Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

Credit card debt can seriously hold you back from reaching your financial goals. It makes it harder to save for a home, invest, or build real wealth. Even if you make your minimum payments every month, high interest rates—often 15% or more—can keep your balance from going down. Instead of moving forward, you’re stuck paying mostly interest with little progress toward paying it off. Tackling this debt should be a top priority if you want to get ahead financially.

Credit card debt can feel overwhelming—and on top of that, there’s the frustration of knowing how you got there. Maybe you lost your job and had no emergency fund, so you had to rely on credit to cover basic expenses. Or maybe you overspent on things you didn’t really need. Either way, the result is the same: a growing balance that feels impossible to manage. The key now is to stop beating yourself up and start focusing on how to fix it.

The truth is, you’re stuck in credit card debt hell.

The good news? You can get out. It won’t happen overnight, and it won’t always be easy—but with the right strategy, you can make real progress faster than you think. It doesn’t matter if you’ve got a small balance or you’re drowning in debt, or if you have a high credit score or a low one. There are proven ways to pay off your credit card debt, take back control, and start building real wealth.

You’re Not Alone

It might not make you feel better, but you’re definitely not alone if you’re dealing with credit card debt. Millions of Americans carry a balance every month, and with rising interest rates, it’s getting harder to keep up.

That means you’re in the same boat as a lot of people, many of whom are struggling with the exact same financial stress. The important thing is recognizing the problem and taking steps to tackle it head-on.

As of the latest data, Americans owe a record $1.21 trillion in credit card debt. On average, individuals carry about $6,580 in credit card debt. This represents a significant increase over recent years, driven by factors like inflation and rising interest rates.

The amount of credit card debt in America is substantial, however, it remains lower than the total student loan debt, which has reached $1.77 trillion. Both types of debt pose significant financial challenges for many Americans, especially those who manage both simultaneously.

Credit card debt can be tougher than student loan debt due to its high-interest rates. With average rates around 24.20%, carrying a balance can be costly. It’s like the opposite of a great investment: while earning over 24% is attractive, paying that much in interest is a significant burden.

Yeah, it sucks—but the good news is we’re going to show you how to knock out these high-interest debts and finally get back in control of your money.

First Thing’s First

If you’re carrying credit card debt, there’s a good chance you don’t even know the total amount you owe—and honestly, we get it. That number can be intimidating. But knowing your exact debt is the first step to getting out of it.

Start by making a list of all your credit cards. Write down the balance and interest rate for each one. You’ll need this information to determine the best strategy for paying them off and staying on track.

Next, set up a Monarch Money account if you haven’t already. It’s free to try, easy to use, and great for tracking your spending. You’ll use it to build a budget that shows exactly how much money you can put toward your credit card debt—and where you might be able to cut back so you can pay it off faster. A clear budget is key to staying on track and making real progress.

Monarch Money can also give you a serious boost of motivation. Once your account is set up and your credit cards are linked, you’ll see exactly how much you owe in one clear view. Even better, as you start making payments, you’ll be able to watch those balances shrink over time—which is incredibly satisfying and helps you stay focused on your goal.

Next, head over to Credit Karma and create a free account to check your credit score. Knowing your score is important because some of the strategies we’ll cover for paying off credit card debt depend on having a score above a certain threshold. If your score is lower, don’t worry—there are still smart ways to tackle your debt and speed up your payoff timeline.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

Getting Down to It

Paying off credit cards can feel overwhelming, but it’s totally doable with the right approach. There are a few different strategies you can use, depending on your situation and goals.

Whether you’re dealing with high interest rates, multiple balances, or just trying to get back on track, understanding your options is the first step. Let’s break down some of the most effective ways to tackle your credit card debt.

Ask for Lower Interest Rates

This one’s easy and worth trying—no matter your credit score. Call your credit card companies and ask if they’ll lower your interest rate. Let them know you’re serious about paying down your debt and that a lower rate would help you do it faster. If you’ve been a long-time customer or never missed a payment, mention it. You’re making your case, so don’t be shy.

Also, remind them that plenty of credit card offers are out there. If they don’t budge, tell them you’re thinking about switching to a balance transfer card with a better deal (we’ll talk more about that later).

And if the answer is no? Wait a few days and call again. Different rep, different outcome—call centers are huge, so it’s unlikely you’ll get the same person twice.

Any concession you can get will help you pay off your credit card debt faster.

Get a Debt Consolidation Loan

If your credit score is solid, a debt consolidation loan can be a smart way to knock out credit card debt. You borrow a personal loan from a peer-to-peer lender like Prosper or go with a traditional option like Credible and use that money to pay off your high-interest credit cards.

You’re still paying back a loan, but the big win here is the lower interest rate—meaning less money spent overall. Lenders like Prosper and Earnest let you check your rate in just a couple of minutes, and it won’t ding your credit score.

This move works best if you’ve got a decent credit score and a few thousand dollars or more in credit card debt. Depending on your loan amount, you could pay off all your credit cards at once. Plus, it makes things simpler—you’ll only have one monthly payment instead of juggling multiple due dates and accounts.

Get a Balance Transfer Card

If you’ve got good credit, a balance transfer card can be a game changer. These cards come with a 0% intro APR for a set time—usually between 6 and 21 months. That gives you a window to pay off your debt without racking up interest. You can check out current offers and terms on Credit Karma.

Keep an eye out for balance transfer fees and annual fees. Most transfer fees are around 3% or $5—whichever is higher—not a dealbreaker, but it adds up. Annual fees, on the other hand, can be $100 or more. Some cards waive that fee the first year, but not all do.

Once you’re approved, the new card company handles the transfer from your high-interest cards. During that 0% APR period, every single payment goes straight to your balance instead of toward interest.

But here’s the catch: you’ve got to pay it off before the promo ends. Once it does, the rate jumps—and it could be higher than your original card. Also, don’t put new charges on the card—stick to the payoff plan!

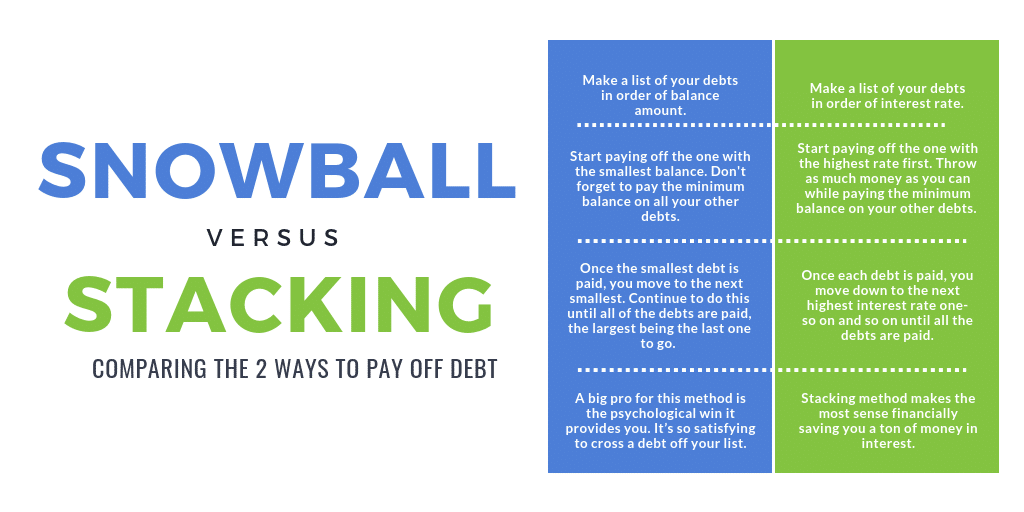

Debt Snowball and Debt Stacking

If your credit score isn’t high enough for a balance transfer or debt consolidation loan—or if you’ve got more debt than those options can handle—don’t worry. You’ve still got solid strategies to work with.

Check out the snowball method or stacking method for paying off debt on your own. Both are proven ways to make real progress, no matter how much you owe or where your credit stands.

Here’s how these two popular debt payoff strategies work—and how to decide which one might fit your situation best.

Grab that list you made earlier with all your credit card balances and interest rates. You’ll need it for both the snowball and stacking methods.

With the debt snowball method, you line up your debts from the smallest balance to the largest. For example:

- Home Depot: $400

- Visa: $1,100

- American Express: $1,500

- Discover: $2,000

You throw every extra dollar at the smallest debt (Home Depot in this case) while making minimum payments on the rest. Once that’s gone, you take all the money you were putting toward it and roll it into the next smallest debt—then keep going until you’re debt-free.

The debt stacking method works the same way, but instead of focusing on balance size, you focus on interest rates—starting with the highest. That same list might now look like this:

- American Express: 21% interest

- Visa: 19% interest

- Home Depot: 16% interest

- Discover: 15% interest

You pay off the highest interest card first, which saves you the most money in the long run.

So which is better? From a pure numbers perspective, stacking wins—it reduces how much you pay in interest. But for many people, the snowball method is more motivating because you see quick wins by knocking out smaller balances first. That sense of progress can keep you going when staying disciplined feels tough.

Make Extra Money

No matter which debt payoff method you use, bringing in extra cash will speed things up. One of the simplest ways? Ask for a raise at your current job. But don’t wing it—go in with a plan. Here’s how to ask for a raise the right way. Even better, consider switching jobs. While the average raise at your current gig might be 3%, a new job—with strong negotiating skills—could land you up to 20% more.

Once your paycheck grows, don’t stop there. Start a side hustle. We’ve shared tons of ideas for making money online or in person. You could drive for Uber or Lyft, babysit or pet sit, or rent out a room on Airbnb. You can also take online surveys, teach English online, or do some freelance writing to earn extra income.

Remember to declutter for cash. Channel your inner Marie Kondo and sell stuff that no longer sparks joy. Use Facebook Marketplace, Nextdoor, eBay, Poshmark, OfferUp, or Craigslist to turn unused items into extra money.

Every extra dollar you make is one step closer to getting out of debt. Whether it’s a raise, side hustle, or selling stuff you don’t need, that money adds up—and it moves you forward.

Find Extra Money

Go through your budget and figure out where your spending leaks are. Food is a common one—whether it’s eating out too often or overspending at the grocery store, most of us can cut back without much pain.

Let Rocket Money help clean up your monthly expenses. It scans your transactions to find recurring charges—like unused subscriptions or memberships—and gives you the option to cancel them with a tap. It’s an easy way to stop wasting money on stuff you don’t even use.

You can also let Billshark negotiate lower rates on your monthly bills. From cable and cell phone plans to internet and home security, they’ll work with your providers to cut costs so you can keep more money in your pocket.

What Now?

Nice work—you made it! You paid off your credit card debt, and that’s no small feat. So what’s next? Now’s the time to use that momentum to level up your finances. Redirect those payments into savings, build an emergency fund, or start investing for the future.

Stay mindful of your spending and use credit strategically so you don’t end up back where you started. You’ve done the hard part—now focus on building long-term financial freedom.

About Those Cards

You might think the next step is to cut up your credit cards and cancel the accounts—but hold off. Canceling credit cards can actually lower your credit score, especially if they’ve been open for a long time or have a high credit limit. And if you’ve worked hard to boost that score, there’s no reason to undo the progress.

Credit cards aren’t the enemy—they’re just tools. When used wisely, they can earn you rewards like cash back or travel points. The key is learning how to use them responsibly. Here’s how to do it right.

If you’re worried about falling back into debt, you don’t need to cancel the cards—just remove the temptation. Cut them up or lock them away, and set up a small recurring charge on each one (like a streaming subscription). Set it to autopay from your bank account. This way, your accounts stay active—which is good for your credit score—but the cards stay out of sight and out of mind.

Start Building Wealth Through Smart Investing

One of the worst parts of being buried in credit card debt is how it keeps you from growing your wealth. Now that you’ve freed up your cash, it’s time to put that money to work. And the most effective way to build long-term wealth? Investing.

If you have access to a 401(k), start by contributing enough to get the full employer match—it’s free money. Then review your plan’s fees with tools like the Empower Fee Analyzer. If the fees are reasonable, consider maxing it out. If not, contribute just enough to get the match, then open an IRA for better control and lower costs.

Both 401(k)s and IRAs are tax-advantaged accounts, which means they help you legally avoid taxes—one of the biggest long-term wealth killers alongside interest. Take full advantage of them to grow your savings more efficiently.

Once you’ve maxed out your retirement accounts, consider investing in a low-cost index fund like

You can also diversify with real estate. If buying a property isn’t realistic, consider platforms like Fundrise, which lets you invest in real estate without needing to own physical property. Another option is Roofstock, if you’re interested in owning rentals but want a more hands-off approach.

You Have No Idea

Credit card debt can feel like a constant weight on your shoulders. It’s overwhelming, stressful, and can mess with your sleep, your mood, and your confidence. But something shifts the moment you pay off that first balance. You start to feel lighter and more in control—and when the last card is finally paid off, that freedom is something you can’t describe until you’ve lived it.

There’s no magic fix to wipe it all away overnight, but the right strategy can get you there faster than you think. Stay focused, stick to the plan, and keep moving forward. You’ve got this—and it’s going to feel amazing when you’re on the other side!