Today we’re going to talk about the history of money. Where did the concept of money start, where is it going, and how does that affect you today? Most importantly, what can our past with money tell us about the future? Unlike your 7th-grade history class, this is going to be interesting.

Without money, society as a whole would come to a screeching halt. I don’t want to work for free and I’m guessing you don’t either. So, we have this concept of money that we happily, or begrudgingly, trade our time for.

But money itself has no value. Those U.S. dollar bills in your pocket only have value as long as everyone else agrees to their value.

Even bricks of solid gold have no real value, just the value we all agree to assign them. So what gives? Why do we spend so much time chasing those greenbacks?

To start off, let’s get a basic definition of money.

Money is any good that is widely used and accepted in transactions involving the transfer of goods and services from one person to another.

What Was Used Before Money?

Money wasn’t always just paper and precious metals. In fact, money wasn’t always even a thing. Today we take it for granted but there weren’t always monetary systems in place. In early human history, we didn’t have a universal concept of money.

Instead, we used the barter system. When we were all hunters and gatherers we could just trade back and forth because we all had similar possessions.

There’s some evidence that we operated in a gift economy. When people lived in small, tight-knit tribes we weren’t so concerned with getting something out of helping each other.

Plus, we were always on the move so we didn’t have the desire or ability to accumulate a lot of tangible possessions. You might have more berries than you need and I happened to catch two rabbits. So, we’d make a trade and we’d both eat that day.

But even if you didn’t have any berries I would probably feed you to make sure we both survived.

Specialization Created Problems

Once we settled down into cultivating societies we started specializing. We lost a little bit of that tight-knit closeness. Instead of being out hunting and gathering with each other all day we stayed home and worked on our small patch of land.

Being stationary also gave us the ability to keep more possessions. Suddenly we weren’t nearly as interested in a gift economy.

Some people hunted, some people farmed, and some people ran around fighting with other tribes of people. Each person wanted to be compensated for his or her efforts.

The people who farmed had way more vegetables than they could eat and the people who hunted had more meat than they could eat.

Those two parties could trade goods, and that’s fine unless the person who grows vegetables doesn’t want any meat and they aren’t as interested in giving you free vegetables.

If you’re the hunter this puts you in a real bind. You can go find a third person who has something the vegetable guy wants, but that’s really time-consuming and not very practical when you start to add three, four, five, twenty, different parties into the mix.

Add into this whole mess of a situation that the vegetable crop can only be harvested once or twice per year but hunters can get new meat every day and it’s clear the bartering system could use an upgrade.

The Universal Third Good

In order to fix this quandary, humans came up with the concept of money to be a universal third good everyone could trade for.

Instead of trading you four chickens for one sheep I gave you a coin, or some other form of money, that had the same agreed-upon value as one sheep. That way I didn’t have to walk around carrying four chickens all day just in case I ran into the sheep guy.

Anything can serve as money as long as it’s durable and hard to get. Money is simply a third good that doesn’t spoil and has an agreed-upon value.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Who First Invented Money

Throughout human history, people have used cowry shells (also spelled cowrie shells), alcohol, deerskin, metal coins, and even large stones as currency.

The ancient Chinese were the first to use the cowrie shell during the Shang dynasty. It became a widely used form of currency in the ancient world because it could be harvested from the Pacific and Indian Oceans. These mollusks became one of the first known forms of money.

In the old days you could get a goat for two cowrie shells.

Tweet ThisCoins Are So Metal

There is some controversy as to who came up with the first coins, but the general consensus is it was either the Chinese or the Greek kingdom of Lydia around 600 B.C.

The Lydians lived in modern-day Turkey and made their coins out of electrum, which is an alloy of gold and silver. Chinese coins were made from bronze and brass and were meant to mimic the cowry shell.

You read that right. The ancient Chinese started using coins because they were trying to make a fake version of the cowry shell.

Why Were There Holes In Coins?

If you’ve ever seen pictures or drawings of ancient coins you’ll notice the holes have been cut out. Why is this? This was done as a way to keep all your coins neatly bundled.

People would put a string through their coins and wrap them all together. It was also an easy way to determine value.

Different lengths of rope would have set values to them. This made making larger purchases more convenient. Instead of counting out several hundred coins you could just hand someone four ropes.

In China, as well as in the ancient Greek, Persian, and Roman Empires, they started wearing coins as jewelry. Having holes in them made them easier to attach.

The Birth of Paper Money

For hundreds of years, coins ruled. The problem with using coins or shells to pay for everything is it’s heavy and cumbersome. It’s fine to carry around enough to buy one goat, but carrying enough around to buy a whole farm is annoying.

As a solution to this, we started printing paper receipts to represent a certain number of gold coins.

The first paper money came out of China during the Tang dynasty in the 7th century AD. It took another five centuries before Europeans caught onto the practice.

A fun bit of history, paper money didn’t become a mainstay in the U.S. until the Civil War caused a coin shortage. The money supply was running low so the government had to increase taxes to ward off inflation.

In 1861 they printed Demand Notes and by 1862 printed Legal Tender Notes which closely resemble our modern dollar.

The problem with just printing paper money is it can easily be forged. Any old guy can make a piece of paper that says “This here is worth 47 sheep” but without a centralized bank, there’s really no telling which currencies had any real value behind them.

So local governments would print their own legal tender and “buy” the gold or silver coins from the citizens.

They said something akin to, “We’ll keep all the gold coins at the capital bank and give you this banknote. If you ever want them just come on up to the capital and we’ll trade you back.”

So people brought their shells, coins, and anything else they used as currency up to the capital. In return, they were given a nice, shiny, piece of paper.

Was Paper Money Really Money?

Paper money wasn’t exactly the same as a gold coin. It was essentially a receipt that represented the value of a gold coin. So, a $1.00 bill wasn’t actually worth $1.00, it was just a receipt that could be traded in for one dollar worth of coins.

When people wanted to make a purchase they’d bring their $20 banknote to the capital, get 20 gold coins and trade those coins for a sheep. The guy who sold the sheep would then take his 20 coins back to the capital and exchange them for a $20 paper receipt.

At first, the banknotes were all backed by an equal amount of actual gold or silver being held at the capital. This is known as the gold standard. But, because there’s only so much gold to be had, using the gold standard can bottleneck the economy.

As people got used to the idea of using paper slips they stopped worrying about going to the capital bank to exchange the slips for the actual thing of value.

Instead, they’d just use those pieces of paper to directly go buy something they wanted.

Fractional Reserve Banking

Banks started realizing people weren’t actually collecting their gold and silver coins so they started giving out more paper receipts than the physical gold and silver they represented.

When the government needed to generate more money, instead of finding more gold, they simply printed more pieces of paper.

This is a dangerous gamble because if everyone decided they wanted to collect their gold at the same time the bank wouldn’t be able to pay up. If too much paper money gets into the economy compared to the amount of actual gold in the bank it can cause rampant inflation.

Ironically, this is exactly what happened with the first-ever printed money. The Chinese printed too much paper currency which caused hyperinflation and completely devalued their dollar. They actually got rid of paper money for several hundred years.

Modern humans fall victim to this too. Venezuela is currently experiencing rampant inflation. As of February 12, 2020, one U.S. Dollar is worth the same as 248,487.75 Venezuelan Bolivars.

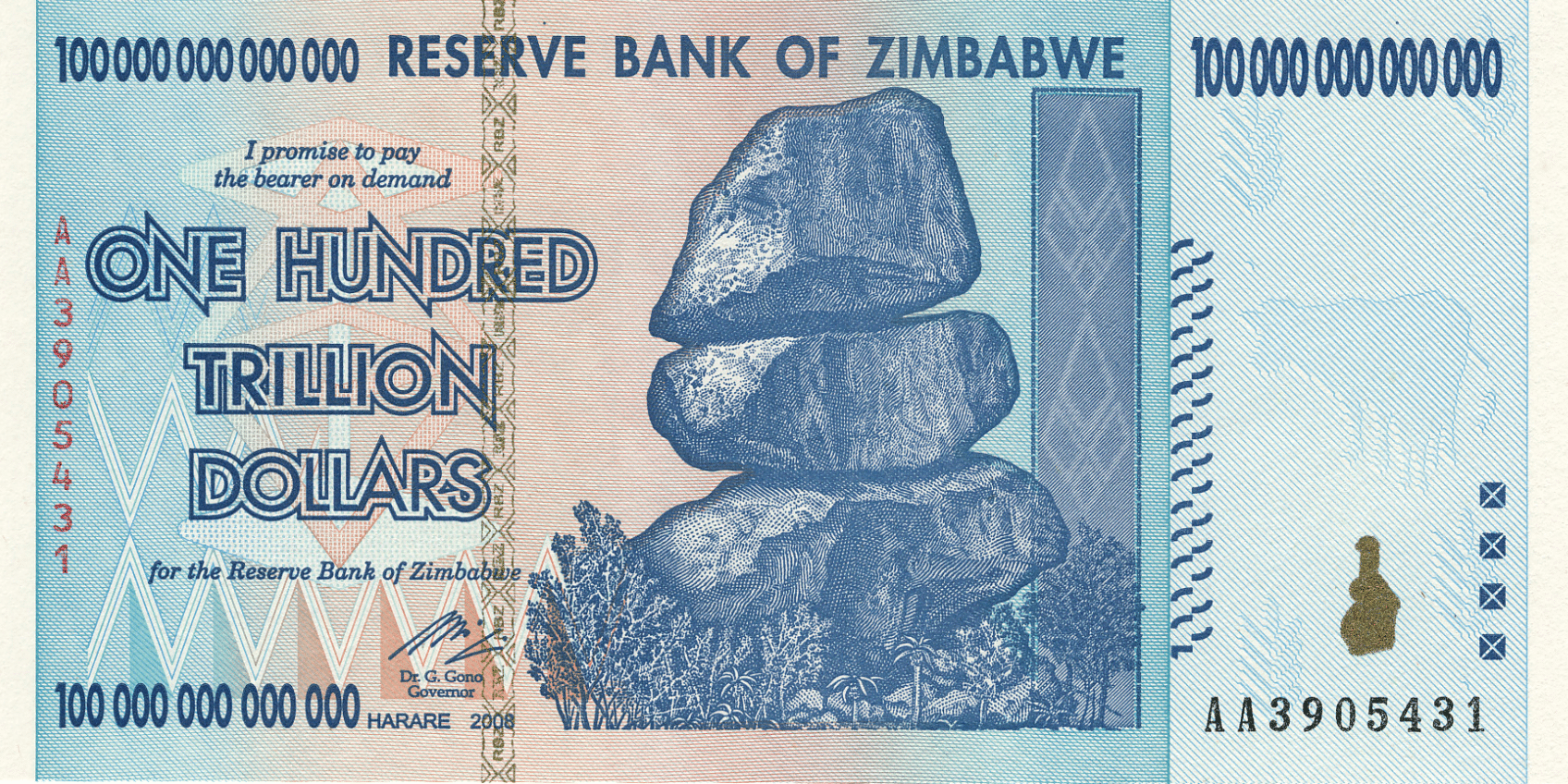

Back in 2009, the government of Zimbabwe issued a $100 trillion dollar banknote because the value of their dollar had declined so much.

During the great depression, fractional reserve banking was the reason so many banks went under. People were desperate and scared, so they attempted to withdraw what they had from the banks but the banks simply didn’t have it.

The upside to fractional reserve banking is it allows the bank to lend out exponentially more money than it otherwise could have. This keeps the economy going and theoretically protects from stagnation.

Almost every bank in the world practices fractional reserve banking. Typically banks are required to keep 5-10%, of the money deposited. The other 90-95% is lent back out into the economy.

Check Out My New Credit Card

People got used to the idea of paying for goods and services by trading paper notes back and forth. But carrying around all that cash, while better than a bag of gold coins, is still a pain.

Plus, paper money can be stolen just as easily as coins or anything else. Enter, checks.

Checks were first introduced in the United States as early as the 17th century. Unlike cash, checks aren’t worth anything until they’re filled out and signed.

Even if you managed to steal a check that was filled out you wouldn’t be able to cash it since checks also designate the rightful recipient.

Another benefit of checks is you can write any amount you want, so there isn’t the complicated matter of getting people the correct change. Checks also made it easier to make large purchases since the buyer no longer had to carry around wads of paper cash.

The downside to checks is you had to physically go to the bank to cash them since you couldn’t turn around and buy something with that same check.

Electronic Money and the Death of Checks

Today checks have become almost obsolete with the invention of computers and eventually electronic money. Filling out a check isn’t as fast or convenient as paying in cash and almost everyone has a virtual bank in their pocket in the form of a credit card.

The invention of credit cards marked a monumental shift in how we view money. We went from viewing our wealth as stacks of cash to simply seeing it as numbers on a screen.

Holding our net worth in cash would make us feel incredibly nervous and uncomfortable. We’d only start to feel relaxed once we transferred the money back into numbers on a screen.

Today when we pay for goods and services we rarely exchange anything other than data. For the first time in hundreds of years, cash is back to feeling like a receipt instead of actual money.

I don’t feel wealthier by having a few hundred dollars in my pocket. It’s only after depositing the money in my bank account that I feel ownership.

The Future of Money

So that’s where we’ve been with money. But, what about the future? What’s going to be the next big thing?

We hear words swirling around like blockchain, cryptocurrency, and BitCoin, but for a lot of Americans, this new frontier of virtual money is an intimidating step into the unknown.

Despite the reservations, cryptocurrencies such as BitCoin and LiteCoin are becoming increasingly popular since they carry so many advantages. Facebook is even trying to get in the game with their own version.

Credit Card machines work on a ‘pull’ system. The seller ‘pulls’ funds from the consumer’s account. The consumer has to trust the seller won’t keep the data or charge more than they promise.

Every time you give your credit card number online you’re trusting that the person on the other end won’t use your credit card for anything other than what you’re agreeing to buy.

The Push of Cryptocurrency

Cryptocurrency works on a ‘push’ system where the consumer ‘pushes’ a set amount of money to the seller. Encryption throughout the transaction provides security. Even a nefarious seller has no way to access any additional funds from the buyer.

People are anxious about cryptocurrency because those ones and zeros are just numbers in a computer. They like the idea that ten-thousand dollars in their savings account actually represents ten-thousand dollars worth of gold coins in a vault somewhere.

But, as we learned with fractional reserve banking, this just isn’t the case.

Cryptocurrency is just ones and zeros online, but when you think about it, so is the money currently in your bank account. Cryptocurrency has a lot of advantages over how we currently think of money.

If you want to learn more, here’s a really good infographic that succinctly explains some of the advantages.

As people get more comfortable with the idea of cryptocurrency as real currency I think we’ll see it start to take over. We might look back on credit cards as the stepping stone that got us from paper cash to cryptocurrency and beyond.

It’s very possible that in a hundred years people won’t equate cash with money. Paying for something with paper money will seem as antiquated as paying for something with gold bars feels for us today.

How Does Knowing the History of Money Help You?

New forms of currency caused the people to worry. We worried about switching from cowrie shells to coins. Then, we worried about switching from coins to paper to electronic money.

But, looking in the rearview of history we can see that using paper is an infinitely better system than using any previous medium of exchange that came before it.

Now we can see that having everything online is infinitely better than having a briefcase full of cash.

I’ve always been hesitant about cryptocurrency because it just doesn’t feel like it has real value. While I’m not ready to close my bank accounts just yet, learning about the history of money has helped put my mind at ease.

Whatever the next phase of currency looks like it will make our current idea of money feel outdated.

Tangible Next Step

You might not be ready to purchase your first Bitcoin either, but there are a few things you definitely should start doing with your money.

If you’re hesitant to dive into the stock market do this: Take the cash from your brick and mortar bank and put it in a high yield savings account. It’s 2020, there are several great online banks that actually pay you to keep money with them.

Keeping a huge amount of cash in a regular bank account is like paying for Taco Bell with a gold bar.

Businesses like CitBank and

Over the long term investing in low-cost index funds is your best bet to making your money work for you. If you’ve got some cash that you don’t have all your money tied up in the market, put some in a high-yield savings account.