If you’ve ever heard of using your whole life insurance policy (whole life as opposed to term life insurance) like a savings account to borrow against for personal use, then you’ve heard of the Infinite Banking Concept (IBC) – whether you realized it or not.

The idea behind it advocates becoming your own bank by leveraging your whole life policy for easy access to cash while sidestepping high-interest payments from lenders in the form of loans.

The main point of the IBC is that you lose money to creditors on the various loans you take out over your life. Things like:

- Mortgages

- Car loans

- Credit cards

- College loans

All of the above examples will deplete your wealth over your lifetime in the form of interest payments.

What the IBC advocates is by aggressively saving your money in whole life insurance, you could use that money to fund big-ticket items like a house or college tuition with your policy and not lose money to interest payments. It’s like an interest-free loan.

The argument in favor of the IBC:

- A guaranteed tax-free death benefit

- Tax-free growth, loans, and withdrawals

- Annual dividend payments through your mutual insurance company

In essence ~ Be your own bank.

IBC: A Quick History Lesson

Infinite Banking isn’t a new concept. It’s been around for centuries but the term gained popularity 20 years ago when Nelson Nash coined it in his book: Becoming Your Own Banker: Unlocking the Infinite Banking Concept.

Strategic Self-Banking aka Infinite Banking seeks to treat life insurance as an asset with its prime focus on dividend-paying, whole life insurance.

However, to understand how the IBC works, you need to understand whole life insurance.

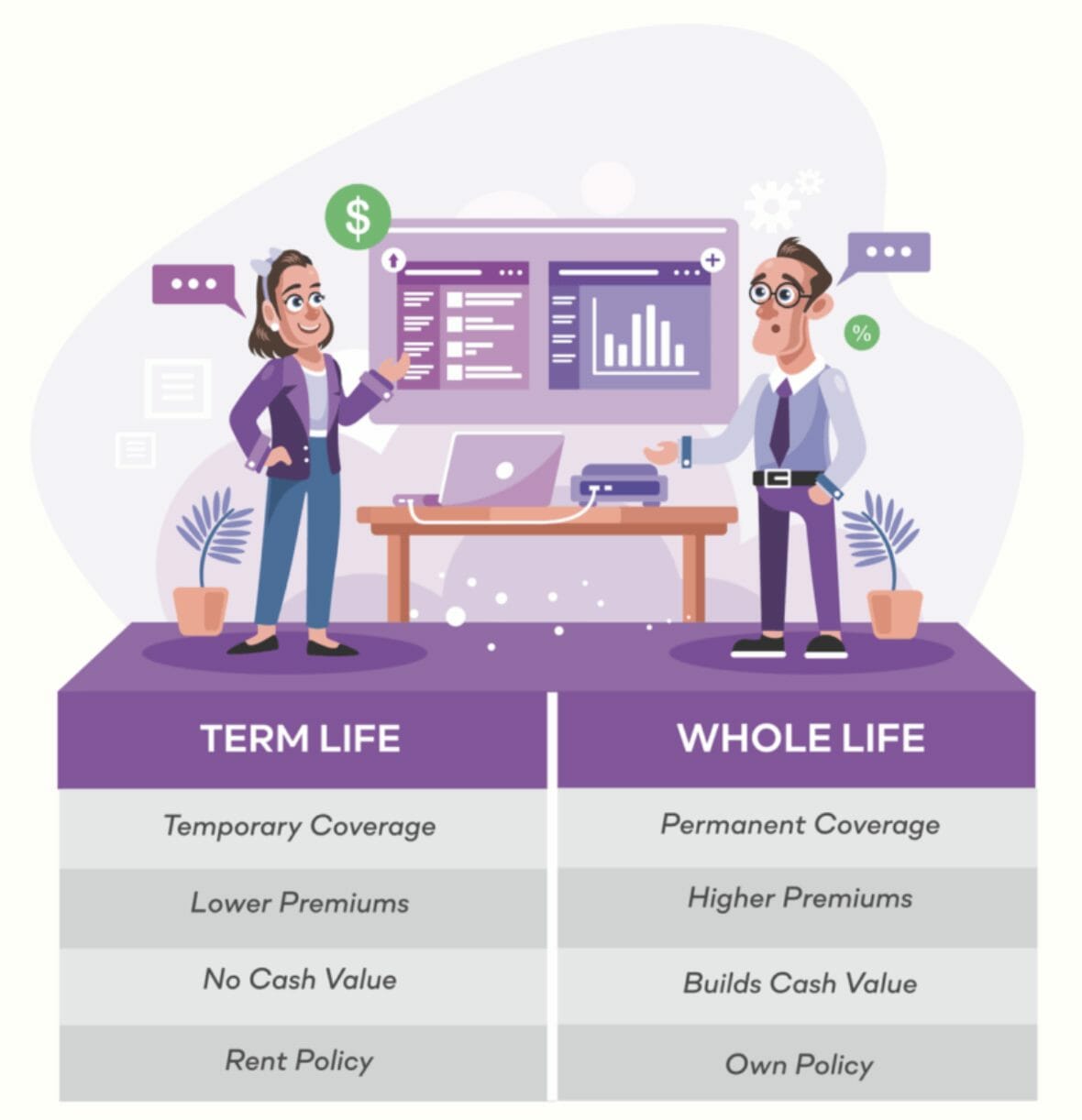

WTF Is Whole Life Insurance?

Whole life insurance is a type of life insurance. It’s a policy that stays in effect until you (the insured) die. Your premiums are fixed and either paid monthly or annually.

Whole life belongs to the cash value category of life insurance and is what you need when putting the IBC into practice. Cash value policies provide coverage alongside an investment account with a portion of your premiums paying into the investment account. It’s a combination of insurance and investing.

What Do Your Premiums Cover?

There are three main components that your premiums pay for:

- Cost of insurance to cover the death benefit (this is separate from the cash value of your policy).

- Fees, overhead, and operational costs. Think of these as the expense ratio of your policy.

- Cash value (the investment account within your policy).

A word about cash value…

Cash value is separate from your death benefit. When you die, the cash value returns to the insurer – not your beneficiaries. It pays for the amount of money you’d receive if you gave up your policy and surrender coverage. It covers the insurer’s ass too.

Cash value takes several years for the money to grow tax-deferred so it’s virtually worthless in the policy’s early years. If you need a loan, you’ll have to wait. Why?

Because the first several years of coverage typically pay for the cost of insurance (your death benefit) and operational costs like fees and overhead.

***The more aggressive you fund your policy in the beginning, the quicker you can start borrowing against it. The amount of time needed depends on your unique situation.

Why Does It Have To Be A Whole Life Insurance Policy?

In a nutshell…

Dividend-paying, whole life policies are operated by mutual life insurance companies with no shareholders. Instead, the policyholders own it.

This means two things:

- When the insurer makes a profit, the insured receives a dividend.

- Dividends are paid out based on the size of your cash value.

You can receive your dividends:

- As cash

- To pay premiums

- To buy more coverage

Life Insurance Policy Loans (Where the IBC Comes Into Play)

When you’re ready to start borrowing against your policy (aka taking out a loan), you get it from your insurer. Your loan comes from the cash value portion of your plan and is used as collateral.

Because the insurer holds the funds to cover your loan means there are no underwriting requirements. You can keep the loan outstanding for as long as you want. This means no hard inquiries against your credit. The loan won’t show on your credit report because it’s all done in-house through your mutual life insurance provider.

***Caveat ~ When you withdraw from your cash value it reduces your death benefit until it’s paid back.

Fiscal flexibility that’s funny, free and delivered weekly.

The Infinite Banking Concept: Steps For Setting Up Your Policy

Setting up your policy requires specific steps to reap the IBC’s benefits. There are many moving, parts and if you set up your plan the wrong way in the beginning, it’s tough to untangle.

Step 1

The first step you’ll need to take is finding the right mutual insurance company. You’ll want to keep your eyes peeled for a company with stellar ratings and has nearly 100 years of reliable dividend payments.

Dividend payments are what let you borrow against your policy.

Step 2

You must make sure your policy is eligible for policy loans. Otherwise, what’s the point?

There are two types of policy loans:

- Direct recognition policy loans

- Non-Direct recognition policy loans

Direct recognition policy loans don’t pay dividends on the money you’re borrowing. For example, if you’ve got a $100,000 cash value and take out a $5,000 loan, you earn dividends only on the remaining $95,000.

Non-direct recognition loans pay you dividends even if you’ve taken out a loan on your policy. Using the above example, when you take out that same $5,000 loan, you’ll earn dividends on the entire $100,000. It’s still fully-funded in the eyes of the mutual life insurance company.

Non-direct recognition policy loans are ideal.

Step 3

Your policy must be a blended, over-funded, high-cash value policy. You construct it using Paid-UP Addition Riders (PUA). Why?

Because you want your policy to have the minimum amount of death benefit and the maximum amount of cash value from day one. Most life insurance policies not using the IBC do the opposite by using the maximum amount of death benefit and the minimum cash value amount.

The PUA riders add cash value to your policy immediately.

Let me explain…

Blended policies contain minimum whole life insurance and the maximum amount of paid-up level term insurance known as the “Paid-up Additions Rider.”

Paid-up insurance instantly adds cash value because you’ve purchased full death benefit insurance all at once.

For example, a regular whole life policy will take at least a decade before there’s any cash value in the account. However, when using the IBC and PUA riders, you pay more money up front as a way to augment your cash value for personal banking (IBC).

If you throw in an extra $10,000 or $20,000 up front, you’ll have that money to the bank with from the beginning.

***Caveat – You must be mindful when funding your policy. If you contribute too much too soon, it loses its tax-free benefits. The IRS no longer views it as a life insurance policy. Instead, it’s seen as an investment and called a Modified Endowment Contract (MEC).

Ideally, you’d contribute to your policy’s cash value until reaching the MEC limit. It increases your policy’s cash value ASAP in the shortest amount of time

Borrowing money against your policy’s cash value lets you take out a loan while your remaining funds earn dividends.

However, there’s typically a 7-10 year gap where your returns will be negative at the start. You’ve got to wait it out before any real value begins compounding in your policy.

IBC Is Conservative Growth

You’re not going to generate colossal returns using the IBC. Your money will grow similar to the way fixed-income assets like bonds do. You’re aggressively funding your policy for moderate returns of ~4.5%.

You aren’t getting rich with moderate returns. Instead, folks in favor of using the IBC think of it like having your own ultra high-yield savings account equipped with tax-free growth and interest-free loans.

Additional Set-Up Costs

In addition to the steps above, you’re also required to get a physical exam and blood screening. You must be deemed insurable. Imagine having to do that setting up an IRA! It can take up to two months until you’re approved or denied upon exam completion. You also need to find an agent who specializes in the IBC.

There are thousands of insurance companies, but only a small number offer the riders and terms that maximize the IBC. Some companies will let you bypass the physical exam, but you’ll pay a higher monthly premium for it.

How Much Do You Need To Start?

The younger you start, the lower your premium. Pricing for this is tricky as no two insurance companies are identical. You’ll want to do your homework.

Let’s say you’re a healthy 25-year-old male and want to take out a $1M policy. You’d pay $688 a month for the rest of your life. If you start a plan when you’re 30, it’s $827 a month (~$10k annually) and keeps getting higher the older you are when you start.

Think of the dividend-paying portion of your policy as the cash-value in a savings account.

What Amount of Your Personal Bank Belongs To You?

Your personal bank is determined by the cash value of your insurance plan. Most whole life insurance policies generate a return of ~4.5%. You can borrow against your policy, but you shouldn’t dip beneath its cash value.

For example, if your cash value were $100K, you wouldn’t borrow more than that amount.

One of the arguments in favor of using your policy as opposed to a regular bank to borrow against is the higher velocity of money you’ll have. Banks use other people’s money, but with the IBC, it’s your own money.

Also, when using non-direct recognition policy loans (Step 2 in setting up your policy), the money you’ve taken out still earns dividends as if it’s still in your account.

Pros

There’s potential to reap some sweet tax benefits that could be worth it when considering your time horizon. The longer, the better. The minimum ~4.5% dividend you’d earn from your policy is tax-free as are loans and withdrawals.

The IBC isn’t tied to the stock market. Whether the stock market is up or down doesn’t affect the dividends you earn.

The guaranteed, tax-free death benefit for your loved ones provides peace-of-mind.

Also, there are no credit checks when taking out a loan and you’re paying nearly 0% interest.

Cons

Fiduciary Vs. Salesman

RED FLAG #1

Life insurance agents (the folks selling you these policies) aren’t fiduciaries. They’re salespeople who earn money off commissions. It’s in their best interest to sell you an expensive policy because they’ll make more money.

There’s a conflict of interest when the person selling you something is commission-based. You must know precisely what you’re setting up to use the IBC; otherwise, you might end up getting taken for a ride.

RED FLAG #2

Nelson Nash, the guy who coined the term Infinite Banking and author of Becoming Your Own Banker in the ‘80s, said in his book he made a fortune and tripled his income selling whole life policies with the IBC.

If using the IBC as your only financial vehicle, 100% of your money is tied to your life insurance policy. This breaks the first law of investing 101 – diversify.

Setting up a policy is expensive. I can’t imagine someone earning $50,000 a year shoveling $10,000 of their income into whole life.

Proceed with caution.

Final Thoughts

There are some legitimate reasons for someone wanting to add this as an additional layer to their portfolio. Tax-free growth and virtually 0% loan interest-rates are music to my ears.

However, I wouldn’t suggest the IBC as your financial foundation. It might make sense for more affluent individuals looking to seize some serious tax breaks. If I were on a tight budget, I couldn’t justify paying $800 a month in premiums.

Also, I’m turned off by the complexity of it all. If I can’t explain it to a five-year-old, then it’s probably not worth it.

Remember Occam’s Razor?

Simpler solutions are more likely to be correct than complex ones.

Sounds like a marketing gimmick on the part of Nelson Nash. He just branded it ‘infinite banking.’ Who wouldn’t want to be their own banker? He did say his income increased when he started selling whole life policies with the IBC as a strategy.

It’s like what Dave Asprey did with the Bulletproof Diet (not knocking you Dave. You’re doing great things!) It’s essentially the ketogenic diet only rebranded with a cool name. Who wouldn’t want to be bulletproof?

But the most important question to ask is:

Would you feel comfortable recommending this to your mom?

I wouldn’t.

Show Notes

https://www.ommegang.com/beers/game-of-thrones/

https://infinitebanking.org/about/

https://www.whitecoatinvestor.com/a-twist-on-whole-life-insurance/

https://www.whitecoatinvestor.com/debunking-the-myths-of-whole-life-insurance/

https://www.investopedia.com/terms/w/wholelife.asp

https://www.insuranceandestates.com/pros-and-cons-of-the-infinite-banking-concept/