We all make mistakes, but financial mistakes can be especially costly. These are the biggest financial mistakes people make and how to fix them.

There are some mistakes you can’t fix, but financial mistakes usually don’t fall into that category. It’s not always easy, but most financial mistakes can be rectified.

Joy Liu from The Financial Gym is here to tell us about the biggest financial mistakes she helps her clients fix.

You’re Too Vague

It’s great to have financial goals, but they have to be well-defined. “I want to buy a house” is not a well-defined goal. When do you want to buy a house, in years, in ten years?

How much house can you afford? It’s easy to be seduced by the number you see when you input your numbers into one of those online mortgage calculators. Damn! You could own a whole house for what you’re paying in rent!

But there are a lot of hidden costs in buying and owning a home. You need to factor them in to know how much house you can actually afford.

Will you be able to come up with at least a 20% down payment? If not, you’ll get stuck paying PMI.

If you want to buy a house, understand your real numbers. Once you do that, you can break your goal down into small, manageable steps.

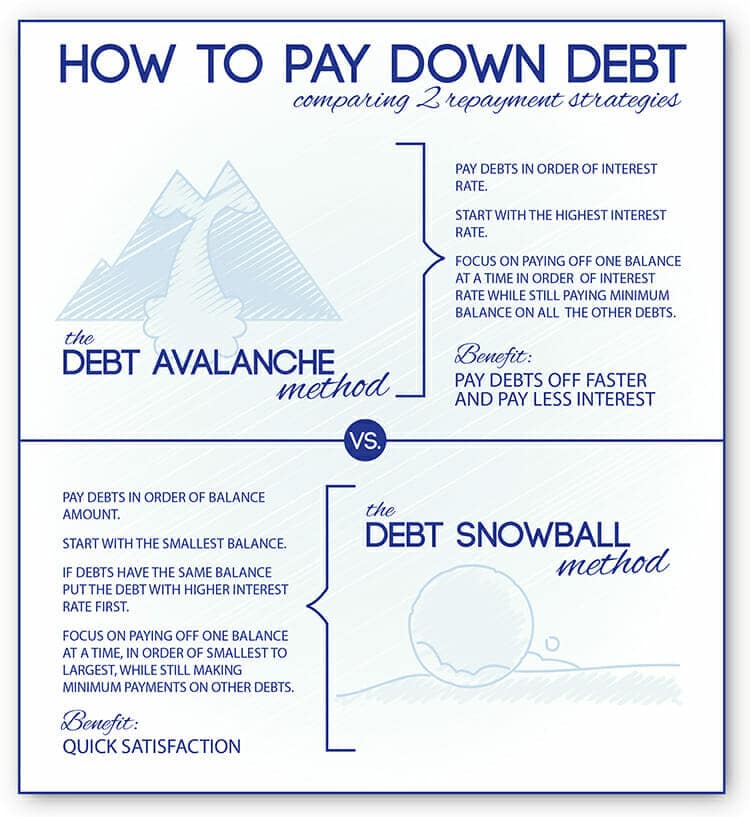

You Have No Debt Plan

If you have debt, especially high-interest debt, like credit card debt, you can’t just ignore it or throw money at it haphazardly. Know the balance and the interest rate on each card. Use the snowball or stacking method to pay the cards off.

We know it’s scary to open your mail when you’re in debt and getting collection notices, but you can’t solve the problem if you don’t know the scope of it. Some of those debts could be relatively small and paid off before they’re sent to collections.

Debt in collections is going to really do a number on your credit score. Open your mail and if you’ve moved, update your address with any company you owe money to.

If you’ve lost your job, call and let your debtors know. It’s in their interest to work with you. They may be able to lower your payments or put your account in forbearance. In the case of student loans, you may be able to get a deferment. Don’t just start missing payments.

Being in debt sucks so it’s understandable you want to pay off as much as you can as fast as you can. But make sure you’re not using money that you need for necessary living expenses like rent and groceries to pay that debt.

All you’ll end up doing is going into more debt because now you have to put those things on the very credit cards you’re trying to pay off. Debt repayment should be a regular budgeting category.

Fiscal flexibility that’s funny, free and delivered weekly.

Too Much Cash

There is such a thing as too much cash if it’s sitting around in your checking or savings account making 0.00001% interest. You might think your money is nice and safe there, but it’s losing value because of inflation.

Historically, the average rate of inflation in the US is around 3%. That means that any long-term saving and investing strategy needs to realistically plan for a return of at least 3% just to keep from losing money.

And while there have been periods when interest rates rose to the point where you could indeed get more than a 3% return on a savings account, these high-interest rate environments usually go hand-in-hand with high inflation rates.

Thus, regardless of the base interest rate you’re getting now, bank savings accounts will rarely if ever allow you to beat inflation, let alone make a reasonable return compared to your other options.

If you have that kind of money in a bank account, you need to put it to work making more money for you. Open a

Not Enough Cash

You look at your IRA balance and feel pretty pleased with yourself; you’re saving for retirement like nobody’s business! Then you’re roof collapses, and you have to pay to have it replaced. But you have no emergency fund.

Water, water everywhere and not a drop to drink. If you don’t have cash set aside for emergencies because you’re shoveling everything into retirement accounts, you’re making a financial mistake. If you have to pull money out of those accounts, you’re going to get hit with all kinds of penalties, fees, and taxes.

By all means, save as much as you can for retirement but make sure you have six months worth of bare-bones living expenses in an emergency fund first.

Do You Want to Work Forever?!

Becuase that’s what you’re going to do if you aren’t saving for retirement. If you don’t have credit card debt and do have an emergency fund, the next thing you need to do is start taking advantage of your employer’s 401k or open an IRA.

In fact, even if you do have debt, contribute just the amount you need to get the company match on the 401k because that is free money, something we never turn down.

Sorry to Tell You

Sometimes you just aren’t making enough money; it’s as simple as that. At some point, there isn’t anything left to cut out of your budget, and you’re still not making ends meet. Or you’re trying to support a family of 4 in San Francisco on $65,000 a year.

Sometimes all you need is a billion dollars.

Tweet ThisYou’re going to have to start a side hustle, ask for a raise, get a new job, or move to a place with a lower cost of living.

Okay, You’ll Go Back to School!

More education doesn’t always translate into more money. If you’re already drowning in student loan debt from undergrad, don’t double down and borrow more for grad school. Or you’re fed up with your current career and want to make a change so you’ll go back to school.

More education is not a bad thing, but it may be an unnecessary thing, or at least going into debt to get it may be unnecessary. There are plenty of ways to get more education or training that don’t cost as much as a degree and some are even free.

See if you can get a higher paying job or a job in a different field without going back to college before you start filling out applications. I’ve never gotten a raise or a job based on what kind of degree I have or where it came from.

Employers want good employees, and that doesn’t always mean the person with the most college degrees.

So You Want a Puppy (Or a baby)

When we see that cute puppy or kitty in the shelter, the last thing we’re thinking of is how much he or she is going to cost us. But you had better think about it. Owning a

I had a kitty who was diabetic, so he had to have special food, more vet visits than a non-diabetic cat requires, insulin, and when I went on vacation, it cost $70 a day to have a sitter come in and give him his twice daily injections. And then there was the $10,000 pancreatitis episode.

A healthy pet costs money, if your kitty or puppy friend gets ill or has a chronic condition, the expenses can run into the thousands every year.

If you think all that sounds expensive, try having a kid. It costs on average, almost a quarter of a million dollars to raise a kid to age 17 so that number, $233,610 to be exact, doesn’t include a college education.

You don’t have to pay it up front of course so you can expect to add an extra $1,000 per month to your current living expenses when you have a kid.

If you want a

Great, You Bought a House!

But you ignored all of the great advice we’ve given you over the years. You chose a house at the very top of your budget, or maybe beyond, you didn’t factor in the hidden costs, you didn’t pay 20% down. And now all of that has come home to roost, and you’re house poor.

All of your money is tied up in a non-liquid asset and even if you did sell it, you have no equity to protect you from a market downturn. You’re underwater; you owe more than your house is worth.

Don’t be in such a tearing hurry to buy a house! Not owning a house is really underrated. Houses not only come with a lot of hidden expenses, but they come with a lot of hidden responsibilities too.

You Bought a Ferrari

That’s Not a Financial Advisor

Did We Miss Any?

This list covers the big ones. Let us know if you’ve made any financial mistakes that we haven’t covered. With five years of shows and articles, it’s bound to be here somewhere!

Show Notes

Tool Box: All the best stuff we use to manage our money.

The Financial Gym: A personal trainer for your money!