If you are investing, you probably have money in an index fund but you even really know what an index is? It’s important in a world with so many investment choices to educate yourself wholly on the types of investments vehicles you’re involved with. So what is an index fund?

It’s time to educate yourself. Know what you invest in, and I promise never to use the word ‘wholly’ again.

What type of investor do you want to be?

That’s what I thought! And, as the famous investor Peter Lynch says,

Most investors would be better off in an index fund.

Like Lynch, most common sense investing advice for non-professional investors says that you should buy an index fund, and sit on it.

You tend to get reduced fees, and historically active stock picking hasn’t outperformed the major indexes. And, ultimately, it’s less work for you to manage.

It’s fairly solid advice, and with companies like Vanguard or

If you know what an index is, do you know how it’s put together? Let’s dive deeper into these topics.

What exactly is an index fund?

Let’s start with the basics, what is an index fund?

The major US indices that you hear about on the news are the Dow Jones Industrial Average (Dow/DJIA), the NASDAQ Composite, and the S&P (Standard & Poor’s) 500. One thing to keep in mind with each of these indices is that the member companies can, and do, change.

This helps partially explain why the market is always moving because if a company no longer fulfills the criteria of that index fund, it’s dropped and someone new replaces it.

However, if you own an investment vehicle that matches an index, you get the benefit of the change without having to do the work of selling and reinvesting.

Before we go deeper into the different indexes, I want to cover a couple of terms that will help make this article make more sense.

Market Capitalization – Often shortened to market cap, it’s a strong indicator of company size. Measured by multiplying the number of outstanding shares (stock owned by shareholders) by the current price of the stock.

Blue Chip – large, high-quality companies. Investopedia has an interesting write up on the history of the term.

Ready? Let’s dive into index funds.

Key things to know about index funds

1. Index fund investing allows you to match market performance

If you’ve never invested before, you might think that taking bigger risks in an attempt to outperform the market is the best way to increase your principal, but this isn’t typically the case.

When you invest in an index fund, you are likely to match the growth of the market as a whole rather than experiencing major drops or spikes that might occur with single stocks.

This gives you the opportunity to grow your investment without assuming the same sort of risk that comes with trying to beat the trajectory of the market.

2. Investors in index funds enjoy the benefits of broad market exposure

With index funds, you can buy into many different companies by investing in shares of the fund. This gives you the chance to benefit from the overall growth of various market indices, even if specific companies underperform.

3. Index funds are versatile and diverse

There are many different market indices that you can choose from when you invest in index funds. You can select an index that focuses on companies with smaller capital values, or zero in on an index for a particular industry like healthcare or transportation.

Doing so enables you to have diversified investments within particular sectors or categories of businesses.

4. Index funds are increasing in popularity

As robo-investing options become more popular among investors, passive investment opportunities, including index funds, are increasing in popularity.

This departure from more traditional, actively managed funds has greatly increased participation in index fund investment.

Fiscal flexibility that’s funny, free and delivered weekly.

Why invest in index funds

There are many reasons why index fund investing is a good choice for so many people.

For one thing, it offers a certain level of consistency and predictability, insofar as the market can be consistent and predictable.

While you might strike gold on a different investment option or lose it all on a particular stock, index funds spread your investment out across many different companies.

Because of that, they tend to mirror the growth of the market.

For long-term investments, you can expect moderate growth on an annual basis that will add up over time to greatly increase or even multiply your principal.

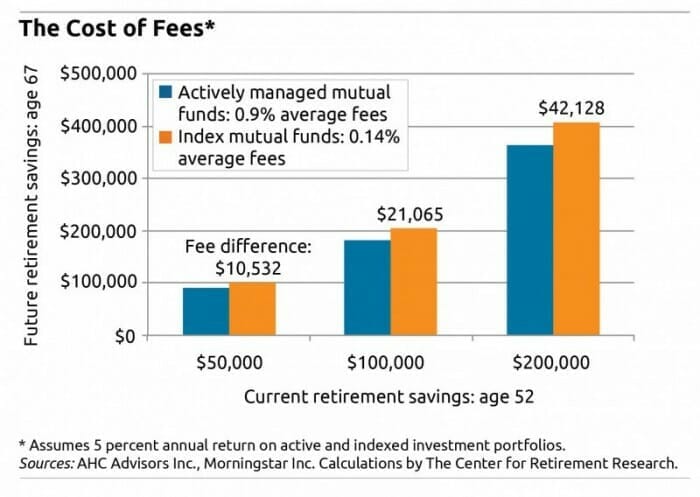

Another great reason to consider investing in index funds is the fact that you’ll spend less on fees.

Source: AHC Advisors Inc.

Actively managed portfolios tend to cost much more because they require so much hands-on management from an investment broker. Index funds don’t cost as much to manage or maintain, which means you can pay less and truly maximize your returns.

You’ve probably heard a lot about the importance of portfolio diversification, and index funds give you the chance to make diversified investments right off the bat.

You can achieve an investment portfolio that’s distributed across many different companies without all the hard work of painstakingly curating a stock portfolio.

How to invest in index funds

Considering all the great benefits of index fund investment, you are probably wondering how you can get a piece of this action!

By following a few simple steps, you can begin your foray into index funds and watch your principal grow with the market for decades to come. Now, you won’t become to Wolf of Wall Street,

…But you will slowly and steadily increase your nest egg in a safe investment vehicle.

Here’s how to make it happen:

1. Select the right fund and index for you

Before you can start investing, you’ll need to choose the fund and index into which you want to put your money.

Start by identifying a fund provider who offers the kind of investment options you’re looking for. Alternatively, you can choose to get your index funds from various providers. However this does require some additional time and effort.

Next, figure out which index you want to invest in.

Think about all the various index funds you can choose from and pick the one that has what you want and need. It’s a good idea to start by looking into the primary indexes, such as the S&P 500 and the Dow.

2. Research investment details and requirements

To get started with a mutual fund investment, you might need a sizeable upfront investment—often, a few thousand dollars. Make sure you understand the requirements that apply to the funds in which you’re interested.

Don’t worry about saving a huge amount so that you can start with a larger principle. Instead, focus on investing what you can right away so that you don’t miss the opportunity to start benefiting from market growth.

3. Shop around

Be sure to compare fees on various fund providers and try to find one with relatively low fees. You want to be able to enjoy your returns as much as possible without losing your profit to excessive account management and administrative expenses.

4. Crunch the numbers

Before pulling the trigger on an index fund investment, take a moment to think about how taxes will figure into your investment.

If you’re investing in an index fund for an IRA or 401(k), you do not have to worry so much about transactional taxes. But, be sure you are aware these matters if you have a taxable account.

Calculate your tax-cost ratio to determine what percentage of your investment’s performance will be lost to taxes.

Expected returns for index funds

The returns on index funds vary depending on several factors. However, you can generally expect your index fund to earn returns that match the growth of the market in the specific sector or industry of your index.

In other words, let’s say you’re invested in an energy sector index fund and the energy sector experiences growth of 8 percent in a given year.

In that same year, you might expect your index fund to grow by about 8 percent.

For index funds like the S&P 500, your growth would be on par with the market average—usually about 7 percent.

The top index funds

The Dow

The Dow is made up of thirty companies with a price-weighted average. It only looks at thirty companies because back in the day (it was founded in 1896) you had to do all of the calculations by hand and they thought twenty (changed in 1928 to thirty) was a good enough representation without having to do a crazy amount of work.

You took the price of the thirty companies, added it together, and divided by thirty. The process is slightly different today because the calculation includes a divisor.

It is adjusted for new companies joining the index with a different price than the one they’re replacing and to account for stock splits, which would cut the companies price by the split multiple.

S&P 500

I like using the S&P 500 as my benchmark more than the Dow. As you can certainly guess from the name, it looks at substantially more companies than the Dow though it’s named slightly incorrectly as it actually looks at 505 companies.

False advertising!

While 505 companies are clearly only a small portion of the total number, the S&P 500 includes most of the largest companies and accounts for about 80% of the total market cap.

Therefore, unless you’re looking to invest in much smaller companies, it’s a good indicator of how large-cap companies and the market as a whole are doing.

The second reason I prefer the S&P 500 over the Dow is that it’s a market-weighted index. This means that it compares the market value of the member companies day-to-day.

And, changes in the index are in proportion to the size of the companies.

NASDAQ

The NASDAQ Composite index is the final of the three major US indices. It includes all of the securities listed on the NASDAQ exchange, which is the second largest exchange in the world behind the New York Stock Exchange.

It was the first electronic stock market, the first to allow online trading and now contains the majority of the large tech companies.

Therefore the NASDAQ composite is viewed more as a tech index. Though the companies on the NASDAQ are also some of the largest in the world and are therefore included in the other indices. It’s also a market-weighted index so it’s a better representation of the actual underlying companies than the Dow.

Vanguard

The founder of Vanguard began the very first index fund, which tracked the S&P 500, in 1975. Since its inception, the Vanguard has grown to become the largest sponsor of index funds in the world.

Vanguard investors enjoy the benefits of famously low fees compared to other fund sponsors in the industry.

Thanks to its history and its accessibility, Vanguard is popular among a wide variety of investors from many different backgrounds. For some of Vanguard’s most popular index fund options, the median capital investment is less than $30,000.

This indicates that investment in Vanguard is popular even among investors without a significant amount of capital to invest in an index fund.

Here’s a curated list of investment strategies we’ve covered using index funds (Vanguard included) to build a diversified portfolio:

- Coffeehouse Portfolio

- Ivy Portfolio

- Swensen Portfolio

- Lazy Portfolio

- Larry Portfolio

- Golden Butterfly

- Minimum Variance Portfolio

- Permanent Portfolio

This portfolio's single goal is to make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is. It does this by focusing on growth and inflation cycles.

If you want to model your portfolio after an expert, Listen Money Matters is a fan of billionaire hedge fund investor Ray Dalio’s All Weather.

What are index funds: Final thoughts

Hopefully, this gives you a bit more understanding of what an index fund is. These funds pool your money to buy all of the underlying companies in the same proportions as the index they track.

This would be impossibly expensive for most investors.

Buying the index allows you to buy easy diversity which is very good for your portfolio. It does limit you to the aggregate performance of all of the companies. This means you’ll have winners and losers each yea. You are unlikely to hit any major home runs with this strategy.

But that’s fine! Slow and steady isn’t sexy, but it’ll sure make you money over the long term.

It’s not like buying Google at its IPO. However, those home runs are few and far between and only obvious in hindsight. Your strategy shouldn’t be geared towards that unless you’re already incredibly wealthy.

If you’re a normal person like me, just looking to get solid returns over time and slowly build up your portfolio then you should read, understand, and act.

Here is a list of the best Vanguard funds that we know about – you should check them out.