Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

You hear the term “fiscal responsibility” a lot when it’s time for a national election. American politicians love to talk about fiscal responsibility, fiscal policy, economic growth, national debt, and the federal budget. But when politicians hit those buzzwords, be they Democrats or Republicans, they’re talking about the federal government. But what does a fiscally responsible person look like?

To Washington, DC, fiscal responsibility is mostly something to be argued over and campaigned on, but that’s pretty much where agreement ends.

Opinions are diverse. To some, it means paying down the federal debt. To others, it means balancing the federal budget. Wrong, says another group, it means keeping the debt at a sustainable level in relation to the size of the economy. Wrong, wrong, wrong, says an emerging school of thought: it’s not about deficits and debt, it’s about outcomes, it means doing what it takes to sustain the world leadership role of the U.S. dollar and economy.

Well, being fiscally responsible seems to be beyond the United States government. I think for most of us, handling our money in a fiscally responsible manner would at least include having a balanced budget for the fiscal year, but a budget surplus would be even better.

When was the last time we achieved that? The American government had a budget deficit every year from 1970 through 1997. Democrat Bill Clinton was in office in 1998 when we finally recorded a surplus (there were budget surpluses from 1998 through 2001). According to the U.S. Department of the Treasury, in the last 50 years, the federal government budget has run a surplus only four times.

If you or I hadn’t maintained a balanced budget for most of the last 50 years, we’d likely be in a tough financial situation. While we might not have control over how the government handles its finances, we can focus on becoming the ideal fiscally responsible individual. Let’s explore the steps you can take to achieve financial stability and create a budget that works for you.

Defining Fiscally Responsible

In government speak, we are the “private sector,” so how can we define and achieve fiscal responsibility? It’s pretty basic really and while I understand the federal government has a lot more moving parts to deal with than we do, like lots of other things, (maybe everything) they make it harder than it needs to be.

You Have a Budget

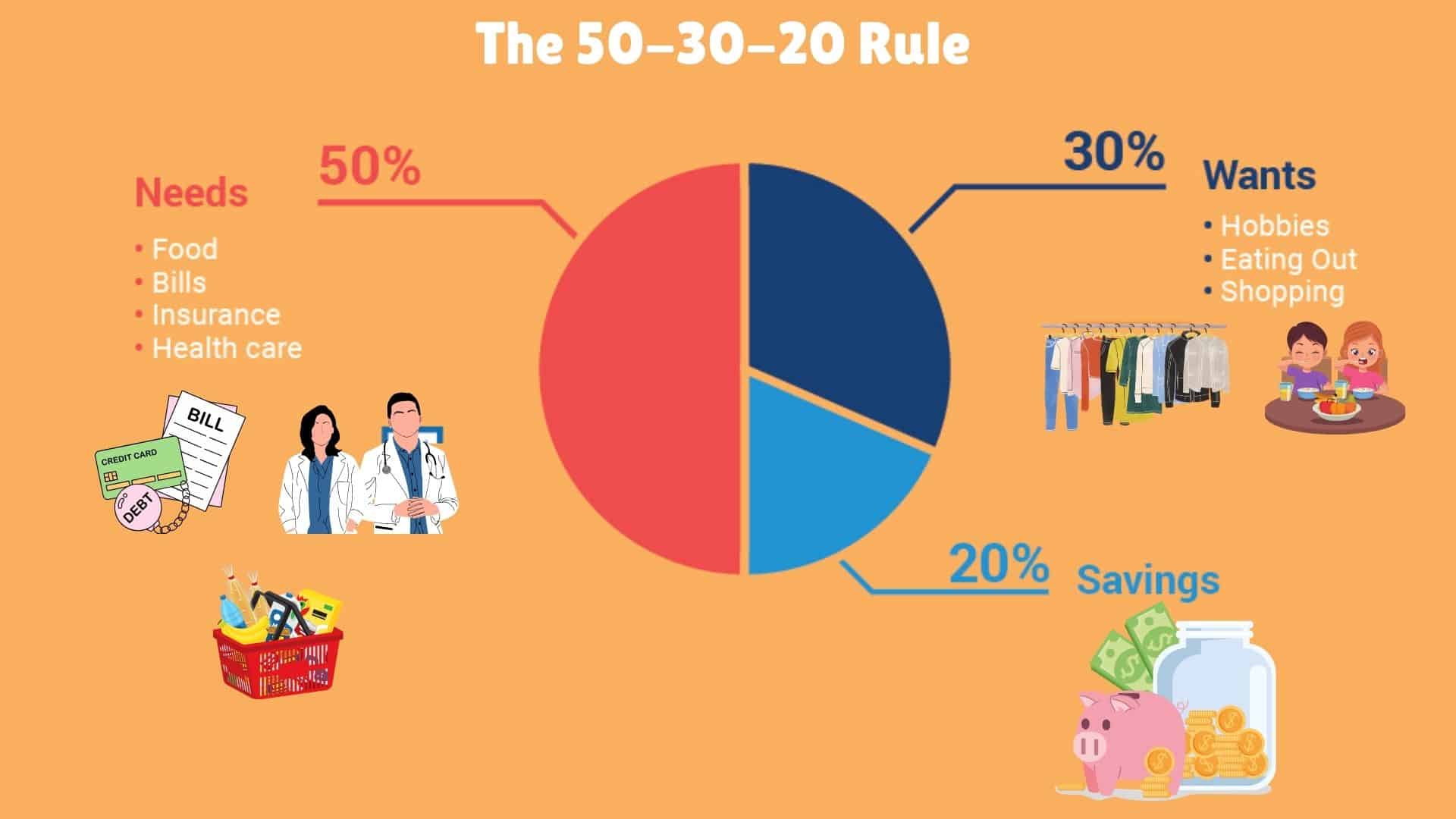

Not only do you have a budget, but you properly allocate your budget and stick to it. We like Mint for budgeting because it’s free and easy to use. To allocate your money, use the 50/30/20 method.

50% goes to essential expenses, 30% to discretionary expenses, and 20% to saving/investing. This budget process is simple and unfussy.

You Have an Emergency Fund

An emergency fund will ideally contain 3 to 9 months worth of essential expenses. Having an emergency fund can be the difference between a small, temporary setback on your financial road and a total disaster.

Saving enough money to fund nearly one year’s worth of expenses can seem daunting, and it can take a long time, but start by saving $1,000. A $1,000 “starter” emergency fund is an excellent step on the path to being a fiscally responsible person.

And the truth is, you may never have to dip into your emergency fund (that’s what we hope for) because, for most of us, a real financial emergency doesn’t happen all that often. If you seem to be having more than your fair share of financial crises, you may need to examine your life choices.

You Have Little to No “Bad” Debt

It’s not realistic for most of us to have no debt at all, at least not if we want to buy a house because most of us can’t afford to pay cash for such a large purchase. What you want to avoid is having bad, high-interest debt like credit card debt.

When your debt has an interest rate in the mid-teens and higher, it’s an anchor on all of your other financial goals. Once you have credit card or similar debt, it’s crucial to address it immediately. Start by creating a budget focused on repayment and explore options like consolidation or negotiating lower interest rates. Taking action now will help you regain financial control.

Use the snowball or stacking method to tackle one debt at a time. Concentrating your efforts will help you pay off the debt faster, which will save you money in interest charges. If your credit score is good enough, you can consider a loan with a company like Upgrade or Credible. Yes, you still have debt, but at a lower interest rate.

Your Credit Health:

- Understand your credit score

- Get Personalized Recommendations

- Get Regular updates

If you have student loan debt, it’s not bad debt if the interest rate is relatively low (and you have a degree). But if your rate is 5% or above, you might want to consider refinancing with Credible to get an even lower rate. You can shop for rates without impacting your credit score, and you’ll get offers in just a few minutes.

You’re Investing

Investing is the best way to grow your income. Most of us are not going to get rich from our jobs, but if you do it right, you can become rich through investing. How do you do it right? You invest early and regularly.

If you’re just starting out, These are the places to do it:

- Brokerage Account: If you want to buy stock in individual companies, you’ll need to open a brokerage account. You can do that with companies like Robinhood, Charles Schwab, or Fidelity. You need to do some research before buying stock in individual companies.

- Mutual Funds: You can buy a mutual fund directly from a mutual fund company like Dimensional Funds, BlackRock, or T. Rowe Price. They can also be purchased through some banks or brokerage firms.

ETFs: You can buy ETFs through companies like M1, Wealthfront, and Empower.

If your employer offers a 401k with matching, contribute at least enough to get the match. That match is free money. If you don’t have access to a 401k or the choices your employer offers aren’t great, you can open an IRA. These are retirement accounts and have tax advantages not offered by non-retirement investment vehicles.

You Have at Least One Form of Passive Income

Passive income is money you don’t have to do anything or very much to earn. Investing is a form of passive income. You regularly contribute money to an investment account, and the stock market takes care of the rest.

But there are so many other ways to make passive income that you should have at least one other. Our favorite form of passive income is real estate. If you’re ready to become a landlord, you can buy a

If you don’t want to be responsible for things like renovating the avocado green kitchen and replacing broken toilets, you can buy a turnkey rental property and hire a management company. Then all you have to do is sit back and collect that sweet, sweet rent check.

Take a look at LMM’s course, Rental Properties for Passive Investors.

Our proven, data-driven approach to building a portfolio of income-producing rental properties that perform in the long-term.

You can learn more about it here.

If you want to invest in real estate but aren’t interested in or can’t afford to buy a

Side Hustle

A side hustle is a little different than earning passive income. Making money with a side hustle usually takes a bit more work. But thanks to the internet, there are dozens of ways to do it, so everyone should be. Drive for Uber, rent out your place (or someone else’s!) on Airbnb, start a blog, or teach ESL.

Your side hustle might not earn you a ton of money (although it can) but even having a trickle of extra money coming in each month can go a long way to helping you become a fiscally responsible person and achieve your financial goals.

You Have Enough of the Right Insurance

Health insurance in America is notoriously expensive, but without it, you risk serious financial hardship. Even minimal coverage, like catastrophic insurance, can help protect you from medical bankruptcy. Ensuring you have some form of coverage is essential to safeguarding your financial future.

Most homeowners have homeowners insurance because their mortgage holder requires it, but too many renters forego having renters insurance. Renters insurance covers a lot more than just the stuff in your apartment (which your landlord’s insurance does not cover) and with Lemonade, you can find a policy for less than $30 per month.

The same goes for auto insurance. It’s required in nearly every state, so most people who drive have it. If you’ve had the same policy for a while, it might be time to shop around for a better deal.

Anyone with dependents needs life insurance. If you depend on a paycheck as most of us do, you need disability insurance. Those nearing 50 or who have a family history of chronic illness need long-term care insurance.

All of this sounds like a lot of legwork, but you can use Policygenius to get an insurance checkup and to shop around for better deals.

You Have an Estate Plan

Most of us know we need a will and we’ve heard of trusts, but we think trusts are something only rich people need. Not true! There are some essential differences between wills and trusts, and most people (and their families) will benefit from having a will and a trust. Trust&Will can provide the documents required for a complete trust-based estate Plan in about an hour and for a lot less than you imagine.

You Spend Well

I wanted to end on this one because being a fiscally responsible person doesn’t mean you hoard your money and only spend it on the bare necessities. Being fiscally responsible is not that different from being frugal. And frugal people aren’t afraid to spend money; those are cheap people.

Money can buy happiness if you know what to buy.

Frugal or fiscally responsible people just want to get the most for the money they spend. That means buying good quality items that will last and not have to be replaced after only a few uses.

And it means that they spend money on buying experiences rather than things. Because doing so has been proven to make you happier. And that’s what our money should do, help make us happy. So happy (fiscally responsible) spending!

Show Notes

1792 Ridgemont Reserve: Small batch Kentucky Bourbon.