OK, I know, not the sexiest thing in the world. But you know what is seriously unsexy? Besides barbed wire tattoos…

… is paying a shit ton of interest on consumer loans when you don’t even know it.

Unfortunately, without a solid understanding of annual percentage rate (APR), you will do just that! And, like the famous Hill Harper said,

Credit card interest payments are the dumbest money of all!

If you’ve ever applied for an auto loan, a credit card or a mortgage loan, you’ve likely heard the term “APR.”

So, what is APR? This simply stands for annual percentage rate. But there’s more to it than just a simple acronym. A small change in APR can have a dramatic impact on the amount you pay.

It is therefore essential that we all understand exactly what APR is, how it’s calculated, and what a reasonable rate is. Let’s get started!

What is APR?

APR is a percentage that represents the amount you will pay in interest on an annual basis. You can think of APR as the price you pay to borrow the money you need to make a big purchase.

Thinking of APR as a kind of cost for a service allows you more effectively choose between different lenders and loan options.

APRs are like shitty tattoos…

Let’s say you want to pay for your next barbed wire tattoo. You would start by researching different tattoo artists and designs before determining which one is best for you.

Once you know which one you want, it’s a matter of deciding where you will get your ink done.

Obviously, you choose the Pamela Anderson special (hola to my fellow Canadian!).

You could go to Don’t Tell Mama tattoo shop down that dark alley, run by a guy named Harvest Dark. Or, you could pay a little extra and get the professionals at Little Pricks to do your ink.

It’s likely that you will see the price fluctuate depending on where you go.

Even though you want to save as much money as possible, it’s important that you also consider what you’ll get out of the tattoo purchase. Going to Don’t Tell Mama’s will likely be the cheapest option, but it also might leave you with poorer service.

A well-established, local tattoo parlor like Little Pricks is likely to sell the same tattoo at a higher price, but its staff will always be there in the event that something goes wrong. Not to mention the quality difference.

With shitty tattoos, as with APR, you’re not just paying for a product—you’re also paying for the accompanying service. You should keep this in mind when comparing APR offers for loans from various institutions.

While the highest interest rate is not necessarily indicative of the best service. Be open to the possibility that paying a slightly higher APR may prove beneficial down the road.

APRs should not be the only factor you consider when selecting your loan, but it can certainly help rule out lenders that ask for excessive interest rates.

How does APR work?

So, how does APR work? Good question. I had no idea until I started writing this.

After a long chat with my accountant friend Dexter, here is what we came up with.

APR is the annual interest you pay on a loan. Many people believe that APR is consistent and will be consistent from year to year and month to month, but this is not usually the case.

Rather than being a one-time calculation that is then applied to your monthly payments until the loan has been repaid in full, APR is calculated on a daily basis. Which means it should become progressively less expensive as the year progresses.

As your loan principal is paid down, your APR declines.

Compounding interest comes into play with most loans and lines of credit that banks issue. Essentially, compounding interest, aside from being a pad on your principal, is the interest that you pay on your interest.

It might seem like a far-fetched financial magic trick, but charging compound interest is actually a standard practice among financial institutions.

Let’s use an example…

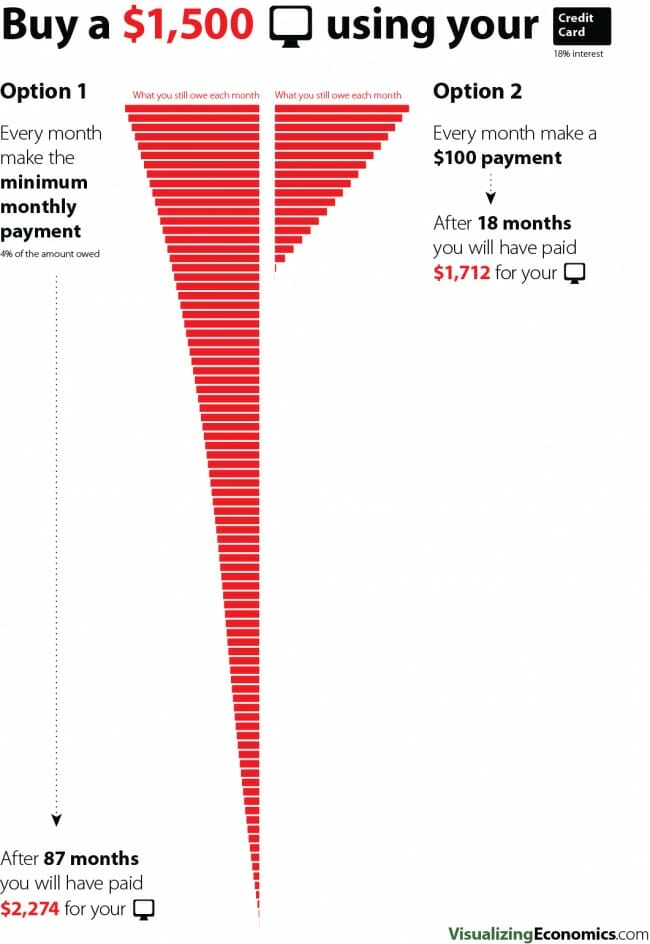

As a practical example, let’s say you take out a $15,000 loan to purchase a car and you must agree to a 6 percent interest rate. If your interest compounds monthly, you will be charged interest at a rate of one-half of 1 percent.

If you don’t pay down your loan principal in the first month, and assuming your interest rate is in effect immediately upon the loan issuance, you will accrue interest in the amount of $75. The next month, your compound interest rate will be calculated based on your new principal, which is $15,075.

After several months of neglected payments, you might be left with a principle that’s far more than the initial value of your loan.

On the bright side, monthly compounding interest makes it possible for you to take advantage of a lower interest rate over time.

The best way to benefit from compound interest—and avoid the negative potential of it—is to make sure that you are fully capable of making the regular monthly payments on your loan.

There are some special situations that apply to APR of which you should be aware. In many cases, credit cards come with conditional APR that’s only applied if you leave a balance on your card after the due date has passed.

By paying off your credit card on time every month, you may be able to avoid APR completely. Be sure to ask your lender about the conditions that apply to APR so that you know what to expect from your loan.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

What is a good APR?

Because APR depends on so many different factors, it can be challenging to pin down an ideal rate. It might seem like a no-brainer that the best-possible APR is zero, but consider some of the other implications of a credit card with 0 percent APR.

At the end of the day, the best way to reduce the interest you pay on high-interest consumer debts is to keep track of your spending.

End of story.

The most important thing to remember is that credit cards are competitive. And, every lender is trying to draw in consumers with a different advertising strategy to make its product more appealing.

If you see a billboard, television commercial, or website that advertises a credit card with an APR of 0 percent, be aware that the deal may be too good to be true.

Banks and lenders always operate in ways that minimize risk and maximize profits. In other words, if a bank offers extremely low fees or interest rates in one area, it’s likely that you will see those costs manifest themselves in other ways.

APR: Considerations for consumers

When you secure a loan with 0 percent APR, you can expect to pay some additional fees that might even exceed what you would have paid with a reasonable APR.

In other cases, 0 percent APR is offered during a promotional period, after which a higher APR is attached to the loan.

If you know that you will be able to pay off your principal before the promotional period expires, it is wise to take advantage of the 0 percent APR. However, jumping on one of these promotional offers can prove devastating if you fail to make payments or meet all the loan requirements.

The APR that is eventually charged may be much higher than the standard rate for a non-promotional loan.

Different APR, Different Card

That said, there are some benchmarks you can use to identify whether the APR on the credit card you are considering is reasonable or not. These include the following:

Travel cards

If you have a credit card for flights or hotels, you can expect a higher interest rate. This is because travel cards tend to have various benefits and rewards—such as discounts on flights and lodging bookings—that make it worth paying a bit more in interest.

Generally, airline credit cards have a slightly higher APR, with an average of 18.09, percent while hotel credit cards are lower, at an average of 17.09 percent.

Business cards

Of all the primary credit card options, business credit cards tend to have the lowest APR. Usually, lenders appeal to business owners’ desire to save money and avoid excessive fees for borrowing.

Advertisements for business cards usually capitalize on low APR. The average APR for business credit cards is 16 percent, but it can often be 13.33 percent or lower.

Cashback cards

Cash back credit cards have an APR rate that can be anywhere from 14.01 percent on the low end to 21.67 percent on the high end.

Make sure that you understand all of the perks of your card to determine if it’s worth it to pay the higher interest rate.

Student credit cards

Lenders who chose to issue a credit card to a student take on an inherently greater level of risk. For this reason, student credit cards may have an APR that’s upwards of 23.33 percent. The average APR for student credit cards is 18.69.

APR vs. Interest Rate

There is much confusion regarding the difference between APR and an interest rate. In a nutshell,

APR is a comprehensive figure that includes your interest rate and any associated charges or fees on your account all rolled into a single, easy-to-digest percentage.

Interest rates, on the other hand, are a singular aspect of a loan that is charged in addition to various other fees.

Considering this distinction, it should come as no surprise that you should focus on the APR when you are looking at the terms of a loan. Seeing the interest rate is helpful to gauge the number of extra charges and fees you’ll be expected to pay.

But, the APR is a much more useful metric when it comes to determining the total amount that you will pay, on top of your loan, on an annual basis.

How to calculate APR

When figuring out how to calculate APR, you’ll need to look at several different factors. To start, you should take your credit score into consideration. The higher your credit score, the more favorable your interest rate will be.

Your bank will take the market standard interest rate for your credit score, and add a margin. This will include their various costs and fees.

What is my daily APR rate?

To figure out what your daily rate is, take the annual APR and divide it by 365. Then, multiply it by the daily principal of your loan. If you have an APR of 19 percent on a $10,000 loan, your daily APR is 0.00052, or $5.20. If you make a $250 payment on your loan, your daily interest will be $5.07.

From here, things can get a little more complicated. There are different kinds of APR terms that will apply depending on changing circumstances. These include the following:

Balance transfer APR

When you transfer an old credit card balance to a new one, a balance transfer APR will be applied. Typically, the balance transfer APR is lower than the regular APR of your credit card.

Purchase APR

The purchase APR is the standard rate on credit cards that will most typically apply to your purchases. This is the APR you will see when you first agree to the terms of your credit card.

Penalty APR

If you cannot make payments on time, you will be charged a penalty APR on your principal. That is, until you get back on track with your payments. In some cases, this APR may be as high as 29.9 percent.

Cash advance APR

If you use your credit card to withdraw money, you will be charged a higher interest rate. This rate is not as high as the penalty rate, but it’s still a good idea to avoid cash withdraws.

So, there you have it: the very sexy basics of annual percentage rates and the various factors that influence them.

Regardless of what the APR on the loan you choose is, you should never rush into a decision. Take your time to research the options. That way, you will thoroughly understand what you’re getting yourself into when it comes to borrowing money.