Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

Got a few extra bucks in your pocket at the end of the month? Good for you, that’s half the battle, spending less than you make and plenty of people don’t. The other half is knowing what to do with those extra bucks. The decisions you make can for your discretionary income can be the difference between just doing okay and thriving financially.

If you want to thrive, you should be doing this with your discretionary income.

Call It What You Like

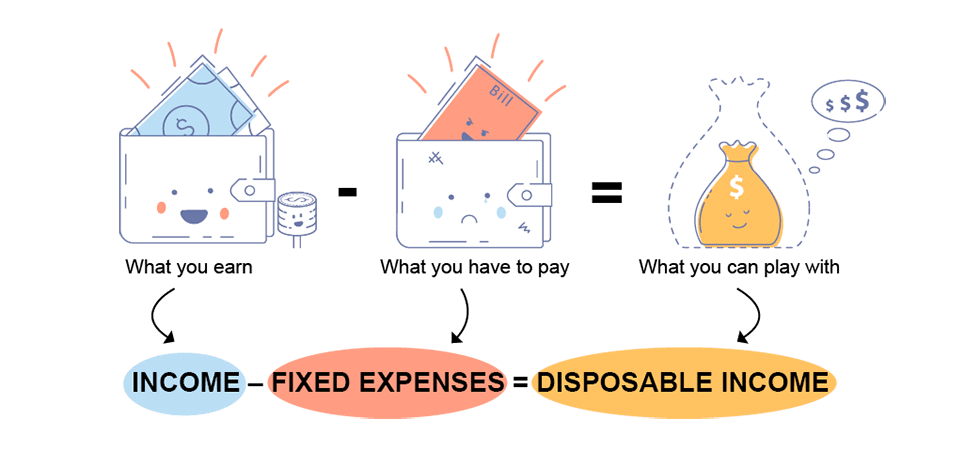

Discretionary income is also known as disposable, fun, and mad money. Whatever you call it, it’s the money left over after paying your mandatory expenses.

What you do with this money matters more than how much money it is. Those with a high disposable income may have much worse money habits than those with a low income. People with a propensity to save will grow their wealth no matter how much disposable personal income they have.

The problem is that what many people consider mandatory expenses really aren’t.

Mandatory expenses are things like housing costs, food, utilities, health care, and student loans. And even within those mandatory expense budget categories, there is often room to cut costs.

You could move to a cheaper apartment or get a roommate, reduce food expenses by batch cooking and eating leftovers, and lower student loan payments by refinancing.

So what about those expenses like dinners out, bar tabs, tech upgrades, manicures, and gym memberships?

Sorry, not mandatory.

That doesn’t mean you can’t spend your discretionary income on them or anything else you choose to spend it on but every additional dollar you spend on non-essentials is one less dollar you have to save and invest.

And those discretionary dollars are going to make up your wealth and your retirement income, so you have to use them well.

Calculating Your Discretionary Income

How much discretionary income do you have? It’s easy to get the number if you have a budget. There are a lot of budgeting systems out there, but Mint is our favorite because it’s free and easy to use.

Your gross income includes money from all sources including:

- Your salary

- Side hustle money

- Retirement income

- Social Security income

- Dividend earnings

- Rental income

- Child support

Factor out any taxes paid on these earnings to get your after-tax income number. This number is your disposable income.

Next, total all your necessary expenses like housing, utilities, food, etc. and subtract the number from your disposable income. The number you have is your discretionary income.

And you’re probably spending more of it than you realize. Americans spend $174.186 over their lifetime to “treat themselves.”

Anything that feels good couldn't possibly be bad.

Tweet ThisBroken down to monthly numbers, that is $199 a month which is about 22 percent of their disposable income. And while there is indeed nothing wrong with treating yourself occasionally, it can’t be your priority if you want to grow your wealth.

So precisely what should be your priority when it comes to your disposable income? We’re going to tell you.

Put it Away

One of the most important things you can do financially is to build and grow an emergency fund. Having an emergency fund can mean the difference between a small financial setback and complete financial ruin.

Ideally, an emergency fund contains six months’ worth of mandatory expenses and is kept in a safe place like a high-yield savings account. If you have high-interest debt, paying it off makes more sense than hoarding six months’ worth of money because debt costs so much in interest.

But even if you do have that kind of debt, you need a small emergency fund of $1,000.

Pay Off Debt

Not all debt is dire but high-interest debt, usually credit card debt, is an emergency and you must make paying it off your priority once you’ve saved $1,000 for your emergency fund.

But you want to spend the least amount of your take-home pay on that debt as possible. It’s the interest that makes debt expensive, and there are ways to lower your interest rates.

If you have credit card debt, you have a few options.

A consolidation loan from lender like Upgrade is the best solution. You borrow money and use it to pay off your credit cards.

Yes, you will still have debt, but the interest rate will be lower, often much lower, than the rate on credit cards.

You can call up each issuer and ask them to lower your interest rate. Tell them that you want to focus on paying off your cards so you don’t have to declare bankruptcy and if they agree to lower your rate, it will really help.

You use the bankruptcy line because the credit card companies know that they won’t get paid a dime if you declare it. Lowering your interest rate is a much more appealing option.

If you have student loan debt, it doesn’t have interest rates anywhere near what credit cards have but even lowering the rate by just 1 percent will save you money. You can lower that rate when you refinance your student loans.

Credible lets you window shop for the best student loan refinancing rates and terms.

Make it Grow

You’ve done the hard stuff, saved up an emergency fund and paid off or refinanced your debt. Now comes the fun part! Investing is easy, you can set it and forget it and watch your money grow with pretty much zero effort from you.

Now your priority for your discretionary income is retirement investing. Why? Because retirement accounts are tax-advantaged in a way that other investments are not.

Concentrate first on maxing out your 401k, especially if your employer offers to match. That match is free money. Contributing to your 401k lowers your taxable income, always a plus come income tax time.

Once your 401k is maxed, you can open an IRA, Roth or Traditional; both have their advantages.

Generally speaking, a Traditional IRA is the best choice if you expect to be in a lower tax bracket during retirement which is the case for most people. There are also income limits for Roth IRA’s, so if you’re a high-income earner, you’ll need to go Traditional as well.

If you have some discretionary income left over after fully funding your retirement accounts you can continue to invest with an M1 Finance account.

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.

Make Passive Income With Real Estate Investing

All of the money in your retirement and

If owning an entire house is a little more than you can deal with or afford, Fundrise is just what you’re looking for.

Fundrise gives individual investors access to commercial real estate via an eREIT.

Diversify into income-producing real estate without the dramatics of actual tenants. Fundrise eREITs are a diverse family of funds, each of which pursues a focused real estate investment strategy.

Disclosure: When you sign up with this link, we earn a commission. All opinions are our own. I am an investor with Fundrise.

If you do want to own an entire house but don’t want the everyday hassles of being a landlord, you’ll want to explore turnkey rental properties.

Andrew and Laura used this exact strategy to generate passive income which they detail in their course, Rental Properties for Passive Investors.

Our proven, data-driven approach to building a portfolio of income-producing rental properties that perform in the long-term.

You can learn more about it here.

Turnkey rental properties outsource many aspects of the process depending on the platform you use.

These could include finding the perfect house to finding the perfect tenants and everything else that goes into being a successful

You Should Live a Little!

Consumer spending is what drives the economy and Americans love to spend money. So if you feel a little guilty when you blow some of your discretionary income, don’t. You’re just doing your part to keep the economy going!

Consumer spending is what households buy to fulfill everyday needs. This private consumption includes both goods and services. Every one of us is a consumer. The things we buy every day create the demand that keeps companies profitable and hiring new workers.

But you only have so much discretionary income to blow, so you want to make sure you get those most out of that spending and don’t feel guilty about it. How can you do that? Use that money to buy yourself a little happiness.

And you can buy happiness when you spend money on experiences rather than things.

I recently spent some money to go to France. I could have spent that same money on lots of things that I also enjoy like new clothes, books, and more shelves to hold those books.

But that trip gave me things that buying stuff just can’t, anticipation, excitement, a break from my regular life (which is already pretty awesome), shared experiences since I traveled with a close friend, the chance to see new places, try new things, make new friends, and memories. Those are things I will have forever which is more than I can say for most of the stuff I buy.

You see, money can buy happiness if you know how to spend it. Don’t waste precious, hard-earned discretionary income on crap you don’t need.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Use Your Discretion

We can all spend our money on anything we want, of course, nothing is stopping you from taking your entire paycheck to the roulette wheel. That’s why it helps to see your money, not as a lump sum but as a few small piles of money that must be appropriately allocated.

When you separate the money you must spend from the money you can spend, it puts your finances in sharper focus. You can’t take that whole $1,000 to the roulette wheel, but you can take $20, put it on black and let it ride. If that’s what you’re into. Use your discretion.