- What Is Lendkey?

- What Is Student Loan Refinancing?

- How Lendkey Works

- What Lendkey Offers

- Lendkey Step-By-Step

- Private Student Loans

- Lendkey Requirements

- Refinancing Your Student Loan

- Fixed Interest Rate v. Variable Interest Rate: What’s the Difference?

- Does Lendkey Offer Protection Like Federal Programs Do?

- About Lendkey Lenders

- Resource Center and Educational Tools

- Refer and Earn

- Lendkey Pros

- Lendkey Cons

- Final Thoughts

Did you know 45 million Americans have student loan debt? How’d you like to be $38,000 in the hole after graduating college? How about $100,000? Or as Forbes titled it in a recent headline “The $1.5 Trillion Crisis“.

Student loan debt is now the second-highest consumer debt category – behind only mortgage debt – and higher than both credit cards and auto loans.

While student loan debt doesn’t appear to be going away anytime soon, fintech companies are disrupting the system. Thanks to digital platforms like Lendkey, borrowers are gaining access to a broader range of more straightforward, low-cost alternatives to big banks.

I’m sure you’ll agree with me when I say that applying for a loan can be a daunting task – especially if you’re a student. Juggling monthly payments, interest rates, and debt is a shock to your system if you’re a newbie.

Where do you even look? Is there a one-stop-shop where you can compare different rates? A place where you (the borrower) can connect with potential lenders to pay for college or graduate programs?

Companies like Lendkey are making it easier for borrowers to obtain loans at discounted rates than traditional big banks offer.

In this Lendkey review, I’m going to show you the difference between fixed and variable interest rates (and how they affect the total amount of money you’ll pay), why it’s essential to apply for federal loans before applying for private loans and why you should consider refinancing.

I’m also going to show you what Lendkey brings to the table and whether they’re worth it.

Giddy up.

What Is Lendkey?

Lendkey was founded in 2009 after the financial crisis. Sickened by Wall Street’s recklessness and total disregard for Main Street, USA, they sought a better alternative to what financial institutions were offering.

Big banks had failed us.

With fintech companies on the rise, Lendkey and its partners invested $30 million to grow a digital lending business.

Lendkey is a cloud-based lending platform connecting borrowers with community banks and local credit unions. Their mission:

To make lending simple, accessible, and less cumbersome.

They’ve helped over 90,000 people and have $2.8 billion in funded loans. Their primary focus is on local and not-for-profit lenders.

They also provide borrowers with an excellent resource center and educational tools allowing them to learn about the lending process and how to make smart borrowing decisions.

Lendkey has been featured in:

- Forbes

- Wall Street Journal

- American Banker

- Credit Union Times

And received praise from these reputable companies:

- NerdWallet

- Lending Tree

- Mint

- Credit Karma

- Student Loan Hero

Lendkey connects borrowers with lenders. They’re the middleman. They aren’t a bank.

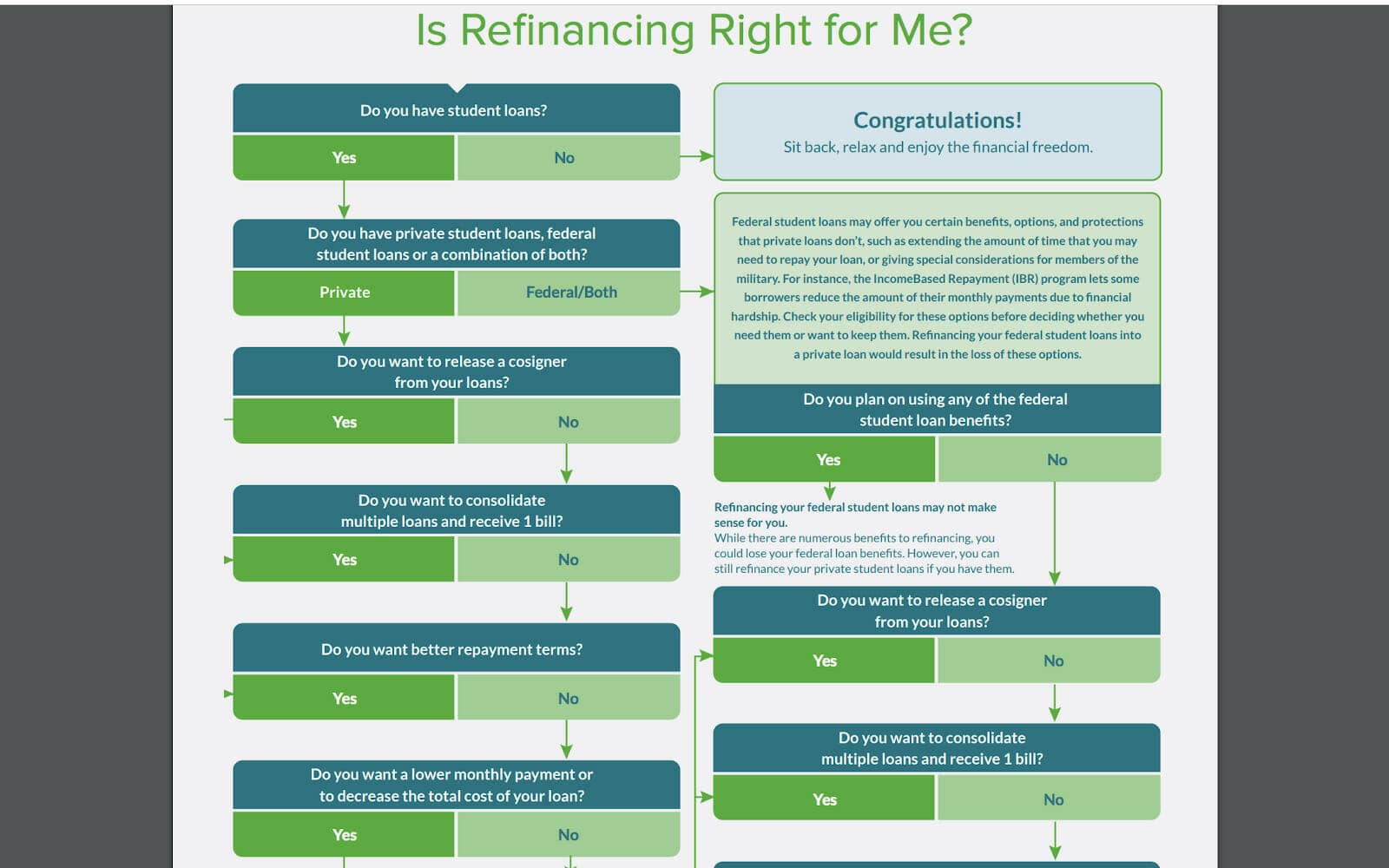

What Is Student Loan Refinancing?

Lendkey breaks the entire process down with easy-to-follow info graphs like this one.

Do you have multiple loans through different lenders? Are you paying a high-interest rate? Would you like to pay down your loan in a shorter time? If you answered yes to any of the above questions, refinancing might make sense.

When you refinance your student loans, you house them under one roof. It’s called consolidation, and it has many perks. Things like:

- Lowering your interest rate (effectively reducing your total amount due over the life of the loan)

- Single monthly payments

Who wants to be writing multiple checks to an assortment of lenders? Wouldn’t it be easier to send one monthly payment?

Yes!!!

When you refinance your student loan, your lender (community bank or credit union) buys it from your original lender(s) and pays it off.

It’s like buying protection from the mob only in this instance, the mob is lowering your total loan amount and not raising it. Imagine that…

Using Lendkey’s calculator shows you of any savings you’ll incur and whether or not it’s worth it. People refi all the time if it means they’ll save money.

How much money can you save? It’s possible to save between $10k-$30k over your loan’s lifetime – maybe more.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

How Lendkey Works

Using Lendkey is like putting together a piece of furniture you bought at Ikea – with explicit directions and lots of hand-holding.

Start with listing your existing student loans on your application or when applying for a private loan. Lendkey will then connect you with banks and credit unions offering low, competitive rates.

Lendkey doesn’t issue the loans because they’re not a bank. Comparing rates requires a soft credit check and will not hurt your FICO credit score.

Once approved, you’re left with a single loan and low monthly payment. A benefit of cloud-based lending is how fast you receive your results – typically in 15 minutes.

What Lendkey Offers

Lendkey offers student loan refinancing for federal and private student loans. You can consolidate both loan types, but be sure you know of any benefits you may lose when consolidating federal student loans (certain federal loan types come with benefits that are lost with a refi).

Lendkey also offers private student loans for qualifying applicants. You have the option to use a cosigner on your loans as well as a cosigner release.

Lendkey doesn’t have any origination fees. These are pesky processing fees charged by many big banks between .5% and 1% – just for setting up a loan account. That adds up to hundreds of extra dollars! When you get a loan through Lendkey, those fees are waived. You’re not getting nickel and dimed.

All of Lendkey’s partners (community banks and credit unions) are in one place.

What’s that mean for you?

A one-stop shopping experience where you’re able to compare fixed and variable interest rates, loan terms, and the number of monthly payments you’ll be required to make.

When you enroll for automatic payments (ACH discount) Lendkey rewards you with an interest rate reduction of 0.25%. Remember, small things add up over time.

In cases of financial insolvency, borrowers are granted forbearance in six-month increments. You’re allowed three for a total of 18 months which is the highest in the industry.

Must be a U.S. citizen or permanent resident to acquire Lendkey’s services.

Lendkey Step-By-Step

Creating an account is easy. Provide your name along with some basic contact info and your loan information. Lendkey will ask you:

- The reason for your student loan refinance

- Your goals (secure a lower interest rate, reduce monthly payments, the loan in a shorter time frame)

- Your existing loan amount

- School and degree earned

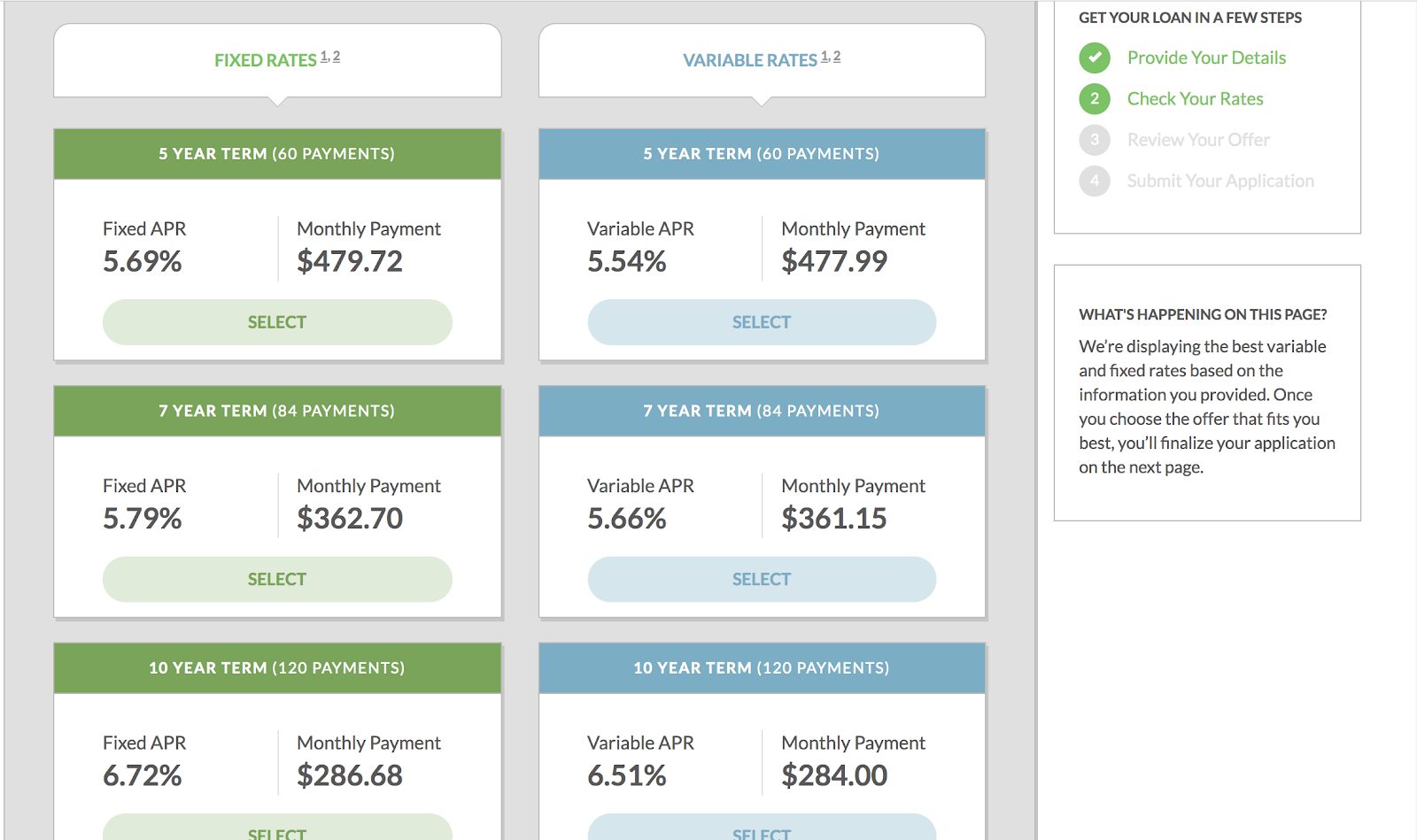

During this process, you must consent to a soft inquiry credit check. No worries as it doesn’t affect your credit score. After the soft inquiry, you can decide on a variable rate or a fixed rate.

Pro-tip: Opt-in for automatic payments and receive a .25% reduced APR.

Lendkey offers loans for five, seven, 10,15, and 20-year terms.

Next, you’re asked which state you reside in (Lendkey currently does not offer its services in Maine, Nevada, North Dakota, Rhode Island, and West Virginia).

For example, I used my home state of California, and it took me to their partner, Sallie Mae. You’ll have to provide your social security and date-of-birth.

There are several loan types available including:

- Undergrad

- Parent

- Graduate School/Health Professions Graduate

- MBA

- Medical School

- Dental/Dental Residency

- Law School/Bar Study

- Medical Residency/Relocation

Clicking on the loan type provides you with the loan’s specific details.

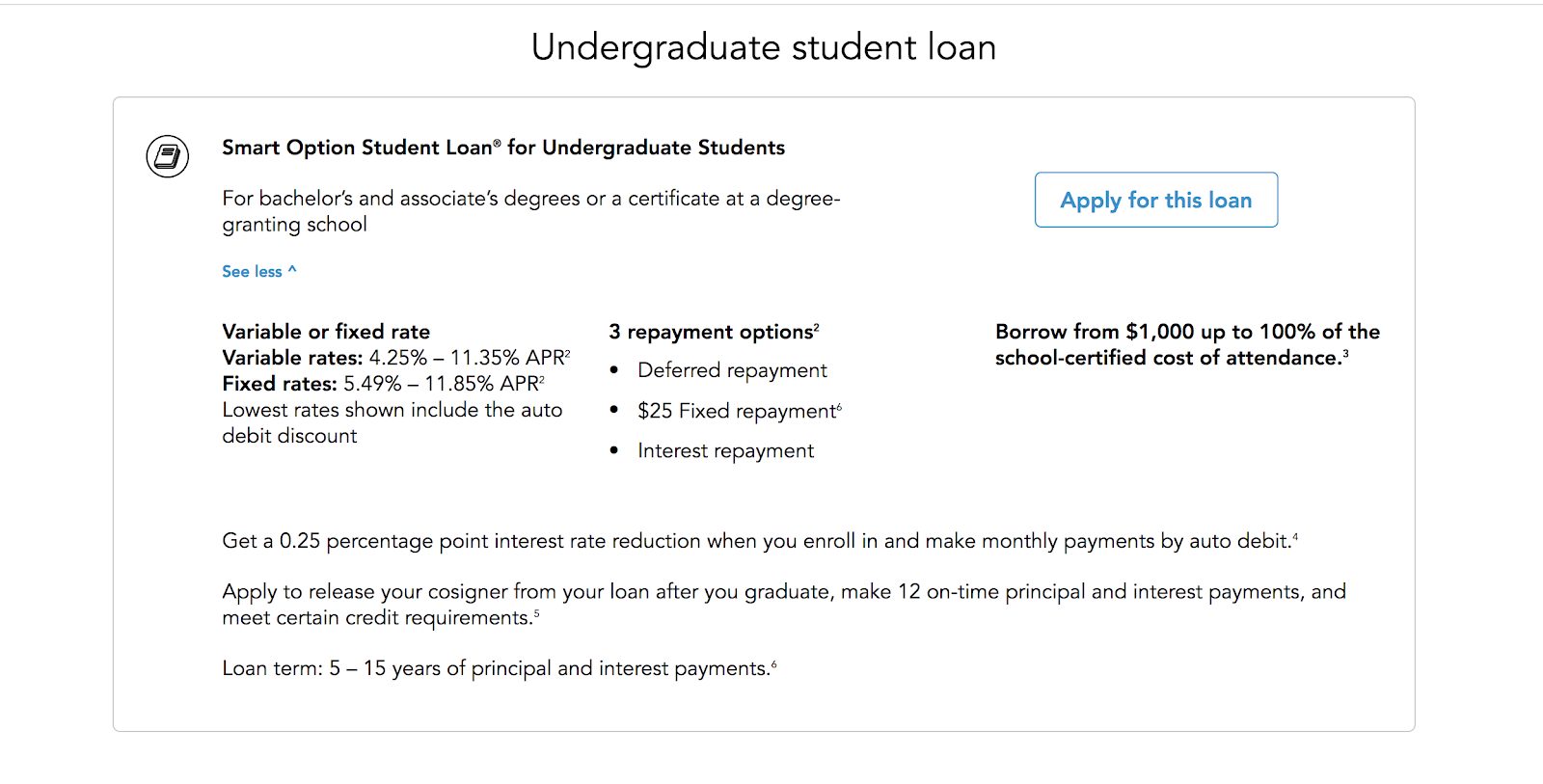

Undergrad loans run between a $5,000 minimum and $125,000 maximum while graduate degrees can apply for loans up to $250,000 and up to $300k for medical, dental or veterinary degrees.

Private Student Loans

For those looking to close the gap once they’ve exhausted all other avenues, Lendkey does offer private student loans in addition to refinancing.

You can leverage a private student loan when you’ve tapped out federal loan or grant options.

Tweet ThisThese loans pay for qualified education expenses like tuition, housing, books, and other school-related fees. They’re a credit-based loan which means your credit score will affect your rate and terms.

If you don’t have the most substantial credit score (no worries if you don’t), you can use a cosigner. The benefits of having a cosigner involved can mean a lower interest rate and a higher chance of getting approved – a win-win for you.

Always check for available federal loan and grant options by completing a Free Application for Federal Student Aid (FAFSA, found at www.fafsa.ed.gov) before applying for a private student loan.

Often, federal loans will have lower interest rates (or zero interest while you’re in college or your loan is deferred) and benefits should you have any financial hardships or are affiliated with the military.

Private student loans should always be a second option.

The primary difference between federal and private loans are:

- Federal loans are offered through the U.S. Department of Education with a fixed interest rate.

- Private loans are credit-based with either a fixed or variable interest rate option and are available through credit unions or banks.

Compare rates at places like CommonBond to ensure you’re getting the best available options.

Usually, these loans are available for 10-year terms and have an in-school repayment requirement of $25 a month.

Lendkey Requirements

To receive a private student loan through Lendkey, you must meet specific eligibility requirements:

- Earn a minimum of $24,000 annually

- Monthly debt payments are less than three times your total income(33%)

- Minimum credit score of 660

- Graduate from an institution that’s part of a Title IV federal student aid program

- Must be an American citizen or permanent resident.

***Lendkey doesn’t offer loans in Maine, Nevada, North Dakota, Rhode Island, and West Virginia

Refinancing Your Student Loan

Refinancing will afford you:

- Loan terms of five, seven, 10, 15, or 20 years

- No origination fees

- Variable rates ranging between 2.81% to 8.79% (w/AutoPay)

- Fixed rates ranging between 3.64% to 8.92%

***Be sure to read the fine print when you’re shopping for the best rate. For example:

Lendkey’s lowest advertised 2.81% variable APR is only available on five – year loan terms and to people with a credit score of 830.

You are afforded flexible options like interest-only payments for the first 48 months when signing up for a long-term loan(for example 15 or 20-year terms).

Cosigner release is also available to participants when paying on-time and in full for at least 12 consecutive months (terms vary).

***Lendkey student loans do require all of its applicants to have completed their associates, undergrad, graduate, or doctorate from a Title IV eligible school.

When considering refinancing your federal and private student loans, re-examine your federal loan terms as they come with certain benefits like military discounts, and loan forgiveness.

You may also lose access to federal programs like income-based repayment and Pay As You Earn. When you refinance your federal loans, you lose those benefits. Why?

Because the Federal Direct Consolidation Loan program doesn’t consolidate private loans into federal loans.

If you only have federal loans, refinancing is done through the Federal Direct Consolidation Loan program.

Fixed Interest Rate v. Variable Interest Rate: What’s the Difference?

A fixed rate loan means your interest rate will not change for the life of the loan. Some people prefer a fixed rate loan because of its reliability. Your rate doesn’t change which means your monthly payments will not change – no surprises for you.

That static, constant payment offers borrowers peace of mind. However, it might mean you’ll pay more over the loan’s lifetime. Individual fixed-rate loans can require a higher repayment schedule up front.

Variable rate loans have a fluctuating interest rate that moves in sync with the LIBOR and Federal rates (on a global scale, the LIBOR is the most widely-used benchmark when referencing interest rates).

For those who are more concerned with paying off your loan in a shorter time, a variable rate loan might make more sense.

Variable rate loans are a bit of a gamble. On the one hand, you could end up paying less in interest if rates remain low. On the other hand, if interest rates rise, you could end up paying more.

The interest rate will fluctuate but may never reach a high amount before you’ve paid off your loan. Variable interest rates also mean your monthly payments will vary. Assess your circumstances and talk with a professional to determine which is right for you.

Does Lendkey Offer Protection Like Federal Programs Do?

If you lose your job or have trouble making payments, Lendkey does offer some assurances. While it may not be on par with specific federal programs, Lendkey does offer up to 18 months forbearance in cases of financial hardship. This is the longest term offered in the student loan refi industry.

***It isn’t 18 consecutive months. Your payments will be frozen for a six-month term up to three times.

About Lendkey Lenders

Lendkey isn’t a lender, creditor or bank. Instead, they’ve partnered with reputable companies like:

- American Bankers Association

- CUNA Strategic Services

- Allied Solutions

- NAFCU Services

- Leverage (Your Advantage)

They’re a turnkey digital solution much like Roofstock is with their

Lendkey connects borrowers with lenders. In Lendkey’s words:

We’re an end-to-end digital lending solution designed to help banks and credit unions offer consumers the loans they need.

Lendkey helps community banks and credit unions reach a wider audience and grow their business by assisting in the creation of consumer loan products. Their products are more accessible for borrowers than what many big banks are currently offering.

Lendkey has an assortment of asset classes for every lender which means a greater selection of loan options for you.

Resource Center and Educational Tools

If you’ve got questions about anything loan-related, Lendkey has the answer. They have a robust collection of resources at your disposal including:

- Scholarship Search

- Intuitive Student Loan Calculator

- Blog

- How-To sections about debt consolidation, paying for college, consolidating versus refinancing and more

- Ultimate Guide to Student Loan Refinancing

Refer and Earn

They’ve even got a referral program called Refer and Earn. You have the chance to get paid every time a friend gets approved – even if they decide not to accept the loan.

- Earn $50 for every friend approved

- Earn $200 for every friend who takes a Lendkey loan

- No caps/limits on referrals

Lendkey Pros

They’re the IKEA of putting your loan together. Lendkey is there with you every step throughout the entire application process.

- Lendkey touts a competitive industry low rate

- No origination fees

- 0.25% ACH interest rate deduction (automatic payments)

- Backed by some of the most reputable names in the business like the American Bankers Association, NAFCU Services, and Credit Karma

- Cosigner release after proving for a set time-period you’re a reliable borrower

- User-friendly experience and easy-to-use loan consolidation tools

- Fantastic Resource Center and Educational Tools

- A+ Better Business Bureau rating

Lendkey Cons

- Not all loan disclosures are conspicuous so do your homework and read the fine print. Everything may not be on their website because of the ample amount of partners Lendkey has

- Limited to Lendkey partners only. Better rates may be available to you on another platform like SoFi or Earnest. It’s essential to shop around.

Final Thoughts

The system isn’t perfect. Graduating with a degree only to be shackled by debt is a terrible way to start life after college.

According to Lendkey, the class of 2018 is predicted to retire at age 72 – not 65.

Is Lendkey right for you?

Your chances of finding a loan from a community bank or local credit union with better terms than a big bank are higher because of platforms like Lendkey. Are there other options? Sure.

However, student loan refinancing has never been easier because of what Lendkey offers. Borrowers can find lower rates and better repayment options. These potential savings could amount to $30,000 or more.

And, they walk you through the entire process with complete transparency. Overall, I’d say Lendkey is a great company looking to fix a flawed system. Thumbs up!