Americans love a good deal. And a bad deal. And no deal. What we mean is that Americans love spending money. Even more so than baseball, spending money is our national pastime. How do you stop spending money when it’s part of your heritage?!

We even do something called “drunk spending!.”

A survey found that 26 percent of Americans — about 53.4 million people — admit to shopping while under the influence of alcohol and collectively, Americans spent $39.4 billion on drunk purchases in the past 12 months, an increase from last year’s $30.43 billion. That means the average American drunk-shopper spent $736 while intoxicated over the last year.

What are we buying in our drunken state? You name it. Everything from food (fair enough) to vacations, to pets, to art (for the classy wine drunks), to cars! And if our credit card debt is anything to go by, our sober purchases aren’t much better. The average American is in credit card debt to the tune of $4,293, and it totals more than one trillion with a T dollars.

At the same time, 40% of us can’t come up with $400 in the case of an unexpected emergency expense. So a lot of us don’t have an emergency fund nevermind any investment accounts or retirement savings. What we do have is a spending problem. We can’t seem to control our spending habits and stop overspending, and we’re often left with nothing at the end of the month.

This has to stop. In fact, the buck stops here. If you want to know how to stop spending money and start saving money, you came to the right place.

How to Stop Spending Money

Our bad money habits weren’t created overnight, and they can’t be solved overnight. Training yourself how to stop spending money takes some degree of willpower, but willpower is a fleeting thing. It comes and goes, waxes and wanes. Discipline is a better way to control spending, but discipline is like a muscle, it takes some time to build it up.

But your overspending is an emergency, so we don’t have that kind of time. While we encourage you to flex your willpower and build discipline, we’re also going to show you some cheap and dirty ways to help control your bad habits around money. Hacks if you will. But you won’t because that word is mega played out and y’all hate it.

Find the Root of the Problem

When do you make impulse buys? When you’re drunk (some of you do, the stats in the top of the article prove it)? Maybe when you’re angry, frustrated, sad, happy? Think back to the last ten things you bought that you didn’t need. If you can remember that many.

Often when we make impulse buys, what we spend money on aren’t things we even want by the time we make it home from the store. So we stick it in a closet somewhere and will toss it out eventually, unused when the spirit of Marie Kondo possesses us.

Note how you felt when you bought those things. Now ask yourself if those purchases made you feel better for longer than a few minutes. We won’t ask if what you purchased solved the anger or frustration or sadness. You already know that it did not, and it never does. So why do you keep doing it?

I don’t know. Who am I, Freud? You can do some soul searching or find a therapist to aid you in figuring it out if you think that would be helpful. But for our purpose, which is to get you to stop spending money, it doesn’t matter. It only matters that you recognize what emotions lead you to spend money on non-essential stuff that you don’t want, don’t need, and can ill afford.

When you identify that emotion, write out a list of things you can do to soothe yourself that don’t require you to spend money. Go for a walk, call a friend, clean out a closet, cook a meal, something that will distract you. However, don’t eat or drink adult beverages. Substituting one bad habit for another is not the goal here.

Set Up a Budget

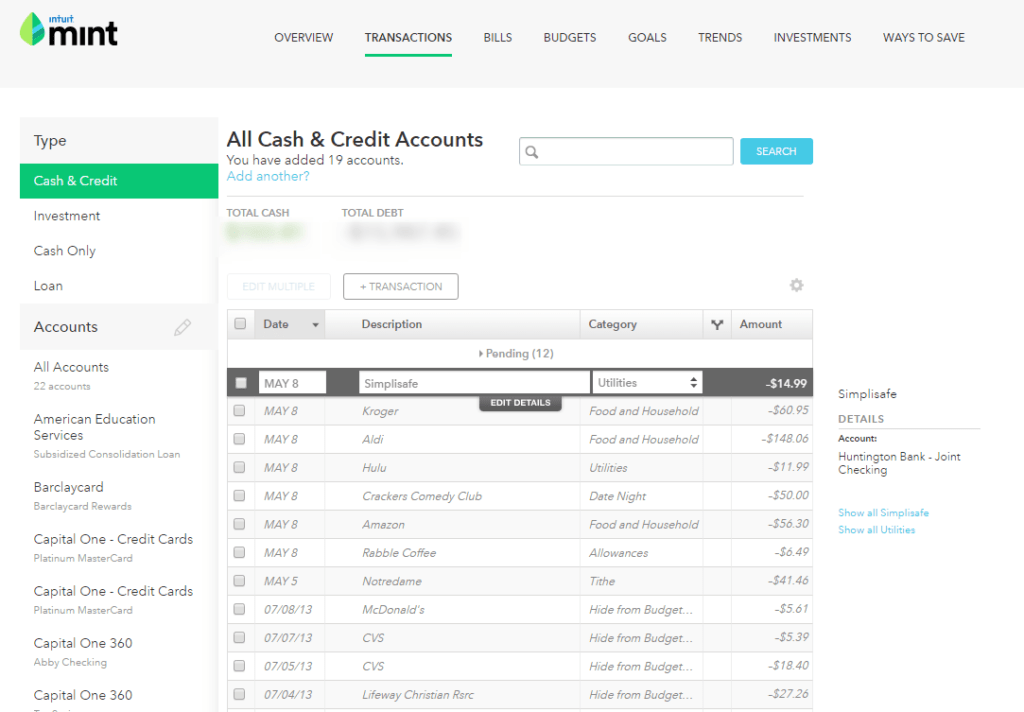

This step is going to suck. Not because creating a budget is hard. It isn’t. Mint makes it very easy and is free to use. What’s going to suck is being confronted with just how much you’re spending and on what. Connect your checking account and credit card accounts to Mint and go through a month or two of transactions. Eye-opening isn’t it? You’re almost certainly spending a lot of money that you didn’t even realize you were spending.

Now use the 50/30/20 method to create a budget. What gets measured gets managed, and you can’t stop wasting and start saving if you don’t know where your money is going. Mint isn’t a magic wand though. You can create a budget in Mint or any other budgeting program, but they can’t prevent you from going over your budget. We’re getting to that. But creating a budget is personal finance 101. Everyone needs one, not just those who can’t stop overspending.

Use Cash

I don’t prefer using cash or even debit cards over credit cards. Credit cards give you certain protections that you don’t have when you spend cash or use a debit card. But if you’re serious about how to stop spending money, cash is king.

Swiping a debit or credit card doesn’t feel like you’re spending money, in the same way, pulling out cash does. Cash seems more tangible and can make you more aware of how much you’re spending. Cash is also finite in a way that debit and credit cards aren’t. Once you spend all of the cash in your wallet, you’re done spending. And taking out cash is a pain. If you can’t find an in-network ATM, you have to pay a fee to access your own money. And at LMM, we always avoid fees!

So take out the amount of cash you’ve budgeted for the week and leave your cards at home. Is this foolproof? No, you can always retrieve your cards and spend more, but spending only cash really can help you to make better spending decisions.

Delete, Delete, Delete!

The internet has made life so convenient. You can use Uber Eats to have food delivered right to your door, you can buy almost literally anything on Amazon and a million other sites without putting on clothes, you can see what purse some shill on Instagram is hawking and order the same one right from her post.

If all of this sounds familiar, a big part of our collective impulse buying problem can be linked back to online shopping, be it for food or expensive purses. So the first step is to remove your saved credit or debit card account details out of any and all sites you use to buy stuff online. Having that information so close to one of the sources of your overspending is just too dangerous.

The next is to delete apps and block sites through which you buy non-essential items. Does this mean you have to delete Uber Eats and Amazon? Not necessarily. We all work a lot, and sometimes we don’t have the energy to cook dinner. If this is a chronic problem, there are better solutions than ordering out (get a slow cooker!), but the odd food delivery won’t put you into the poor house.

And if you use Amazon to bulk order staples like cleaning products, personal care items, and pantry items, that can be an excellent way to save money as Amazon can be cheaper than buying them in the grocery store or pharmacy. But be honest with yourself. You know where your problems are.

No is a Complete Sentence

Someone is always asking us to spend money. Sometimes it’s for fun stuff that we want to do like going out to dinner with a friend. Sometimes it’s for not so fun stuff like sponsoring a co-worker you barely know who is doing some kind of charity walk or selling some nasty chocolate for their kid’s school fundraiser.

But if you have a spending problem, you have to learn to say no. And by saying no, I mean say the word and then stop talking. You don’t have to explain your no. It’s no one’s business that you’re trying to save money because you’re trying to pay off your credit card balances or trying to build the discipline that will lead to better spending decisions.

Your no doesn’t have to be rude, but you don’t owe anyone an explanation. No means no, and no is a complete sentence.

Have Fun for Free

Saying no too often to friends who invite you out can lead to receiving fewer and fewer invitations until one day they just…stop. Yes, you’re trying to learn how to stop spending money, but that doesn’t mean you can’t have fun.

Our idea of fun is often doing something that requires money like going out to dinner or for drinks, but it doesn’t have to be that way. Create a mental list of fun things to do that are free or at least, don’t cost a lot. We’ve covered this from free date ideas to free ways to spend a Saturday night.

If a friend proposes an outing you can’t afford, offer an alternative. They may not always agree, but at least they won’t think you’re trying to avoid them. If this person is a financial friend, you won’t feel awkward about explaining why you proposed an alternative to their suggestion and they may be happy to save money too.

Have a Reason

List some of your financial goals; becoming debt-free, stockpiling an emergency fund in your savings account, saving for a home. It’s hard to deny yourself, so you need a reason for doing it. And track your progress. Seeing those credit card balances dwindle is motivating. Watching your emergency fund grow is motivating. Daydreaming about the newly renovated kitchens you see on Zillow is motivating.

No, motivating isn’t enough alone, but in weaker moments it’s good to be reminded of what you’re working towards.

Use the 30-Day List

A 30-day list won’t work for things like groceries because you need groceries and you need them more often than 30 days from now. But using a 30-day list will help curb impulse buys. The idea is to write down any non-essential purchase you want to make and wait for 30-days. If 30 days pass and you still want the item, then it’s likely something you really need or want and not an impulse buy.

But you’ll find more often than not that you forget about that thing way before the 30 days is up, and when you see the list weeks later, you’ll wonder why you ever thought you wanted it.

If you want to supercharge the power of the 30-day list, take the amount of money the thing you want costs and transfer it from your checking account to your savings account. Watching that balance grow helps grow that discipline muscle. Very rewarding!

Digging Out

The great thing about learning how to stop spending and finding success is the second you stop spending; you can start digging out of your hole. For some of you, that means paying off credit card debt, for some of you, saving and investing. As soon as you stop, you can start.

Debt

Most of the time when we talk about debt at LMM, we’re talking about credit card debt. Why? Because it’s pretty much the worst kind of debt you can have due to the high-interest rate. Being debt-free is ideal, but typically, student loan, mortgage, and car debt are more manageable.

There are several ways to tackle credit card debt. The best is a balance transfer credit card. The card will give you a period of time where the balance is not subject to interest. Every penny you pay goes to the principal which allows you to pay it off more quickly.

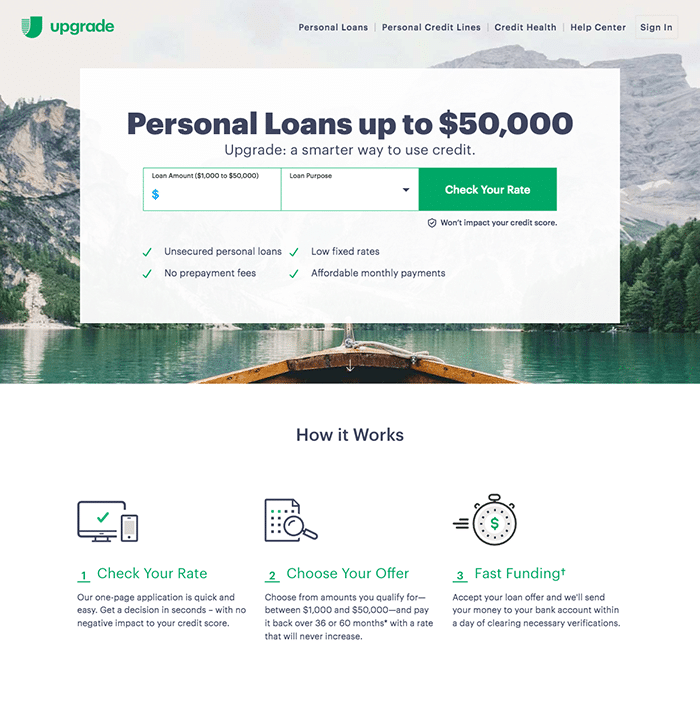

If you’re not eligible for a balance transfer card, you can apply for a personal loan from Upgrade. You’ll still have debt, but if your credit score is high enough, the interest rate will be lower than the rate on the credit cards.

Tally is a new app that gives qualified users a revolving line of credit to pay off credit card debt and helps manage payments using the stacking method to pay off the highest interest cards first which saves money on interest.

If none of those are options, you can use the snowball or stacking method to pay off your cards.

Emergency Fund

An emergency fund is money set aside for well, an emergency. Ideally, the fund contains 3 to 9 months worth of bare-bones expenses. If you have a car or home repair or suffer a job loss, an emergency fund can save the day.

Not only does it cover whatever emergency has befallen you, but it gives you peace of mind. If you’ve had a spending problem, you know how stressful it is to live paycheck-to-paycheck. When you have an emergency fund, you never have to live with that dread again.

Investing

When you start investing, you will see how much damage your spending problem has done. You see how that balance grows seemingly like magic. You’re not doing anything at all, but you have more and more money!

That’s the power of compounding interest and the magic ingredient in compounding interest is time. It’s disheartening to think about how much time you wasted and how much money you left on the table because it took you so long to learn how to stop spending money.

The best time to invest was 20 years ago. The second best time is now.

Tweet ThisThat’s okay. It happens to lots of us. There’s no use crying over spilled beer (some of you will beg to differ), but you do need to start getting serious about investing to make up for as much time as you can.

In less time than it took you to read up to this point, you can go to

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Don’t Become Complacent

Those who have addictions never consider themselves to be “cured.” They have better habits now and better ways to cope with whatever drove them to their addictions. But those who are successful in their recovery are always vigilant. They know they could slip up and fall back into their addiction.

By making the life-affirming transition from addicted to recovered, we gain a recovery “toolbox” that helps us navigate life’s challenges and stresses in a much healthier way. We learn to connect with people, push our egos aside, and to ask for help if we need it. Thus, when faced with stressful situations that formerly would trigger our addictions, we might respond by exercising or calling a friend. As such, we substitute addictions with healthier activities that perform the function that the addiction used to, albeit in a much more fulfilling way.

If your problem was spending, you have to watch out that those old, bad habits aren’t allowed to creep back in. Because for some of us, learning how to stop spending money is a life-long lesson.

Show Notes

Mint: LMM’s budgeting for dummies.

Magic Hat Elder Betty: A great summer beer.