1, it will be 75,000 miles.”

Rewards

There are two main types of credit card rewards: cash back and travel rewards. Travel rewards—especially sign-up bonuses—can look flashy and tempting, which is why they attract so many people shopping for a new card.

But travel rewards can offer real value too. You can earn perks like free flights, hotel stays, free checked bags, or credits toward programs like Global Entry or TSA Precheck. Just make sure they fit your lifestyle—if you don’t travel much, you may get more value from a simple cash-back card.

If you only fly once or twice a year, prefer staying at Airbnb over hotels, or rarely travel internationally, a travel rewards card might not be your best fit. You could snag a nice sign-up bonus, but you probably won’t earn enough points from day-to-day spending to make it worth keeping long-term.

If that sounds like your situation, a solid cash back credit card is likely a better fit. You can still grab a generous sign-up bonus—often worth a few hundred dollars—and keep earning cash back on the things you already buy.

Before picking a card, check your spending patterns. Use your Mint account or bank statements to see where your money actually goes. If you spend a lot on groceries, gas, or dining out, look for a card that rewards those categories to maximize your earnings.

Some cashback cards give cardholders a flat percentage back on all purchases, and some give a higher rate back on certain kinds of spending like grocery stores, gas stations, and office supply stores.

Protections

Using the right credit card gives you access to built-in protections that can save you money and stress. These vary by card, so always read the fine print to understand what’s covered.

Fraud Protection: By law, your liability for unauthorized charges is capped at $50—and it’s usually $0 if you report your card lost or stolen before any fraudulent activity happens.

Purchase Protection: If something you buy with your card gets damaged or stolen within a set period—usually up to 90 or 120 days—your credit card may reimburse or replace it.

Price Protection: If the price of something you recently bought drops, some cards will refund the difference within a 60—to 90-day window. This perk is rare now, but it’s worth checking for.

Return Protection: If a seller won’t accept a return on an item in good condition, your credit card might still cover the cost—typically within 60 to 90 days of purchase.

Travel Insurance: Depending on the card, this can include trip cancellation or delay, lost luggage, emergency medical coverage, or accident insurance. Coverage varies, so review the terms.

Rental Car Insurance: If your card offers rental coverage, you can decline the rental company’s insurance. It usually covers theft and collision damage—but not all cars or situations qualify, so read the details.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

The Best Credit Cards for You

Finding the right credit card is easier than you think—no matter your credit score, spending habits, or goals. Start by focusing on what matters most to you:

- Want to earn cash back? Look for cards that reward everyday spending like groceries, gas, or dining out.

- Travel often? Go for a card that offers travel points, perks like airport lounge access, and no foreign transaction fees.

- Need to pay off debt? Consider a balance transfer card with a 0% intro APR to save on interest while you pay it down.

- Building or rebuilding credit? Secured and student cards can help you build a strong credit history.

There’s no one-size-fits-all card—but with a little research, you can find one that matches your lifestyle and financial goals.

Credit Cards for Those With No Credit or Bad Credit

If you have little or no credit history—or your credit score has taken a hit—it can feel like you’re locked out of the best credit card options. You probably won’t qualify for those flashy rewards cards just yet, but that doesn’t mean you’re out of luck.

You can still get a credit card designed specifically for building or rebuilding credit. With responsible use—like paying on time and keeping your balance low—you’ll strengthen your credit and eventually qualify for better cards down the road.

Discover it Secured

Discover it® Secured Credit Card

The Discover it Secured card is a strong choice if you’re building or repairing your credit. It functions like other secured credit cards, but comes with extra perks you won’t always find at this level.

- Refundable security deposit: Your credit limit is based on the amount you deposit, starting at $200.

- Reports to all three credit bureaus: On-time payments help you build a positive credit history.

- No annual fee: There’s no cost to keep the card open, which is great while you’re rebuilding credit.

- Automatic reviews for upgrade: After seven months, Discover will check if you qualify for an unsecured card and can return your deposit.

- Cash back rewards: Earn 2% back at gas stations and restaurants (on up to $1,000 in purchases per quarter) and 1% on everything else.

Most secured cards skip rewards, but Discover gives you real earning potential while you work on improving your credit score.

This card is a good fit if you have limited credit history or a score of around 660 or lower.

Petal Visa Credit

Petal 2 Visa® Credit Card

The Petal 2 Visa® Credit Card is designed for individuals seeking to build or rebuild their credit without the need for a traditional credit history. Instead of relying solely on credit scores, Petal evaluates your banking history to assess eligibility.

- No Credit History Required: Petal assesses your income, savings, and spending habits by analyzing your bank account activity, making it accessible to those new to credit.

- Cash Back Rewards: Earn 1% cash back on all purchases immediately upon account opening. After six on-time monthly payments, this increases to 1.25%, and after twelve on-time monthly payments, it rises to 1.5%.

- No Fees: Enjoy no annual fees, late fees, foreign transaction fees, or any other hidden fees.

- Credit Reporting: Petal reports to all three major credit bureaus, aiding in building a positive credit history with responsible use.

- Credit Limit Increases: Through the Leap program, you may qualify for a credit limit increase after six months of responsible use.

By focusing on your financial behavior rather than just your credit score, the Petal 2 card provides a pathway to establish and improve your credit profile.

You don’t need a credit score to be considered for Petal—approval is based on your income, spending habits, and overall financial history.

Best Student Credit Cards

College students can apply for regular starter credit cards, but student credit cards are built specifically with their needs in mind. They’re easier to qualify for and often come with perks tailored to student life.

Bank of America Credit Cards for Students

Bank of America offers several student credit card options that help you earn rewards and build credit while in school:

- Bank of America® Customized Cash Rewards Credit Card for Students: Earn 3% cash back in a category of your choice—like gas, online shopping, dining, or travel—plus 2% at grocery stores and wholesale clubs, and 1% on everything else.

- Bank of America® Travel Rewards Credit Card for Students: Get unlimited 1.5 points per dollar on all purchases. Points can be redeemed for travel, dining, and more with no expiration dates.

- BankAmericard® Credit Card for Students: A good choice for those focused on building credit while avoiding interest. It includes a low intro APR on purchases and balance transfers.

These cards are designed to support smart spending and credit growth, whether you’re just starting out or looking for flexible reward options.

Discover it Student Cash Back

The Discover it Student Cash Back card is a solid choice for students looking to build credit and earn rewards. It’s packed with student-friendly perks and doesn’t require a strong credit history to apply.

- Cashback rewards: Earn 5% cash back in rotating categories like grocery stores, restaurants, and Amazon (up to the quarterly max when activated), plus 1% back on all other purchases.

- 0% intro APR: Get a 0% APR on purchases for your first six months. After that, a standard variable APR applies.

- First late payment forgiveness: There’s no fee for your first late payment, and your APR won’t go up if you pay late.

- Cashback Match: Discover will automatically match all the cash back you’ve earned at the end of your first year—no limits or sign-ups required.

- Good Grades Reward: Earn a $20 statement credit each school year your GPA is 3.0 or higher, for up to five years.

- Ideal for new credit users: This card is designed for students with limited or no credit history, making it a great entry point for responsible credit building.

Between its rewards, no annual fee, and student-specific perks, this card offers real value while helping you start your credit journey on the right foot.

Best Balance Transfer Credit Cards

If you’re carrying high-interest credit card debt, a balance transfer card with a 0% intro APR can help you pay it off faster and save big on interest.

Chase Slate Edge

The Chase Slate Edge℠ card is a solid option for paying down debt or financing a large purchase. While it doesn’t offer rewards, it’s built to help you manage interest and improve your credit profile.

- 0% intro APR: Get a 0% intro APR on purchases and balance transfers for 12 months. After that, a variable APR applies.

- Balance transfer terms: Transfers must be made within 60 days to qualify for the intro rate. A balance transfer fee of 3% applies (5% after 60 days).

- APR reduction opportunity: You may qualify for a 2% APR reduction when you pay on time and spend at least $1,000 in your first year.

- Credit limit review: Automatic credit line evaluation for potential increases when you meet the above conditions.

- No annual fee: There’s no annual fee, making it a low-cost option to manage balances or finance purchases.

While this card doesn’t offer rewards or travel perks, it’s ideal for tackling high-interest debt or improving your credit through responsible use.

Chase Freedom Unlimited

The Chase Freedom Unlimited card remains a strong option for cash rewards and balance transfers. Here’s the updated information as of April 2025:

This card does have a balance transfer fee—3% of the amount transferred within the first 60 days of account opening (minimum $5), increasing to 5% thereafter. It offers a 0% introductory APR for 15 months on purchases and balance transfers, followed by a variable APR of 18.99%–28.49%.

The sign-up bonus has increased to $250 after spending $500 in the first three months of opening the account. Users earn 1.5% cashback on all purchases, with elevated rewards of 3% on dining and drugstore purchases and 5% on travel booked through Chase Travel℠. There is no annual fee, and a minimum credit score of 670 (good credit) is typically required for approval

Best Cash Back Credit Cards

Maximize every dollar you spend with a cash back credit card that rewards your everyday purchases—whether it’s groceries, gas, or online shopping.

Blue Cash Preferred Card from American Express

This is one of the best cash back credit cards for people who spend a lot at grocery stores—because let’s be honest, who doesn’t? Even if you’re not big on cooking, you still need household essentials like trash bags and paper towels, and you can grab those at most grocery stores too. Plus, this card offers great cash back in other everyday categories.

The annual fee is $95 (currently waived the first year), and there’s a sign-up bonus of a $250 statement credit after spending $3,000 in the first six months.

- 6% back at U.S. supermarkets on up to $6,000 per year in purchases (then 1%)

- 6% back on select U.S. streaming services

- 3% back on transit including taxis, rideshares, parking, tolls, trains, buses, and more

- 3% back at U.S. gas stations

- 1% back on all other purchases

If you spend around $30 a week at the grocery store, you’ll nearly earn back that annual fee in rewards alone. In most cases, it more than pays for itself.

The minimum recommended credit score is 690.

Citi Double Cash Card

You can definitely find cards with higher cash back rates—but most only offer those rewards in rotating categories. On top of that, you often have to activate those categories every quarter and then remember what they are. Honestly, who has time for that?

That’s why we like this Citi card. It has no annual fee, offers an 18-month 0% APR on balance transfers, and gives you 2% back on every purchase—1% when you buy, and another 1% when you pay it off. It’s simple, consistent, and low effort.

As of April 2025, Citi now also offers a $200 cash back welcome bonus after spending $1,500 in the first six months. That’s a nice new perk.

The minimum recommended credit score is 700.

Best Travel Rewards Credit Card

These are the most fun kind of travel rewards credit cards, lots of great perks, and typically outstanding sign-up bonuses too.

Chase Sapphire Reserve

This is considered by “professional” travelers to be the king daddy of travel rewards cards—and you’ll probably agree. The sign-up bonus is excellent: 60,000 points after spending $4,000 within three months of opening the card. That’s worth $900 in travel when booked through Chase or $600 as a statement credit.

We did an in-depth review of this card, and you can read all the details there. I have the “little brother” to this card, the Chase Sapphire Preferred. It’s a great travel card too, but I reallllly want the Reserve. The $550 annual fee has been a sticking point, but I’ve been traveling more, so I think I can finally justify it!

-

- $300 annual travel credit automatically applied to travel purchases

- 3x points on dining and other travel, 10x on hotels and car rentals, and 5x on flights booked through Chase Travel

- Complimentary Priority Pass™ Select membership for 1,300+ airport lounges worldwide

- Up to $100 credit for Global Entry, TSA PreCheck®, or NEXUS every 4 years

- Trip cancellation, rental car damage waiver, lost luggage, and other premium travel protections

The minimum recommended credit score is 750.

Capital One Venture Rewards Credit Card

Some people make a hobby—and even a living—out of “travel hacking” credit card rewards. If you get it right, you can save a ton and enjoy perks like free upgrades. But let’s be honest: it’s a skill with a lot of moving parts. Some frequent travelers just don’t want the hassle. This Capital One card is for them.

The Capital One Venture Rewards Credit Card has a $95 annual fee and no foreign transaction fees. New cardholders can earn a generous 75,000 bonus miles after spending $4,000 within the first three months, plus a one-time $250 Capital One Travel credit during the first year. That’s up to $1,000 in travel value if redeemed wisely.

- Earn unlimited 2 miles per dollar on every purchase

- Earn 5 miles per dollar on hotels and rental cars booked through Capital One Travel

- Up to a $100 credit for Global Entry or TSA PreCheck® application fees

- No minimum to redeem miles for travel-related statement credits—cover even small purchases like a $6 Uber

- Miles never expire and there’s no cap on how many you can earn

The minimum recommended credit score is 700.

Choose Wisely

Choosing the right credit card is easier than it seems—just match the type of card to your needs and make sure your credit score meets the requirements. Using it smartly is just as simple: avoid charging anything you wouldn’t be able to pay for in cash. That way, you stay out of debt and build your credit at the same time.

Debt is the worst poverty.

Tweet ThisWe get it—things don’t always go as planned. Credit cards can be helpful tools, but if you’re not confident you’ll use one responsibly, it might be better to skip it for now. The rewards and perks are nice, but no bonus is worth the stress of falling into debt you can’t manage. Stay focused on your financial health first.

Show Notes

The Andrew Sangria – Rum, wine, triple sec, and sprite. Perhaps Andrew will delight us and share his actual recipe. I’ll ask him. (edited by Andrew) For the record, who has time to measure ingredients? You’ll know you’ve done it right if you still taste the rum ;)

Podcast Correction:

In case you’re too lazy to scroll down much, further, I’d like to point out that we made a mistake in the episode. You can’t use prepaid cards to build credit, but you CAN use secured cards to. A similar idea only there’s actual credit usage involved with secured cards. Thanks goes out to Kyle Russell for catching this one!