- 1. Resourcefulness

- 2. Gaining Momentum

- 3. Risk vs. Reward

- 4. Meaningful Relationships

- 5. Reputation

- 6. Luck Meets Opportunity

- 7. Celebrate Others

- 8. Mentor Mindset

- 9. You Can’t-Do It All

- 10. Embracing Competition

- 11. Know When to Quit

- 12. War of Attrition

- 13. There’s No Such Thing As Done

- Show Notes:

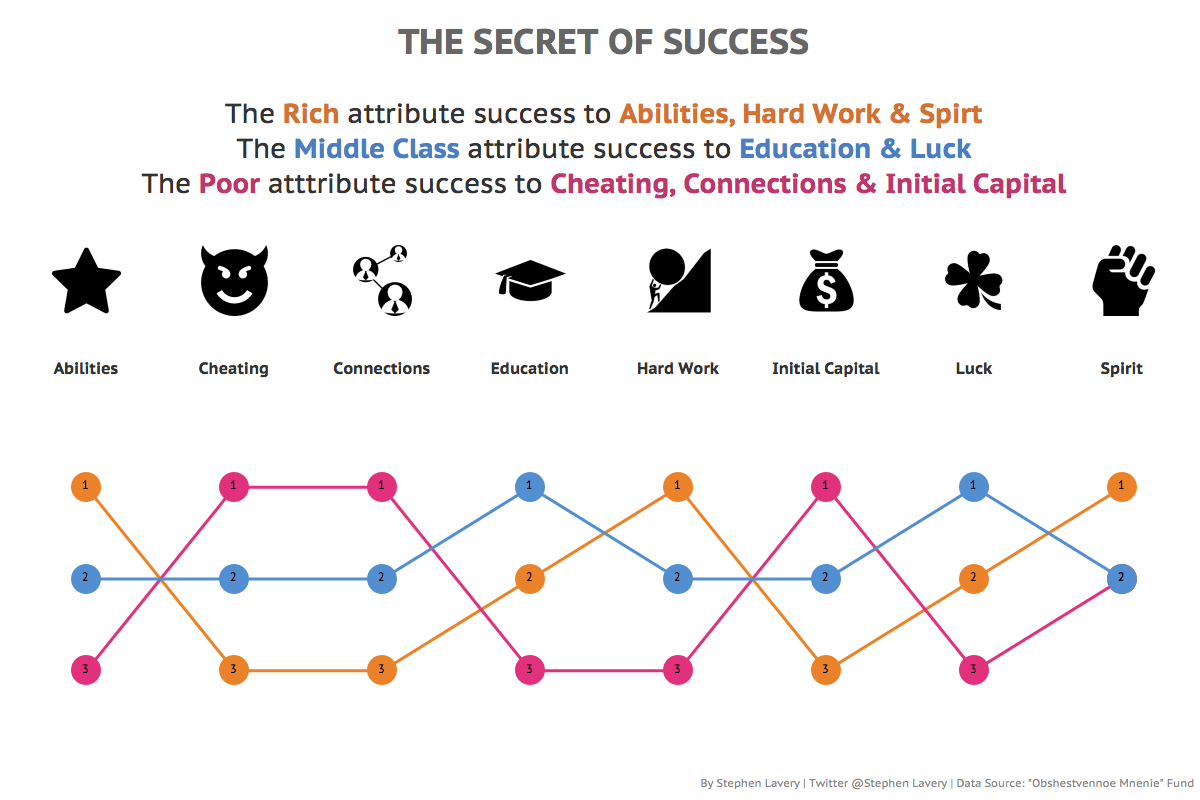

Maybe you are rich. Perhaps you are poor. Perhaps you have experienced being both at some point in your life. If you haven’t figured it out, being rich isn’t all about money. It’s about well-being, abundance, time, success, and the right mindset.

Social issues contribute to poverty; however, rich vs. poor mindsets can also drive wealth and success.

Many poor people with a rich mindset are financially poor due to circumstances. And there are many trust fund babies with a poor mindset.

A simple shift in your mindset can point you in the right direction to becoming as wealthy as you want.

1. Resourcefulness

A rich mindset understands that the first goal is to gain a surplus of resources. Then, use that surplus to accelerate things. Accelerate education. Accelerate a business. Accelerate the next generation.

A poor mindset immediately sees a surplus as an opportunity for consumption and inflates its lifestyle.

Challenge Yourself: Create a 30-day list. If you have to wait for your paycheck to buy something, it better be something you absolutely need. Think about where you can accelerate things and build your personal advantage.

2. Gaining Momentum

A rich mindset seeks to spend their time, resources, and energy on work that continues to pay off long after the effort has been invested. A rich mindset is all about getting a flywheel spinning and building momentum. They are creating systems that continue to generate value on their own.

A poor mindset is all about short-term returns. Hours-for-dollars. Resources invested without an immediate return are resources wasted.

Challenge Yourself: Investing is critical, and you need to find space for it. Your 401k is a great start. Another area of focus is your personal productivity.

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

3. Risk vs. Reward

A rich mindset is willing to invest resources with seemingly no reward right away. Not everything has a clear path to profitability; you have to take a chance and try. It’s about risk vs. reward.

A Poor mindset’s immediate thought is, “What’s in it for me?”. Why pay money to fly to that conference, pay for the hotel, and spend all the time when they’re not even paying you?

Challenge Yourself: You need to be willing to take calculated risks because no reward worth discussing comes without risk. Being uncomfortable is Important; it means you’re growing.

4. Meaningful Relationships

A rich mindset seeks to build relationships based on trust, shared values, and mutual respect. People with a rich mindset help others and cultivate relationships without expecting anything in return.

A poor mindset thinks, “I scratch your back, you scratch mine.”

Challenge Yourself: You’re the average of the 5 people you spend the most time with. Start making new friends who have a rich mindset. Go to a local meet-up group and meet some people you can learn from.

Be the dumbest person in the room. Make connections with smarter people, and you’ll all win. Smarter people make smart people even more successful.

5. Reputation

A rich mindset understands that its reputation is everything, that trust and respect are earned slowly, through hard-fought, bloody effort – and that both can be lost instantly.

A poor mindset believes it can get away with compromising its reputation to make a quick buck.

Challenge Yourself: Take the high road. Always consider the consequences of your actions/decisions.

6. Luck Meets Opportunity

A rich mindset knows that the world isn’t fair and deals swiftly, humbly, and practically with reality. It knows the world owes it nothing, that the universe is indifferent to its existence, and that the default for life is suffering and death. All successes are improbable and should be appreciated as such.

A poor mindset is consumed by the unfairness of the world and wastes time complaining about it. It feels like the world owes it something and waits for it to be handed out.

Challenge Yourself: Entitlement. Get something you want this week. Then, if you get it, appreciate that luck met opportunity. If you don’t get it, appreciate your effort and take some time to try and understand why. Be humble.

7. Celebrate Others

A rich mindset celebrates the successes of others, embraces the competition, and often befriends it. You have two choices, tear down another person’s success or be inspired by the example.

A poor mindset feels jealousy and bitterness about the successes of others, and it looks at everything as a zero-sum game.

Challenge Yourself: There will always be people who have accomplished more and most likely have done it better than you. Find a competitor and make them your mentor. Lead with humbleness and gratitude, and you will be greatly rewarded.

“Change The Way You Look At Things And The Things You Look At Change” – Wayne Dyer

8. Mentor Mindset

A rich mindset understands that one can never know everything and that something can be learned from everyone.

A poor mindset deludes itself into believing it knows everything and those opposing perspectives are wrong before even hearing them.

Challenge Yourself: Seek to place yourself in a situation where you are inexperienced and uncomfortable. If you are against gun control, read some well-thought-out arguments for gun control. If you are for gun control, read some well-thought-out arguments against gun control.

Allow yourself to build a broad well-informed perspective and allow yourself to change your mind. The most idolized people in history are almost uniformly unafraid of changing their opinions based on new information.

9. You Can’t-Do It All

A rich mindset understands that it cannot do everything and that even if it could, it would create greater value by focusing on its core strengths. It knows that the right team is greater than the sum of its parts.

A poor mindset deludes itself into thinking that it can do everything if it just works hard enough.

Challenge Yourself: Read Essentialism. Just because something needs to be done doesn’t mean you need to do it. The Way of the Essentialist isn’t about getting more done in less time. It’s about getting only the right things done.

The Way of the Essentialist isn’t about getting more done in less time. It’s not about getting less done. It’s about getting only the right things done. It’s about the pursuit of the right thing, in the right way, at the right time.

10. Embracing Competition

A rich mindset embraces competition and knows that iron sharpens iron.

A poor mindset is discouraged by Competition. It complains, “Someone else got there first,” or “They’re obviously going to catch up to me; I might as well quit now.”

Challenge Yourself: Listen Money Matters was late to the personal finance game. Before I started, multiple people had sold their brands for millions of dollars – people I’ve met. Yet, somehow, there was still space.

Lady Gaga existed before Taylor Swift, and one doesn’t hamper the success or potential growth of the other. There’s a piece of the pie for everyone, and the first step is showing up.

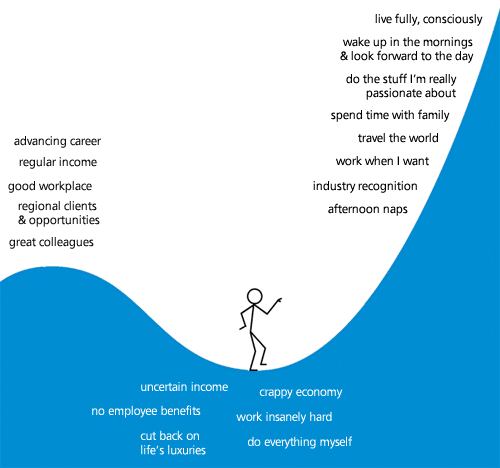

11. Know When to Quit

A rich mindset quits strategically. It plans to quit in advance when it realizes the potential gains of pursuit are either unreachable with current resources or aren’t worth the pain of the work involved.

A poor mind quits in reaction to pain and short-term discomfort.

Challenge Yourself: Quitting a job over an argument with a boss vs. using that argument to fuel their job hunt and getting an alternative before they leave their current position. Shitty things happen every week; let those experiences propel you forward. Don’t be so reactionary.

12. War of Attrition

A rich mindset sticks it out when the going gets tough, provided that the pursuit is worthwhile. It understands the idea of “The Dip” – that anything worth doing will be hard. It understands that the rewards are reaped by those who push through the difficulties of a pursuit precisely because the will to push through is scarce.

A poor mindset sticks things out due to stubbornness. It places too much importance on sunk costs.

Challenge Yourself: I attribute much success in my professional life and business to the war of attrition. People quit; you need to outlast them. However, understanding that spent time and money is gone, so their expenditure shouldn’t heavily weigh on your decision.

13. There’s No Such Thing As Done

A rich mindset understands that there is no “I made it.” No “done.” Challenges and learning define life.

A poor mindset believes that one day they’ll be able to “retire” – to kick back and do nothing. That all work is simply “paying dues” on the way to a life of leisure. Ironically, this kind of mindset stifles the ambition and drive required to ever get to the point of having that kind of life as an option.

Challenge Yourself: If you didn’t have to work for the rest of your life, what would you do every day? This hobby, be it gardening, cooking, teaching, etc., should be something you focus on and cultivate.

Skillshare is an online learning community offering thousands of classes from design to marketing to analytics. Discover hidden passions and explore new skills taught by industry leaders. Or, become a teacher, share your expertise, and make money.

It is no accident that we built a business out of our hobby. All non-profit organizations, music schools, and small businesses started as a challenge/learning experience and eventually grew into something even more meaningful than it was originally.

Show Notes:

Fiscal flexibility that’s funny, free and delivered weekly.

Current Project: Making bloggers money with Lasso.