Death and taxes. I thought about the most depressing way to start this article, and mentioning those two inevitabilities was it. Okay, not really, but keeping them in mind is extremely important when thinking about tax-efficient retirement withdrawal strategies (and how to make your retirement savings last).

The time to start thinking about how your retirement withdrawals will be taxed should be way before you retire.

Planning your sources of income in retirement based on taxation is just as important as planning how to spend it.

The key strategy of tax-efficiency involves using tax brackets to your advantage. It requires you to think about many things.

This post details what you should consider.

Sources of Income

Withdrawing retirement funds usually involves investment income from tax-deferred or tax-free money, but any income affects it.

For a deep dive into optimizing your income tax treatment, read Tom Wheelwright’s book, Tax-Free Wealth.

In general, you can have three types of retirement income.

Fully Taxable

Some sources of retirement funds are fully taxable. That means every penny that you get from specific accounts or income is eligible to be taxed.

If you’re still working, your income is fully taxable, just like before retirement. It’s potentially a reality for many who are of retirement age but may not have enough saved.

Many plan to work at least part-time in their retirement years.

Pensions are generally fully taxable since they’re usually funded by employers pre-tax.

However, some states don’t tax pension benefits. Rental income is also taxable with the usual deductions you can take for expenses and associated costs.

Finally, funds from traditional retirement plans such as traditional IRAs, 401ks, 403bs, and similar pre-tax retirement accounts are fully taxable.

It means any distribution you take from these accounts is eligible to be taxed. It’s not just the gains like in a taxable brokerage account.

Keep In Mind

Periodic income is taxable. It includes interest payments from bonds, ordinary dividends from stock, or interest from savings accounts.

This is important to keep in mind when trying to stay within specific tax brackets. They’re sometimes easy to forget.

Partially Taxable

Some potential sources of retirement funds are only partially taxable. It means that only gains or interest can be taxed or counted toward taxable income.

That becomes important later when we start talking about using the tax brackets to our advantage.

With most assets you buy in a taxable account, such as in a brokerage account or a regular non-retirement account mutual fund, only the gains are taxed.

This comes in the form of capital gains taxes. When you sell these assets, the amount you originally spent on them is not taxed.

If you hold the assets long enough, even the gains carry a lower tax rate.

Interest on savings accounts and bonds in taxable accounts are taxed at regular income tax rates, but again, the principal is not.

Thus, if you were to sell a bond, the amount you originally paid for the bond is not taxable.

Lastly, did you know that a maximum of 85% of your Social Security benefit is taxable? And, depending on your income tax bracket, it may not be taxable at all.

Non-Taxable

Finally, there are potential sources of retirement funds that are entirely tax-exempt. The most well-known are Roth accounts.

They’re funded with post-tax money, and if you’re at least 59 ½ years old and have had the account funded for at least five years, you will owe nothing to the IRS when you take distributions.

Life insurance proceeds and inheritances are also not taxable. However, if the deceased lived in one of six greedy states, some inheritances are subject to taxation.

Although we won’t discuss it here, Health Savings Account (HSA) distributions for qualified medical expenses are also not taxable.

It comes into play for a strategy involving saving up all your medical receipts from the day you start an HSA account and reimbursing years after-the-fact.

Taxation of Retirement Income

| Fully Taxable | Partially Taxable | Not Taxable | |

|---|---|---|---|

| Retirement Accounts | Traditional IRAs, 401(k)s, 403(b)s, 457s, SIMPLE plans, SEP plans | Non-deductible IRAs | Roth IRAs, Roth 401(k)s, Roth 403(b)s, Roth 457s |

| Fixed Income | Pensions | Social Security | Interest on Municipal Bonds |

| Investments | Assets in Taxable Accounts, Savings | ||

| Other | Employment Income, Rental Income | Appreciated Physical Assets | Death Benefit from Life Insurance, Inheritances, HSA Reimbursements |

When or If You Retire

The age at which you decide to retire is just as important as where you have your money when you retire. You have to determine when to stop collecting a paycheck or when to start collecting Social Security.

You also have that RMD deadline lurking.

Continuing to Work

Considering so many people have little saved for retirement, there will be many who will continue working into their golden years or at least work part-time to supplement their income.

This working income can push you into higher tax brackets.

Quick Tip

If you choose to claim Social Security benefits before full retirement age and continue to work, they may be reduced based on your income.

After you reach full retirement age for Social Security, your income from working has no impact on your benefit.

However, it still matters in determining your tax bracket.

When to Collect Social Security

Most people know you can collect it early and get a reduced amount in the future or delay taking it to get a more considerable amount.

This decision is all about what your life expectancy is. The longer you think you’re going to live, the better it is to delay starting benefits.

However, when thinking about taxes in retirement, your income from Social Security will also matter.

Worth Noting

Since at least 15% (and potentially all) of your Social Security benefit will never be taxed, it could be a lower-taxed source of income if you decide to take it early.

It could also help offset the taxes you have to pay on large RMDs.

If the bulk of your retirement funds are from traditional IRAs, you could delay taking Social Security, of which only up to 85% of it will be taxed, and have a larger benefit check taxed at a lower rate than your RMDs.

What are RMD’s? Glad you asked.

Required Minimum Distributions

At 72 years of age, Required Minimum Distributions (RMDs) for traditional, SIMPLE, or SEP IRAs kick in.

It means you must take a certain percentage distribution from your IRAs and pay the associated taxes.

If you don’t, there is a hefty 50% penalty on the amounts you don’t take. The tax impact on your withdrawal strategy will be significant if you have a lot of funds in these accounts.

If you retire before you turn 72, you may be able to minimize the impact of RMDs later if you convert your traditional IRAs to Roth IRAs (which do not have RMDs).

You can do this when you are in a lower tax bracket since you have to pay income taxes on the conversion.

Keep in mind this is because the conversion is considered a distribution from your traditional accounts, and you will move up in your tax bracket accordingly.

You also have to take RMDs on Roth 401(k)s. However, it doesn’t count toward taxable income and you will owe no income tax.

Remember that your medicare monthly premium may be higher if you reach certain income levels as a result of these conversions in a given year. It’s all a juggling act.

If you’re a warrior and work past the age of 72, you can avoid RMDs and their associated taxes if you funnel all your traditional retirement accounts into your then employer’s 401(k).

401(k)s don’t impose RMDs while you’re still working. Granted your employer has to allow reverse rollovers from IRAs to their 401(k).

How Age Affects Your Retirement Income

| Age | Significance |

|---|---|

| 50 | Catch-up contributions can be made to certain retirement plans |

| 59 1/2 | Withdrawals allowed from 401(k)s and IRAs |

| 62 | Earliest age to collect Social Security (at a reduced rate) |

| 66/67 | Depending on birth year, full retirement age for Social Security |

| 70 | Maximum Social Security benefit if waited until this age to collect. |

| 72 | Required Minimum Distributions from traditional retirement plans start |

Fiscal flexibility that’s funny, free and delivered weekly.

How Much You Will Have

As mentioned previously, another factor determining your retirement withdrawal strategy is how much you will have to draw from.

It’s more than just counting on a certain amount to last the rest of your life. As someone once notoriously said, “More money, more problems.”

I don’t know if he was talking about taxes in retirement, but it applies.

If your only source of income in retirement will be Social Security, taxes won’t be an issue.

Your Social Security benefits are only taxed after you exceed a certain amount of income from other sources.

However, if you have multiple streams of income from various taxable sources, you will have to strategize how to take those distributions smartly to maximize the amount you keep.

For example, if you have a large chunk of money in traditional IRAs, after 72 years of age, due to RMDs there is likely going to be a baseline amount of money you will have to pay taxes on that you can’t avoid.

Possible Tax Law Changes

Lastly, Congress could throw everything out of whack by changing the tax laws. Think of how tax laws have changed in the last twenty years.

All signs point to just as many or even more drastic changes in the future. Could we go to a flat tax? Could we join our European friends and institute a Value-Added tax system?

If you’re putting all your eggs in the Roth basket because you do not want to pay any taxes in retirement, there’s no guarantee that’s a smart move.

If they institute a federal sales tax at 33% and let federal income taxes go away, your Roth does you no good, and people with traditional IRAs will brag about it forever.

In this case, it’s best to prepare yourself for any crazy idea those folks on Capitol Hill come up with.

Optimized Strategy

Diversify the tax-treatment of your retirement funds by holding various account types. This way, you have lots of weapons in your tax-fighting arsenal when the time comes.

Tax Brackets

All the above considerations factor into using the tax brackets to your advantage when it comes time to take distributions from and liquidate your nest egg.

Not every dollar in your retirement savings will be taxed at the same rate which creates opportunities to decrease your overall tax burden.

Additionally, having less taxable income could also allow you to pay lower Medicare premiums and lower Social Security tax rates.

How Tax Brackets Work

You often hear people saying things like, “that will put me in a higher tax bracket” and conclude it’s a bad thing.

Some assume that being in a “higher tax bracket” means all of your money will be taxed higher. It’s the single most common misconception about tax brackets.

Moving to a higher bracket means you’re making more money. All the money below the higher bracket is taxed at the same rate as it was before.

Only the amount you’re making above the threshold is taxed at the new, higher rate.

When someone starts talking about tax brackets, you have to prepare for some math and odd percentages.

While you can’t talk about this and completely avoid math, I’ll at least try to make the math easier to follow.

Fictional Tax Brackets

For illustration purposes, and to avoid dating this article in a couple of years, I’ll use the following fictional tax bracket structure.

| Marginal Tax Rate | Income Level |

|---|---|

| 0% | On First $10k |

| 10% | Between $10k and $30k |

| 20% | Between $30k and $50k |

| 25% | Between $50k and $100k |

| 30% | Everything over $100k |

While there is no such thing as a literal 0% tax bracket, incorporating a standard deduction creates one, since anyone is eligible for it. So there will always be some amount of money that won’t be taxed.

Let’s say you have an income of $35k, putting you in the 20% marginal tax bracket.

Tax Bracket Math

There are no taxes on the first $10k = $0 taxes

You will pay 10% taxes on every dollar between $10k and $30k (10% of $20k) = $2000

You will pay 20% taxes on each dollar between $30k and $50k (20% of $5k) = $1000

This means you have a total tax burden of ($0 + $2000 + $1000) = $3000

$3000 of $35k is about 8.6% overall. This is your effective tax rate in this scenario.

So while you’re in the marginal tax bracket of 20%, most of your income is taxed at a lower rate.

Staying in Lower Tax Brackets

As you can see, a big chunk of those taxes come from the relatively small amount you make in your highest tax bracket.

While it’s not worth giving up $5k of income to save $1k in taxes, you can see how you’d want to avoid moving to higher tax brackets.

However, another way to look at it is that you have some room in your tax bracket before any additional income is taxed at an even higher rate.

In the above case, you could make another $15k (bringing you up to $50k) before any income is taxed at the 25% rate.

Using this wiggle room within tax brackets is the key to having an effective tax strategy for your retirement savings.

Working the Brackets

There are several strategies for using the tax brackets to your favor in retirement. It involves drawing from diverse sources that are taxed differently.

It would help if you also consider your income needs in subsequent years. Lastly, converting the tax treatment of your income sources also plays a role.

Have Diverse Income Sources

Previously, we spoke about how you can have three types of income when it comes to tax treatment in retirement.

Having these different accounts and other sources to draw from makes working the tax brackets easier.

Diversification in the tax treatment of your retirement funds is just as important as asset class diversification.

If you need to draw from fully taxable sources of income, you want to do so in low tax brackets.

The ideal situation would be to withdraw fully taxable income only in the 0% tax bracket.

You probably thought your only source of non-taxable income would be from your Roth IRA accounts.

Think On This

In reality, if you withdraw from your traditional accounts while in the 0% tax bracket, you won’t be taxed.

It’s why even if a majority of your retirement income will come from non-taxable Roth accounts, it’s good to have something in traditional accounts.

You could have a source of income that was pre-tax when you funded and not taxed when you withdraw (or at least at a very low rate).

Once you start approaching the top end of whatever marginal tax bracket you’d like to stay in, you’ll need those partially taxable income sources to give you more capital while slowing your ascent in your current tax bracket.

Lastly, it would be helpful to tap into your non-taxable sources of income to keep you from going into the next tax bracket. Roth accounts are your secret weapon in this tax war.

No matter how much you draw from them, it will have no adverse effect on your tax situation.

Diversification in the tax treatment of your retirement funds is just as important as asset class diversification.

Tweet ThisThink About The Following Years

In an ideal tax circumstance, you need exactly a dollar less than the top amount in your marginal tax bracket in any given year.

That way none of your money is taxed at the next tier up. But what if you don’t need that much money?

It may be worth it to think about your possible income needs for subsequent years.

Perhaps you’re planning a long trip around the world or making a big purchase like an RV. If you make a large withdrawal that year, it might push you into a very high tax bracket.

To soften the future tax blow, you can withdraw enough money in the current year to take you to the top of your current tax bracket, pay the (lower) taxes on it, and keep it in savings until you need to make that big purchase later.

Convert to Roths When Advantageous

Suppose you have enough in fully taxable accounts (like traditional IRAs) where you know those withdrawals will be in future higher brackets.

In that case, executing a Roth conversion may be a good idea while you’re in a lower tax bracket.

Perhaps you decided to delay collecting Social Security for the larger payout. Or maybe you want to wait until 72 to take traditional IRA distributions.

You might have a pile of cash or sudden inheritance that you can live on for a while.

You could also decide to live on selling assets in taxable accounts where the long-term gains are only taxed at 15% or less.

Whatever the reason, in a given year you may have little to no taxable income. This is a great time to convert some of your traditional retirement account funds to a Roth.

You will pay little to no taxes on the conversion. Later you will have a larger pool of non-taxable, non-RMD funds to draw from.

Long Term Capital Gains

Long-term capital gains have their own set of tax brackets. Up to a certain ordinary income (currently at $40k for single filers), you will pay a 0% long-term capital gains rate.

At higher tiers, you’ll still pay lower tax rates than your marginal tax rate.

Did You Know?

Long-term capital gains are the amount of profit on taxable assets you own for more than a year.

So if you have a lot of taxable assets, you could consider a strategy where you’ll only pay capital gains taxes on them by keeping your ordinary taxable income to a minimum.

Theoretically, if you can live on less than $40k a year (not including deductions) and your income is from selling taxable assets, you will have no taxable income.

Another quirk about long-term capital gains is that they are taxed separately from regular income. This means that if you realize long-term capital gains, it does not push you higher in the tax brackets.

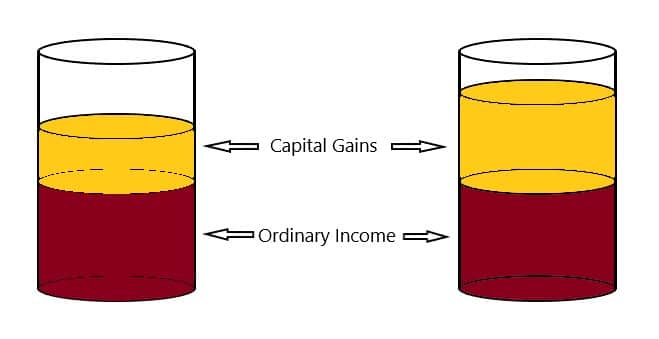

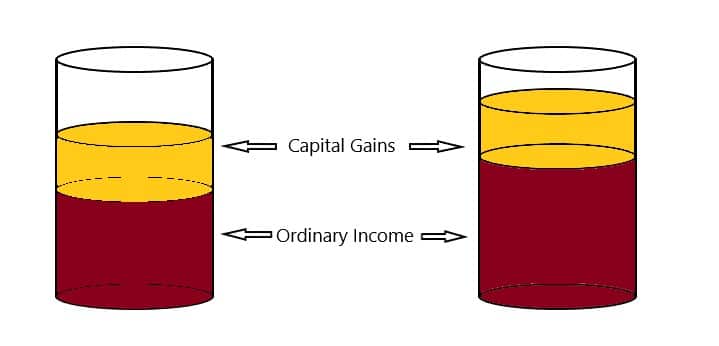

If you need help conceptualizing this, think of your income as a jar of settled oil and vinegar.

Vinegar will always sink to the bottom and oil will rest on top. Vinegar is your ordinary taxable income and oil is your long-term capital gains.

No matter how much long-term capital gains (oil) you dump into that jar, your ordinary taxable income (vinegar) will always remain at the same level.

You may rise in the long-term capital gains tax rates, but they are generally lower than ordinary income rates.

But an increase of regular taxable income (vinegar) not only raises you in the tax bracket, but it can also push those long-term capital gains (oil) into higher long-term capital gains tax rates.

Social Security’s Effect on Tax Brackets

Generally, the lower your marginal tax bracket, the less your Social Security benefits will count toward your taxable income.

Plus, no matter your income, your benefits will never count toward taxable income at a rate greater than 85%.

How Do I Manage My Retirement Withdrawals?

Knowing all the concepts above, you have the ammunition to create an effective plan for tax-efficient retirement plan withdrawals.

If you prepare well, you will have a multitude of options when you’re ready to retire.

A Sample Plan If You Have A Lot

A good problem to have is holding enough sources of income where you have to optimize your tax treatment.

You worked hard to save money so you may as well try to keep more of it.

A big decision that’s going to affect your plan is when to take Social Security. It will not only affect your cash flow but also your tax brackets, so choose wisely.

And whether you take it early or later, regardless of the rate, you’re not going to refuse it to save some of it on taxes.

Next, you’ll want to at least fill up your 0% tax bracket with fully-taxable income. If you plan to live on more than modest means, consider using it for your lower tax brackets.

Alternatively, if you have a lot of taxable assets, like stocks in a brokerage account, you can use the 0% long-term capital gains bracket as your limitation.

Regardless, if you find yourself needing more money than what’s in the lower brackets, you can start tapping your partially-taxable sources to slow your ascent into even higher brackets.

You could take long-term capital gains, which, as mentioned previously, will not move you higher in your tax bracket.

But being in a higher bracket might mean your long-term capital gains tax rate will be higher.

Once you find a comfortable income level, start thinking about filling up the rest of your marginal tax bracket with Roth conversions.

Also, consider fully-taxable withdrawals to have on-hand as something more liquid such as cash or savings for a rainy day or blow-out year.

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.

A More Modest Plan

If you won’t have a lot saved by retirement, it’s even more important to keep taxes at an absolute minimum.

Your first option is to work as long as you can. It will do a few good things besides providing a source of income by the sweat of your brow.

You can forgo collecting Social Security a little while longer, increasing your monthly benefit later.

It will also allow you to continue to save more and get more employer match in your 401(k) at the same time. And, you’re not draining your retirement accounts if you’re not taking distributions.

You could even collect Social Security as soon as you’re eligible while still working. Granted, you’ll get less, and more of it will be taxed, but it will never be fully-taxed like regular income.

Helpful Tip

If you know you’re going to be living on less in retirement than your pre-retirement salary, put your retirement contributions into traditional IRAs or traditional 401(k)s.

Since you’ll likely be in a lower tax bracket in retirement, you’re essentially getting a discount on future taxes by taking the deduction now.

Once you retire, definitely start collecting Social Security; it’s your base. Again, it’s taxed less than other income sources.

Then use your fully-taxable retirement accounts for the lower brackets.

It would be best if you still planned for more expensive years. You can still convert some funds to a Roth as a precaution for tax law changes or drastic modifications to future tax brackets.

However, RMDs will likely not be a huge factor for you.

Conclusion

It’s not only about saving as much as you can. It’s about having a flexible and agile plan to deal with anything that may happen.

Everyone’s tax and income situation will be different, so there is no single right way to do it.

Believe it or not, this lengthy article only scratches the surface of how you can use tax-efficient retirement withdrawal strategies.

The concepts here only point you to more research on the methods described. It’s helpful to know the factors of how your money is taxed in retirement.

Again, all this could change with the banging of a legislator’s gavel. So, try to keep up with any tax law changes in the future.

Good retirement planning requires good tax planning.