Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

Financial independence is achievable, but you have to follow the steps to get there. These are the six steps to get you on track toward financial independence.

What Does Financial Independence Mean?

Becoming financially independent means the end of mandatory work and semi-early retirement. Instead, it’s being able to do whatever you want without worrying about money. Like Mr. Money Mustache!

It isn’t the same thing as retirement, which is the end of your working life (although as people retire younger and live longer, the definition is changing).

Don’t like your new boss, who is impossible to work with? Just quit.

Do you want to go back to school to become a teacher? Enroll!

Do you want to spend a year traveling the world? Pack your bags!

Do you want to start your own business? Then, start writing up a business plan!

You can’t get there overnight. Achieving financial freedom takes proper planning and discipline to stick to the plan, even if things are sometimes harsh.

It also means a lot of sacrifices. Your friends are taking exotic vacations, buying brand-new cars, and buying big houses with swimming pools and outdoor kitchens.

Don't give up what you want most for what you want now.

Tweet ThisYou’re staycationing. You drive a ten-year-old Toyota. You’re still living in the same apartment you’ve been in since you moved out of your college apartment.

You keep your annual spending low. You have a savings goal. But all of the sacrificing is front-loaded.

When you get to the sixth and final step on this list, you will be free while all of those people you’ve spent years envying are chained in place by credit card debt, car loans, and a huge mortgage.

You in? Good, let’s start right now. Here are six steps toward financial independence that you can follow to reach the freedom you’ve always wanted.

Step 1 – Get Control of Your Money

Getting control of your money is simple; spend less than you earn.

Budget

What are your monthly expenses? Some of us bury our heads in the sand regarding our spending. Facing it can be scary, but you must. Next, you can set up a budget. A good rule of thumb is the 50/30/20 method to allocate your money. This will work well for most people, but remember, we’re trying to achieve financial independence here!

The more money you can save, the better. This allocation doesn’t mean you must spend 50% on essentials. And if you have debt, swap the 30 and 20. Put 30% towards paying off debt (at least) and 20% toward discretionary expenses.

Now set up your budget categories. It might take a few weeks or months of tracking to see your patterns, but it will be worth it.

DESIGNED FOR PERSONAL CASH BUDGET - Save time and energy with our color coded cash envelopes specifically designed for use as a cash budgeting system.

Debt

Ok, let’s talk about debt. Every month it costs you money. You can’t achieve financial independence if you’re being held back by debt. Credit card debt is the most serious since it usually has the highest interest rate. Attack it with the snowball or stacking method.

Student loan debt can be refinanced with Credible for a better interest rate which will save you thousands of dollars over time. Upgrade can do the same for any personal loan debt you have.

It would be best if you rid yourself of this debt as quickly as possible.

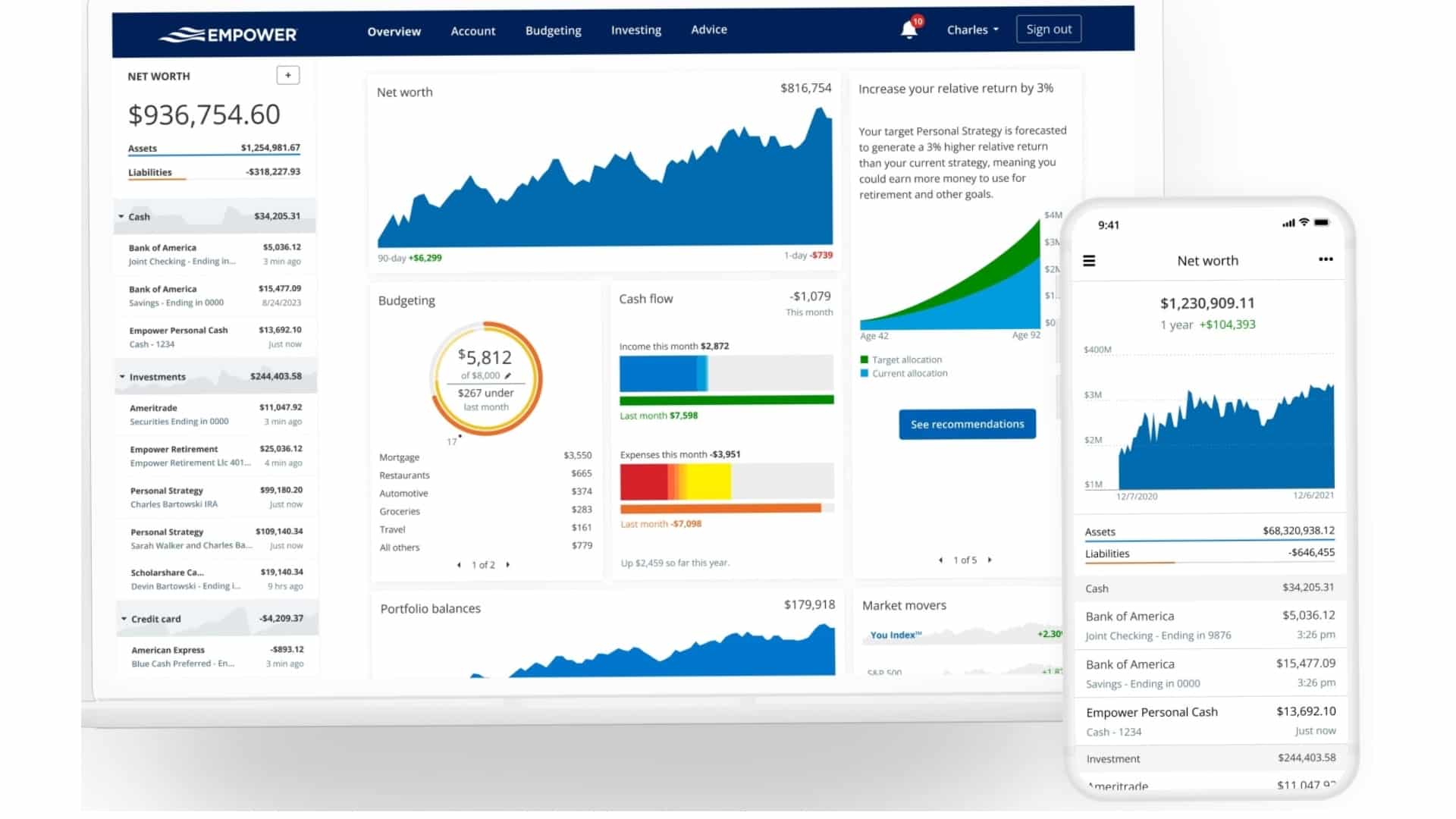

It’s essential to see your whole financial picture, and our favorite tool to use is Empower.

It’s free and will help you budget, manage your investments, plan for retirement, and calculate your net worth. Link your financial accounts, and Personal Capital will pull in all the information. This lets you see how much you make and spend, shows you what, and gives you a 1,000-foot overview of your finances.

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Step 2 – Trim The Fat

Having completed Step 1, we now understand where our money is going. However, knowing is half the battle when working towards financial independence.

The other half is slicing out the fat. No one becomes wealthy by spending all their money. Cutting the fat isn’t always easy but remember, we told you some sacrifices would be made. Once you trim your budget, you’ll see your money pile up much faster and see it was worth it.

If it seems overwhelming, choose one category a week and focus on pairing that down. Food is always a good place to start because so many of us overspend on it. Bringing lunch to work is an excellent first step. It doesn’t have to be fancy at first; make a PB & J.

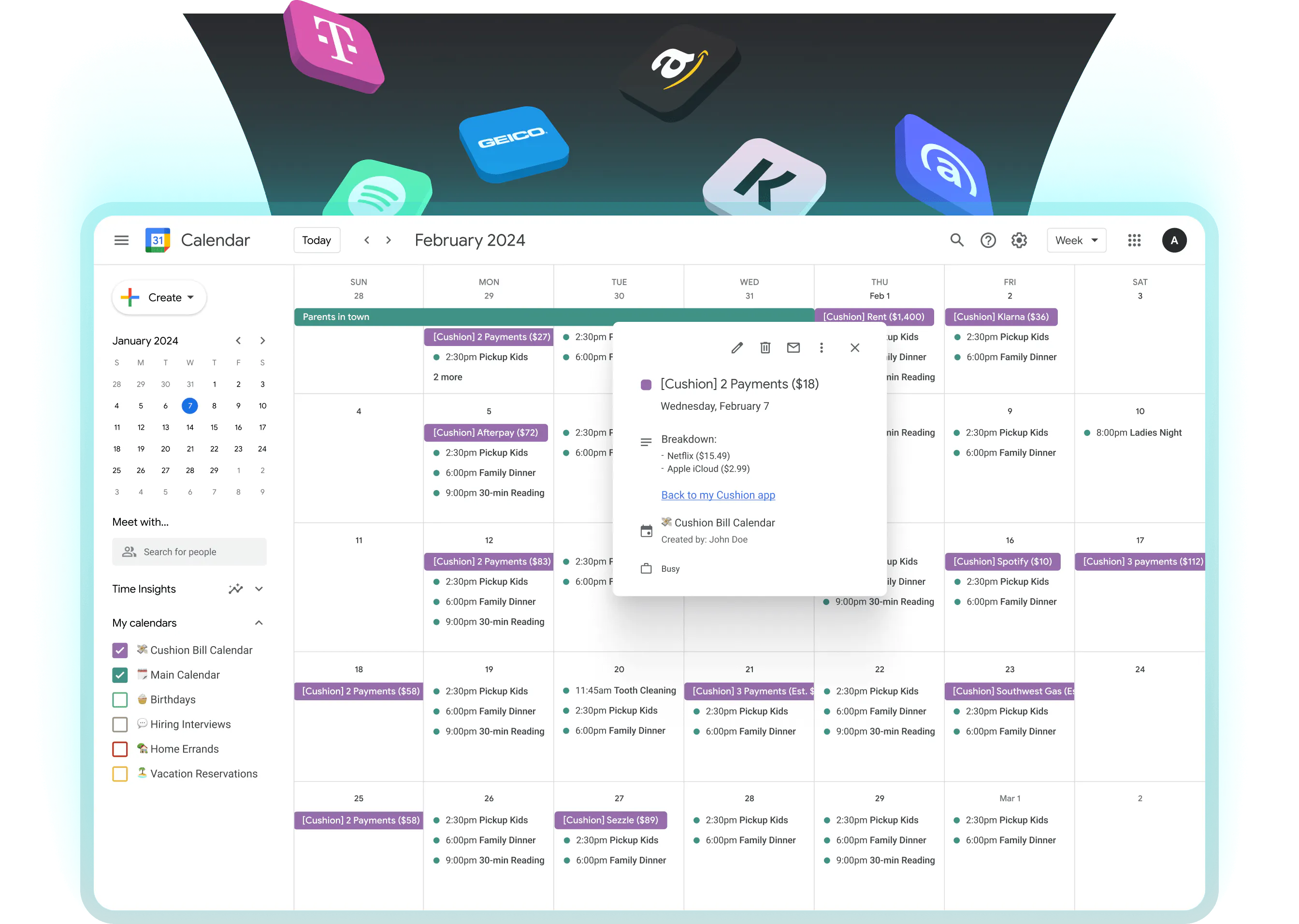

Seeing how much you save each week will incentivize you to keep going and get a bit more creative when cutting living expenses. So let Cushion do some of the heavy lifting.

Cushion is like having your own financial, personal assistant. The Cushion app automates the process of identifying and negotiating refunds for bank and credit card fees, such as overdraft, late, and monthly service charges. Using artificial intelligence, Cushion seeks to recover disputable fees on behalf of users, aiming to save them money and enhance their financial management through insights into their spending habits.

Step 3 – Increase Your Monthly Income And Productivity

At some point, there isn’t any more fat to cut, so if you want to reach financial independence, you’ll have to make extra money. Start where you are, and ask for a raise. Go in prepared. Know how many people in similar jobs in areas with a similar cost of living are making on Glassdoor.

Know the number you want. Lay out all of the reasons you deserve a raise.

While getting a raise is great, it might not mean much more money in your pocket. The average raise is just 3%. If you want to earn more money, you should be changing jobs, and often.

Those who change jobs every two years earn an average of 20% more over their careers than those who stay in the same position for longer.

Staying employed at the same company for over two years on average is going to make you earn less over your lifetime by about 50% or more.

Many of us are not fully stretched when it comes to finding time to earn extra money outside our day jobs. If we dedicate five hours daily to watching TV or browsing social media, reallocating a few of those hours toward income-generating activities could prove beneficial.

Take some of those hours and use them to do something that will aid your journey to financial independence. Consider a side hustle like driving for Uber, babysitting with Sittercity, or selling stuff on eBay or Poshmark. Try your hand at freelancing on sites like Fiverr.

Sell your skills and get paid using Fiverr's platform. It's free to join, has no subscription cost, and has over 200 marketable service categories. Create a gig, do the work, and earn money.

Everyone should have more than one income stream, but that is doubly so for those trying to become financially independent.

Step 4- Multiply Your Savings Rate

At some point, you have no more time left that can be used to make more money. But, on the other hand, you’re working a regular job and have at least one additional income stream.

We must find ways to make money that don’t require our time.

That’s called passive income, and investing is one of the best forms of passive income. When you invest your money, it makes money for you.

You don’t need much money to start investing, but you will never have much money if you fail to support yourself.

There are many ways to invest and build your nest egg; opening retirement accounts like a Roth IRA or 401k, investing in the stock market, mutual funds, index funds, rental properties – the list goes on.

Since we already have many great posts on investing, we’re not going to go in-depth here. Instead, we will link you to our best beginner investment posts.

Everything in here is low risk and low effort. We want you to have peace of mind knowing that your money is safe and growing while you focus on other essential things like your family and spending money on experiences you will remember.

Step 5- Use The Right Tools

There are plenty of tools that you can utilize to help you smooth your path to financial independence.

The right tool for the right job will make things easier and allow you to monitor your progress.

These tools can budget for you, help regulate your investments automatically, find your savings when you do spend, or even challenge you to increase your savings by rewarding you with cash for doing so!

These are our tried and tested personal finance tools.

M1 Finance

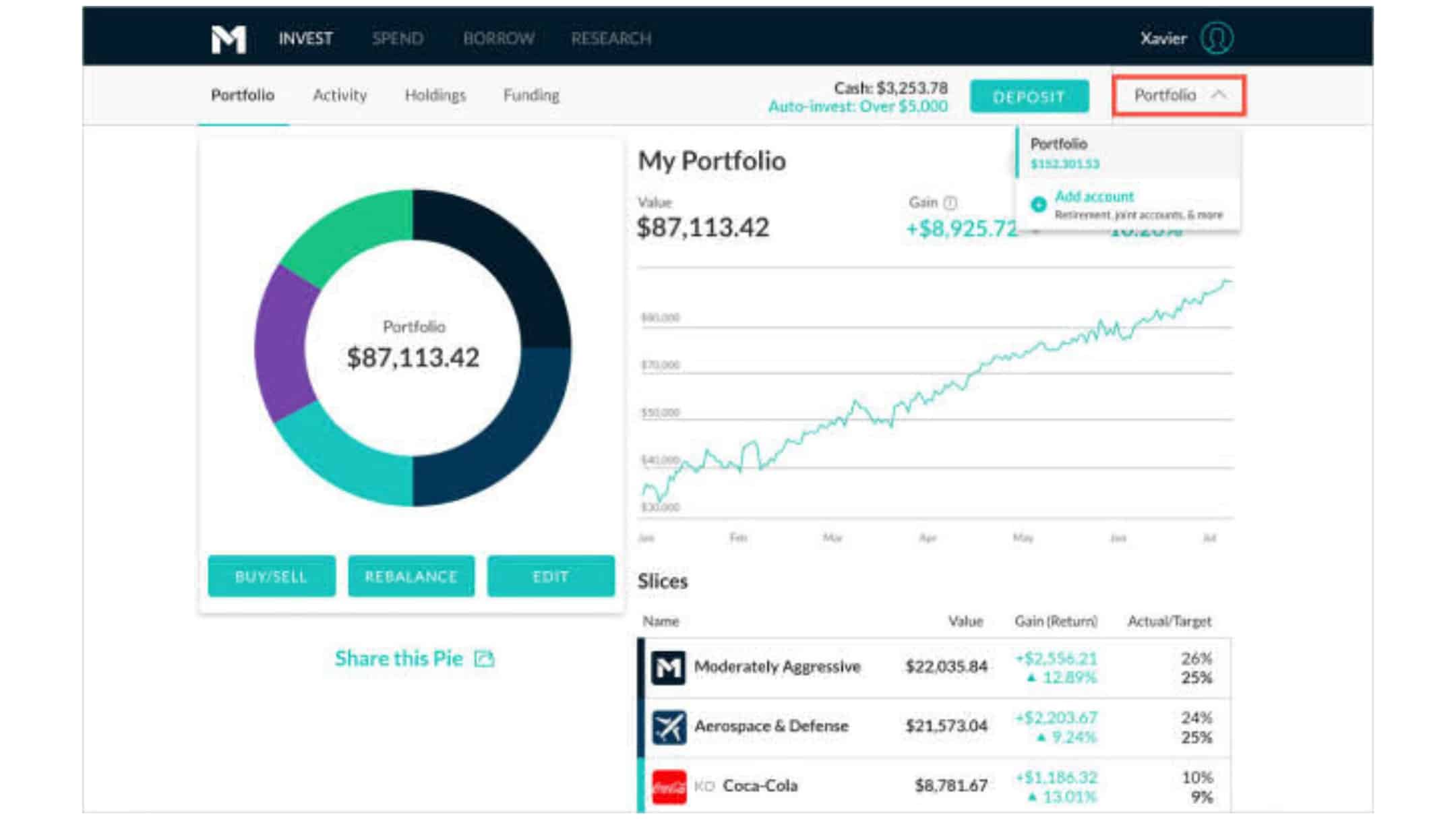

You can’t have a serious conversation about the financial tools without having M1 Finance at the top of your list.

No matter which metric you’re using, M1 Finance is hard to beat. They don’t charge fees for trading (stocks and ETFs) and have an extensive list of stocks and exchange-traded funds (ETFs).

With M1 Finance, users have access to taxable accounts, IRAs, and even LLC business accounts. They also have pre-made portfolios.

If you’re unsure where to invest, M1 Finance might be your cheaper, more straightforward option.

M1 Finance is best for those who don’t need advice; they want an inexpensive, easy-to-use platform.

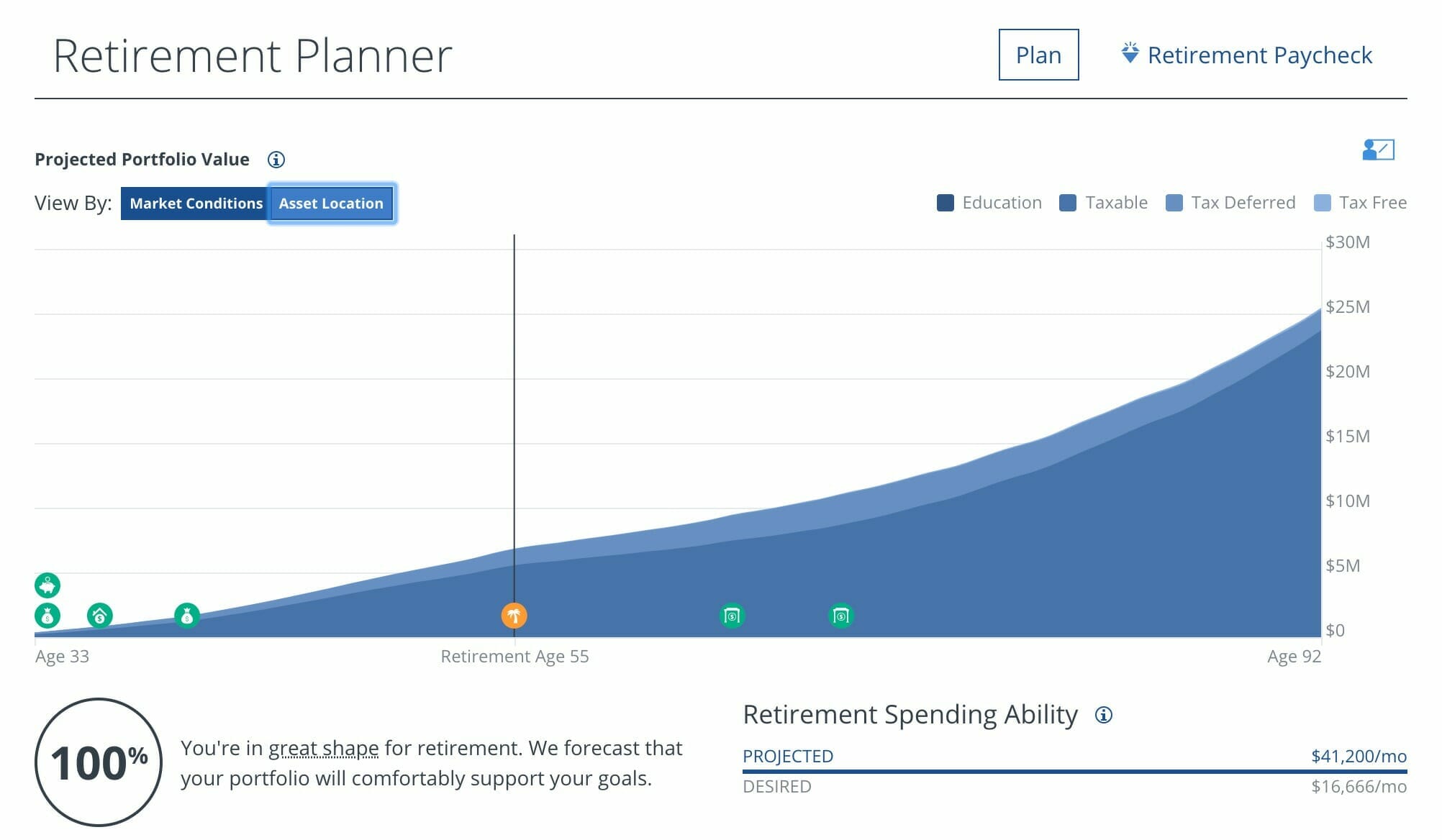

Empower

Empower can help develop your long-term financial strategy – calculate your net worth, set a budget, manage investment accounts, and plan for retirement. It offers personalized financial guidance and automated investing but requires a larger starting balance.

Be sure to check out Empower’s Fee Analyzer.

You can use a considerable percentage of your retirement money for fees over time. Personal Capital can help you find and eliminate unreasonable investing fees.

Fundrise

Did you know that investors with 20% allocated to real estate outperform those who only invest in stocks and bonds?

You’d love to do that, but you don’t have hundreds of thousands of dollars to invest in real estate.

You are going to love Fundrise! Fundrise lets “the rest of us” get in on real estate investing too.

If you’re worried about liquidity, don’t. Fundrise allows investors to liquidate any amount of their holdings quarterly.

Diversify into income-producing real estate without the dramatics of actual tenants. Fundrise eREITs are a diverse family of funds, each of which pursues a focused real estate investment strategy.

Disclosure: When you sign up with this link, we earn a commission. All opinions are our own. I am an investor with Fundrise.

Click here for the complete list of resources we use to manage our finances.

Step 6 – Advanced Investing Techniques

For people ready for a more hands-on approach (and a bit more growth potential), this section is for you!

It will take more work than a “set it and forget it” strategy, but you don’t need to be a rocket scientist to make gains here. Just remember, take risks seriously.

When ready to diversify your investments further and take on a negligible risk, look at our list of the best Vanguard funds.

A retirement account is a tax-advantaged account. If you have retirement accounts (you should!), you can further maximize them.

Gather any 401ks from previous jobs and roll them into an IRA. This allows you to consolidate retirement accounts, gives you more choices, and usually much lower fees.

And check out these super-advanced (and super-advantaged) Roth strategies. Of course, part of achieving financial independence will depend on how good you are at (legally) avoiding taxes.

These strategies will help you do that.

Vanguard is owned by their funds so they are uniquely aligned with the interest of their investors. As a result, Vanguard funds usually have the lowest fee rate in their category. Mind you, signing up is more work and requires more decisions than Betterment.

Why Is Financial Independence Important?

Achieving financial independence means doing whatever you want without worrying about money. Pursue meaningful work. Travel. Learn skills you’ve always wanted to explore. Reduce your anxiety.

If you want to live like most people can’t, you must be willing to do what most people won’t.

There will be times along the way when you want to give up. You want to do all of the things everyone else gets to do.

When you feel that way, imagine what life will be like once you’ve become financially independent. Then, you can do what you want to do when you want to do it.

No Monday morning dread, no depressing feeling when you realize your once-a-year vacation is almost over and you have to go back to “real life.”

No going to a job you hate surrounded by people you can’t stand. You have no debt keeping you up at night.

If you can stay the course and retire early, I’m sure you’ll agree that it was all worth it once you reach financial freedom.

If you want to read more, check out the fat fire (part of the FIRE movement) on Reddit and Mr. Money Mustache’s blog. Lots of like-minded folks are working towards financial independence.

Fiscal flexibility that’s funny, free and delivered weekly.

Current Project: Making bloggers money with Lasso.