- 1. Junk Food

- 2. Gambling

- 3. Singular Goals

- 4. Exercise

- 5. Audio Books

- 6. To-Do List

- 7. Non-Fiction

- 8. Volunteer

- 9. Happy Birthday!

- 10. Write Down your Goals

- 11. Read

- 12. Bite Your Tongue

- 13. Network

- 14. TV

- 15. Reality TV

- 16. Wake Early

- 17. Teach Habits

- 18. Opportunities

- 19. Bad Luck

- 20. Always Be Learning

- 21. Love To Read

- The Rich Are Different

- Show Notes

Rich people are different than you and me. How are they different, though? This list of 21 rich habits will teach you how to become rich and lead you to wealth.

Dave Ramsey published a list of twenty things the rich do every day.

Most of these things are habits. My take on this is that rich people have good habits. Habits that make them more successful, healthier, and smarter. And those things can help you accumulate wealth. Once you have achieved a certain level of wealth, you can focus on yourself rather than on money.

Discipline seems to be the other thing all these qualities have in common. It takes more discipline to cook a healthy meal than to order takeout. It takes more discipline to save money than to spend it. So let’s take a look at each of the twenty-one habits.

1. Junk Food

“70% of the wealthy eat less than 300 junk food calories per day. But, on the other hand, 97% of poor people eat more than 300 junk food calories daily.”

If you don’t feed yourself well, you don’t feel well and can’t think well. And that makes it hard to have the energy and focus on pursuing your goals. Eating well can mean many things: Paleo, vegan, vegetarian, or pescatarian.

Eating poorly is easier to define, and we all know it when we see it. No one thinks a cake is healthier than a carrot.

You can drill down into all sorts of minutia regarding healthy eating, but the basics are pretty, well, essential! Eat a lot of vegetables, and eat a little fruit. Eat plenty of protein and healthy fats. Eliminate refined carbs and keep the slow-burning carbs to a minimum if you’re trying to lose weight. It’s no more complicated than that.

2. Gambling

“23% of wealthy gamble. 52% of poor people gamble.”

People are making less than $13,000 yearly spend 9% of their income on lottery tickets. There is a reason the lottery is called the Fool’s Tax. Of course, there is nothing wrong with buying the occasional lottery ticket for fun or setting aside a certain amount of money you can afford to lose on a trip to Vegas. Still, you will never be rich if you’re spending 9% of your income on gambling.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

3. Singular Goals

“80% of the wealthy are focused on accomplishing some single goal. Only 12% of the poor do this.”

Wealthy people have a goal. And not just a vague goal but a clearly defined purpose and a plan to achieve it. It’s great that you want to quit your job and start your own business, but if you have no plan of action to make that happen, it’s not a goal. It’s just a daydream.

For any goal you have, getting out of debt, saving 50% of your income, or losing 50 pounds, there is a world of information that will show you the steps you need to take to achieve it.

4. Exercise

“76% of wealthy exercise aerobically four days a week. 23% of the poor do this.”

Exercising goes hand in hand with eating well. Regular exercise helps to boost mood and energy. It helps control weight, sleep better, and make sex better. Training is essential for those of us who have sedentary jobs. Sitting all day is terrible for you, and while exercise doesn’t offset it entirely, it would be worse if you were doing no exercise.

Exercise is like a diet; there are no one size fits. The best practice is the one you will do, so find something you enjoy. For example, walking is very underrated as a form of exercise. Almost anyone can do it, and you don’t need special equipment or a gym membership.

5. Audio Books

“63% of wealthy listen to audio books during commute to work vs. 5% of poor people.”

Okay, this one is sort of weird, so we’ll put our spin on it. First, listening to something like an audiobook or a podcast on your way to work is more beneficial than listening to the wacky antics of the 99.5 Morning Zoo.

Listen to something educational (Listen to Money Matters) or something inspirational. The point is to use that time to listen to something that will feed your brain financially rather than listen to morning DJs make prank phone calls.

6. To-Do List

“81% of wealthy maintain a to-do list vs. 19% of poor.”

Always make a to-do list before you go to bed at night. It helps keep intrusive thoughts out of your head. For example, “I need to remember to cancel my dentist appointment. I need to call the bank about that odd charge on my credit card.” You don’t want to lay in bed thinking about stuff like that. Writing it down gets it out of your mind.

Here is a neat trick that works for me. If I know the following day will be rough, I write down even tiny things on my list like, “eat breakfast, drop that letter in the post box.” That way, I get to cross them off my list, giving me a little boost of feeling accomplished. Sounds silly but try it.

I live in Todoist and attribute it to a huge amount of my organization and productivity. It's simple, extremely flexible and has a ton of power features if you really want to get nerdy.

If you're a fan of Getting Things Done (GTD) and don't want to be held down by an inflexible process than Todoist is the project management tool you've been dreaming of. I could not recommend it more highly.

7. Non-Fiction

“63% of wealthy parents make their children read two or more non-fiction books a month vs. 3% of poor.”

I think this goes back to using free time to educate yourself. I prefer non-fiction and always have, but I think there is something to be learned from nearly anything you read, even if it’s just learning a new word. The trick to enjoying non-fiction is to find a subject you’re interested in and dive in. Reading non-fiction often becomes a rabbit hole because one book tends to lead to the next. As long as you’re reading something, I’m happy.

8. Volunteer

“70% of wealthy parents make their children volunteer 10 hours or more a month vs. 3% of poor.”

Ramsey doesn’t elaborate on these, so I had to interpret this. Volunteering is proven to increase happiness. And it’s happiness that didn’t cost anything. That’s a valuable lesson: you don’t have to spend money to be happy.

Volunteering is also an excellent way to make connections that might help you in the future. It can help teach social skills and gives you a sense of purpose. It can also provide you with perspective. No matter how sad you are, you aren’t as low as a puppy in a shelter waiting for a forever home. No matter how big your problems are, they will pale compared to a little kid in the hospital waiting for a kidney transplant. But you helped the puppy, and you helped the little kid by giving your time, and that’s something to feel good about.

9. Happy Birthday!

80% of the wealthy make Happy Birthday calls vs. 11% of the poor.

This one probably has to do with having close social relationships. People who have connections to other people are happier, and when you’re happy, you’re more successful. Remembering the birthdays of those close to you is crucial to fostering relationships. We’ve all had a friend or loved one forget our birthday, which hurts.

10. Write Down your Goals

“67% of wealthy write down their goals vs. 17% of poor.”

It’s proven that if you write down your goals, you are more likely to achieve them. The act of writing things down helps to keep them at the forefront of our minds. Take it a step further and break down your goals into something you can do today, this week, this month, and this year to reach them. For example, how do you eat an elephant? One bite at a time. Writing down each bite makes things more manageable.

If your goal is to save $500 a month, today, you can make coffee at home rather than buy it on the way to the office. For the week, you can bring your lunch to work. For the month, you can become a cord cutter and get rid of cable, research a cheaper phone plan, and sell three items just sitting around your house on eBay. Write down the goals and the steps to get there.

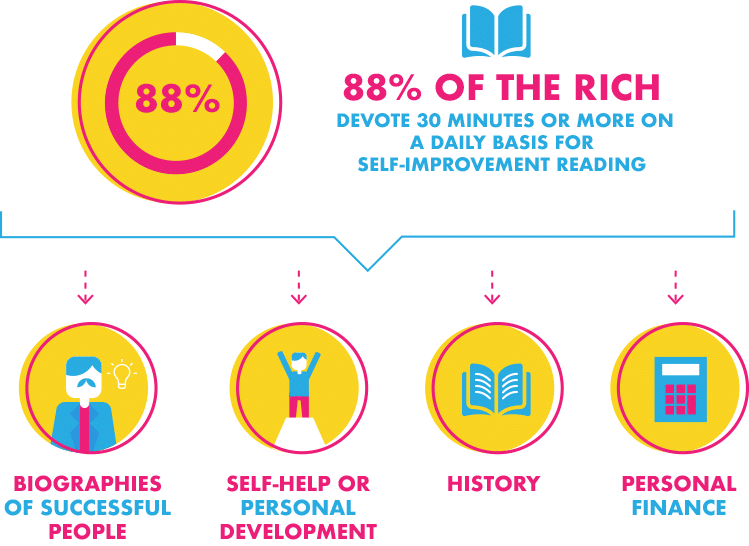

11. Read

“88% of wealthy read 30 minutes or more each day for education or career reasons vs. 2% of poor.”

The reading thing is getting a little repetitive, but the point stands, reading is essential. If you want the most bang for your buck, read a book that will teach you something. Maybe you want to learn to be rich or how to Master Mint.

12. Bite Your Tongue

“6% of wealthy say what’s on their mind vs. 69% of poor.”

Sometimes it pays to bite your tongue. Is Boss being a dick? Don’t call your Boss a dick. Customer making unreasonable demands? Don’t tell the customer to get bent.

It’s essential to pick your battles. Unfortunately, sometimes you have to eat shit. Have you ever had a friend with a temper who was always getting fired? This is likely the reason. They called the Boss a dick and told the customer to get bent.

13. Network

“79% of wealthy network five hours or more each month vs. 16% of poor.”

Wealthy people network. It’s all about who you know. You never know where that next job with a big pay raise will come from. So go to industry events and a Meet Up related to your field. Go to after-work happy hour with your colleagues once in a while. Meet as many people as you can and maintain those connections.

14. TV

“67% of wealthy watch one hour or less of TV daily vs. 23% of poor.”

Watching TV is such a time-sink. Doing almost anything else would be more beneficial. You could read a book, make something healthy for dinner, meet a friend for a drink, run, clean out a closet, or sit and stare quietly at the wall—all the better than watching TV.

I have not watched Breaking Bad, Mad Men, The Wire, Game of Thrones, all of those shows that people talk about at whatever the modern equivalent of the water cooler is.

And not because I don’t think they’re good shows or I might enjoy them. But getting involved in a quality TV show is an investment. If you watched all of those, you would have spent dozens of hours sitting in front of the TV. So never start watching them, and you won’t know what you’re missing.

15. Reality TV

“6% of wealthy watch reality TV vs. 78% of poor.”

I can see why people enjoy the shows I mentioned above. They’re well-written and well-acted. Unfortunately, the same is not true of reality TV. It’s made by stupid people, featuring stupid people, for stupid people. I have no excellent way to say this; frankly, I wouldn’t say it nicely if I could. If you watch this stuff, you’re stupid. Be better.

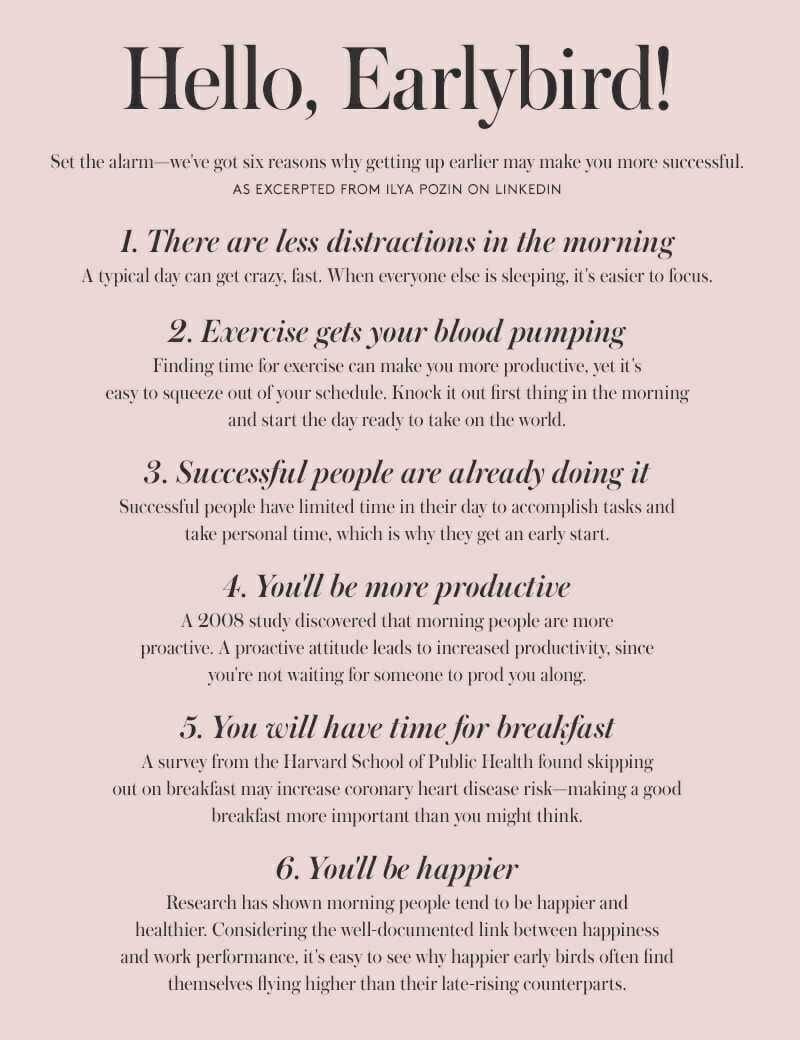

16. Wake Early

“44% of wealthy wake up three hours before work starts vs. 3% of poor.”

I love getting up early. Before 9:00 am, I read the news, had lemon water and coffee, did 90 minutes of exercise, ate a healthy breakfast, and showered. So by 9:00, all of those essential things are done, and I have many hours ahead of me to work.

At the end of some days, I don’t feel like exercising or cooking. So lucky for me, I don’t have to because I’ve already done it.

Those early hours are the quietest for some people too. The family isn’t up yet; there are no co-workers or ringing phones in the office.

Just quiet time you can use to be productive without interruption. Get up a little earlier and claim those hours for yourself. Read, exercise, and make a cooked breakfast. Not starting your day a harried mess will significantly improve the rest.

17. Teach Habits

“74% of wealthy teach good daily success habits to their children vs. 1% of poor.”

I don’t think this one means actively teaching your kids good habits. It’s more about children observing your good habits. That might mean your kids see you brush your teeth every morning before work; they see you make a healthy dinner a few nights a week; they know that they can’t have everything they want because sometimes they are told no.

Some kids get extra lucky, and their parents actively teach them good money habits. And the younger, the better. By age seven, children’s attitudes about money are in place. So it’s essential to model actively good behavior for your kids but go the extra mile and teach them too.

18. Opportunities

“84% of wealthy believe good habits create opportunity luck vs. 4% of poor.”

I’m not sure what language that is, but I think it means that luck is the meeting of opportunity and preparation. So it’s one thing to get a lucky break; it’s another to recognize and be ready to jump on it.

I fell ass-backward into this job, and it was luck. But I was ready when the offer came, and I was able to make the most of it.

19. Bad Luck

“76% of wealthy believe bad habits create detrimental luck vs. 9% of poor.”

Bad habits create bad outcomes. For example, if you have the habit of skipping flossing at the end of the day, you might get gum disease and have to pay for lots of expensive, painful dental work. So bad habits have dire consequences.

Some people don’t believe that, though. When all of their teeth fall out, they rail against the fates, never blaming themselves and their lack of flossing.

20. Always Be Learning

“86% of wealthy believe in lifelong educational self-improvement vs. 5% of poor.”

Some people graduate from high school (barely) and look forward to never having to learn anything again; whoo! No matter what your circumstances, you should never stop learning. There are many ways to learn; not everyone likes to read, fair enough.

Watch some Khan Academy videos, take a cooking class, watch a Ted Talk, and ask a friend to teach you how to change your oil. Then, check out sites like Skillshare and continue exploring.

Learning doesn’t have to be heavy-duty academic subjects. Learning to salsa is learning too!

Skillshare is an online learning community offering thousands of classes from design to marketing to analytics. Discover hidden passions and explore new skills taught by industry leaders. Or, become a teacher, share your expertise, and make money.

21. Love To Read

“86% of wealthy love to read vs. 26% of poor.”

Alright, alright! We get it, Dave, Jebus! Rich people like to read. Roger that. No need to belabor the damn point.

The Rich Are Different

There you are, the rich habits of wealthy people. Of course, the rich are different from you and me because they have better practices and more discipline. But both of those things are available to all of us. Not a single item on this list costs one penny.

Junk food is not cheaper than healthy food; it just takes less time to prepare. You don’t have to join a gym to go for a walk. Volunteering is free, and so is getting up early. Pick three things from this list this week and start doing them. You’ll be rich in no time.

Show Notes

Dave Ramsey: The list of twenty things.

Betterment: Rich people invest.

LMM Community: Join the money revolution.