There is no question Dave Ramsey has helped people take control of their money. We wanted to see for ourselves how useful his financial advice is so we review his best selling book Total Money Makeover.

The book easily breaks down a no-BS approach to money matters. He teaches how to lay the groundwork for a healthy financial fitness. From getting out of crushing debt to easy ways to invest in your retirement.

Introduction

In the intro to TMM, Ramsey talks about the success stories, how changing your behavior is key, and how this sure fire plan can work for anyone if they follow it closely. He also tells you what the book is not; complicated, anything new, politically correct, the same as his other books (so he thinks you should buy those too), or wrong.

Pros

Dave believes that personal finance and most other things in life, is 80% behavior and 20% knowledge. Agreed, the vast majority of America knows what we should be doing with our money, actually doing it is another story.

The book explains that what it’s teaching you is nothing new, secret, or revolutionary. Also true, saving money is like losing weight. The principles are very similar, we all know to have more money you must make more than you spend.

To lose weight, you must eat fewer calories than you burn. The money/weight loss analogy is touched on throughout the book and it’s a good one. But just because those things are simple, that doesn’t mean they’re easy and the book acknowledges that.

The Total Money Makeover system is designed to work in good times and bad weather those good and bad times are personal for you or happening to the economy as a whole. We agree with this too, a good plan shouldn’t need to change due to external factors.

Ramsey does a nice job of explaining the 2008 economic collapse in a way that is easy to understand.

Cons

This book does not contain a ton of the heavy-handed Christian bible dogma that Ramsey is famous for. But it is in there, so depending on your personal tolerance for that sort of thing, it might bother you or it might not.

Ramsey does warn you that it’s in the book and acknowledges that not everyone will like it.

There are some pretty corny analogies in the intro, stuff about flying turkeys and skinny dipping. They went on at some length.

Chapter One: The TMM Challenge

Chapter One tells a little about Ramsey’s personal financial problems. He challenges the reader to acknowledge they are the problem and introduces the TMM Motto. It’s a proven plan as long as you if you follow the guidelines.

Pros

We are the problem with our money and that is true. It’s rare that people are ruined financially through no fault of their own, it happens but it doesn’t happen a lot. If you’re in financial trouble, you most likely put yourself there.

The Total Money Makeover Motto is, “If you can live like no one else, later you can live like no one else.” Huh? I get what he’s trying to say but Adam Carroll said it better on one of our past member’s only podcasts

“If you are willing to do for two years what won’t most people won’t do, you can do for the rest of your life what most people can’t do.”

It means if you sacrifice and suffer for a relatively small amount of time, you can be set for the rest of your life. Live with your parents for two years after college while working full time and saving 80% of your income and you will be ahead for life. Take everything step by step.

Cons

Ramsey started his whole empire because of his own financial disasters.

He doesn’t give a lot of details about what they were. He tells how he felt and how his family has affected but not many nitty-gritty details of what exactly happened. It’s not really our business but it seems like an odd omission.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Chapter Two: Denial: I’m Not That Out of Shape

Chapter Two is about denying how bad your financial situation is and how so many people won’t make changes until they are backed into a corner and that change is more painful than the corner.

Pros

I like the fitness/money analogy and Ramsey points out that it’s much easier to be in denial about your financial situation than your weight. If you’re overweight, you know it and everyone who sees you knows it too because you can’t hide it.

Money trouble is easier to hide. You can dress well, live in an expensive home, and drive a fancy car and be broke as shit.

No one will ever know. This is why it can be so hard to acknowledge that you’re in financial trouble.

Until the day the house gets foreclosed on and the car gets repossessed. Then everyone will know, even you.

Cons

The book uses a really gross analogy about dirty diapers that I could have done without. I’m also two chapters in and the book hasn’t told me what I’m supposed to be doing yet. I get it that people need to understand why they are where they are but two chapters of it feel like belaboring the point.

Chapter Three: Debt Myths: Debt Is (Not) a Tool

Chapter Three explores what Ramsey considers to be myths about debt.

Pros

Learn to distinguish wants from needs and to delay gratification. These are good points and not being able to do so is what gets lots of people in financial trouble, especially credit card trouble.

Ramsey believes that the thought of debt as normal is ingrained in American culture, it’s true. If you know someone without some type of debt, they are certainly the exception and not the norm.

Ramsey does not believe debt should be used to leverage wealth ever. For those who are not financially sophisticated, I agree.

Ramsey warns readers away from things like cash advances and rent-to-own. This is something his audience needs to hear because many of them have probably gotten caught in these traps.

The book advocates never buying a new car and instead of paying cash for a reliable used car.

The book is against debt consolidation because it doesn’t treat the underlying problem of uncontrolled spending. While debt consolidation can be a good thing, it’s correct that if you don’t understand why you had to get a consolidation in the first place, you will continue to repeat the same mistakes.

Borrowing more than your home is worth in order to restructure debt is a no-no. This is true, again, if you are not addressing the problems that caused the need to borrow more money.

Cons

The book talks about people who adhere to the no debt principle being ridiculed by family and friends. I find this hard to believe. If you tell people you are debt free, I doubt they will shun you.

This book is geared towards people who are largely unsophisticated about money and who have gotten into trouble with debt in the past. But that isn’t everyone and there are people who leverage debt to build wealth.

TMM goes on at length about how it’s a myth that making loans to or co-signing for family and friends is a good idea because you’re helping someone. I don’t think anyone thinks these things are a good idea so that’s not really a myth in need of busting.

Ramsey considers needing a credit card to build credit a money myth. He thinks having a credit card means having debt and for some people, it does mean that. But there are people who use credit cards responsibly and used that way, they are a good tool to build your credit.

Another money myth he wants to bust is that you need a credit card to rent a car, a hotel room and to make online purchases. He says a debit card allows you to do those things.

True for buying online but I know it’s not true for renting a car and a hotel.I’ve done both recently and I indeed, needed a credit card.

Ramsey believes using a debit card is just as safe as a credit card. Also not true. I have had my debit card hacked and while I did get the money back, it took a few days and a lot of back and forth with the bank.

I’ve had my credit card hacked too and all I had to do was make a single call to the credit card company and they took care of the rest. Had I needed the cash taken out of my checking account immediately, I would have been out of luck.

Ramsey writes that it’s a myth that if you pay your credit card off each month, you are getting free use of someone else’s money. His counter is that 60% of people don’t pay it off each month. Well, that’s true but it has nothing to do with his first statement does it?

Ramsey claims that getting a credit card for your teen is a bad way to teach them how to use credit responsibly. I think it’s better than what a lot of young people do which is to get their first card when they leave home and go hog wild.

Had I still lived at home instead of on my own at college when I got my first card, my parents could have monitored my spending.

Chapter Four: The (Non) Secrets of the Rich

Chapter Four reiterates that they are no get-rich-quick secrets the rich know that the rest of us don’t.

Pros

There are no shortcuts, you are not going to win the lottery, you are not going to be fine in retirement if you have no money saved, even if you get Social Security, it won’t be enough to live on. Gold is not a good investment.

Attending a seminar (except Ramsey’s I guess), buying DVD’s about getting rich on the no-money-down real estate is not a wealth building strategy, you will not get rich working just three hours a week.

I like that Ramsey is debunking some of the stuff desperate people turn to when they’re having money problems.

He also advocates the envelope system which I think is a good one and a legitimate reason to use cash if you have trouble seeing credit cards as real money.

When the “food” envelope is empty of cash, you’re done spending money on food for the week but there is no such built in restraint when using a credit card.

The book reinforces the importance of having various types of insurance, auto and home, health, etc and that’s true. The majority of bankruptcy cases now are due to medical bills.

Cons

Ramsey seems to think the reason a lot of people don’t use cash is that they’re afraid of being robbed! I live in NYC where that might be true but it was never the reason I didn’t use cash. Weird!

This one was weird too. “If I write a will, I’ll die.” According to Dave, you will die with a will or without one. He didn’t back up this wild claim though so don’t be so sure.

Chapter Five: Ignorance and Keeping Up with the Joneses

Chapter Five is about educating yourself and not succumbing to FOMO. (He calls is Keeping Up with the Joneses cuz he’s old.)

Pros

Ramsey advocates educating yourself on the basics of personal finance. We agree 100%, that is the entire reason LMM exists!

He also cautions against judging yourself by what other people have, or seem to have, because unless you are privy to their finances, you don’t know if all those fancy things they buy are paid in cash and they have a robust retirement account or if they’re one missed paycheck away from losing it all.

Cons

None! This was my favorite chapter of the entire book.

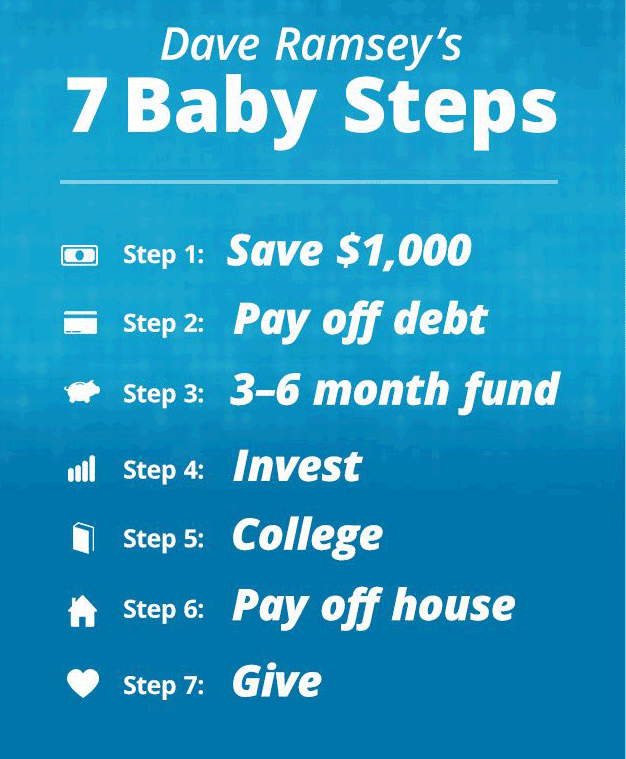

Chapter Six: $1000 Fast, Walk Before You Run

Chapter Six is the first actionable step in the plan, save $1000 for an emergency fund.

Pros

I like the opening of this chapter. It talks about breaking things down into baby steps so you don’t get overwhelmed and give up. That’s important for any goal. It also talks about focus, that you will concentrate on each step to the exclusion of everything else so you can get it done and move onto the next thing.

The importance of having goals and writing them down is discussed. I like the emphasis on writing down goals. It’s proven that this simple act increases the odds of the goals being achieved.

Having a budget is discussed and a zero-based budget is recommended. I agree, this kind of budget gives every dollar a job and is more hands on than other types of budgeting systems which is good for people who have had money problems in the past.

Ramsey emphasizes getting your partner on board with the budget. No budget will work if everyone is not in agreement.

Another step in the chapter is getting current with all creditors. Doing this step is hard and scary but it does take a massive weight off your shoulders if you have late payments.

The big push of the chapter is to do whatever you have to do to accumulate $1000 for an emergency fund and fast. We’ve talked over and over about the importance of having an emergency fund. $1000 might not sound like much compared to six months of expenses but for people in dire situations, this is a big deal and a big win when they manage it. Having that cushion, which some people may never have had before, can feel like a big security blanket.

Cons

Again, none. Having an emergency fund is one of the most important aspects of personal finance. It is also the first step in his 7 Baby Steps.

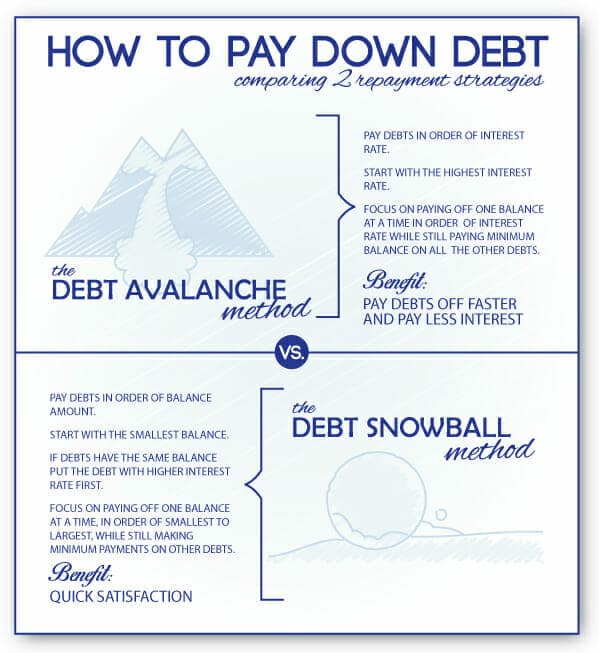

Chapter Seven: The Debt Snowball

Getting down to brass tacks now, tackling debt. You can’t possibly do that by making minimum payments only. Ramsey has taken a lot of flack for pushing the snowball method, including from us. Does he deserve it or does he redeem himself?

Pros

Ramsey makes no bones, this part of the plan is hard and it sucks. You will have to sacrifice and live very austerely to kill your debt. He promises it will be worth it and that’s hard to argue with.

There are two established methods to pay off debt. Snowball which means you throw every extra penny at the smallest dollar amount debt first while paying only the minimums on the others and when it’s paid, roll that payment into the next and so on until all the debt is paid.

The other method is the stack which means you do the same as above but you pay the debts off in order of highest interest rate, not dollar amount.

Surprise! I’m not going to trash the snowball method of paying debt. Yes it saves money on interest to use the stack method but you can pay off the small debts faster and getting rid of even small debts is a big psychological boost.

And that boost is no small thing for anyone, never mind someone who has been drowning in debt for years.

Here comes the hard part; if you have something like a car,

He does not advocate selling your primary residence in this case though unless the mortgage payment is more than 45% of your income. And even then, there are some arguments that you should still stay put.

You need to bring in more income during the debt payoff phase. Get a second job, start a side hustle, work overtime, whatever you can do to speed up the process.

Ramsey recommends you stop contributing to retirement accounts during this phase, even if you get matching, and I was ready to pounce.

Matching is free money Dave! But he does say that if you are in a very deep hole that will take a long time to get out of, you should keep contributing.

I like that the book advises you to stop debt repayment if you need to replenish your $1000 emergency fund. And by this point of the book, you will know what constitutes a real emergency. I liked this because I know how comforting that $1000 can be for people. Once it’s back to $1000, it’s right back to debt repayment.

Cons

Another long ass analogy about cheetahs and gazelles. I like a good analogy as much as the next personal finance writer but Ramsey’s drag on and it feels like cheap filler.

I’m ambivalent about this con, some of you may be too. Ramsey says that all money should be held jointly with your spouse, no his and hers money. His reason is that if you can’t trust your spouse, you shouldn’t be married.

Well, that’s very romantic and in an ideal world, we could all trust our spouses never to develop a drug or gambling habit or have a mid-life crisis and run off with the pool boy and bank accounts. Me, I’ll hedge my bets and keep some money to myself.

Chapter Eight: Finish the Emergency Fund

By Chapter Eight, your debt will be paid and you are ready to move on to the next step.

Pros

Now that you are debt free, you are going to grow your emergency fund to cover 3-6 months of expenses. That’s the gold standard and what we recommend too.

So many people are obsessed with buying a home. It’s not always a good thing for everyone, for financial reasons and sometimes other reasons too. Ramsey wants you to buy a home but not while you’re paying off debt and not before you have fully funded your emergency account.

Cons

Ramsey wants your emergency fund liquid. He recommends a money market account. That will give you the princely sum of 1% interest. I’ve taken shit for this before so I’ll take it again because I’m right. A low-interest-bearing account is fine for a $1000 emergency fund, it sucks for a $25,000 emergency fund. You are not going to need all of that money at once so keeping it somewhere like

Chapter Nine: Maximize Retirement Investing

Chapter Nine is the next step in the plan, funding your long-neglected retirement accounts.

Pros

I like what Ramsey tells us retirement is not meant to be; quitting a job you hate. If you hate your job, find something else to do. It’s one thing if you hate your job and are two years from retirement. You can probably just suck it up and hang in there. It’s a different story to hate your job for thirty years.

The book wants you to save 15% of your gross income to your retirement accounts. That’s a good number to shoot for, it could be higher but we’ll get to that in the con.

Cons

Ramsey doesn’t recommend investing more than 15% because he wants you to throw extra money at paying off your mortgage and saving for your kid’s college fund. Not bad things but we don’t agree with the dogmatic way he advocates paying off your mortgage like it’s the holy grail of personal finance because he thinks debt is literally the devil.

Ramsey is also known for his conservative approach to investing. At this stage he only wants you to invest in mutual funds and Roth IRA’s. That’s fine for those who are not very sophisticated when it comes to investing but there is a much bigger world out there.

Chapter Ten: College Funding

Have some kiddos? This is how TMM wants you to pay for their education.

Pros

I loved the quote in this chapter, “The most useless part of your degree is its pedigree.” He points out that most of us don’t ask our doctor where they got their medical degree and that’s true. Going to an expensive college on loans because it’s prestigious is a good way to spend the rest of your life in debt.

Total Money Makeover recommends ESA’s (educational savings account) and 529 Plans to pay for college. If you don’t have a lot of time before your kid goes to college, Ramsey suggests things like working during college on a work study program or joining the military.

Cons

Because Ramsey is so anti-debt, he is 100% against student loans. That’s just not realistic for everyone. He apparently thinks paying cash is well within reach of the majority of people so he doesn’t offer a lot of alternatives. LMM has your covered where Dave falls short.

Chapter Eleven: Pay Off the Home Mortgage

Chapter Eleven is the top of the mountain according to TMM, paying off your mortgage.

Pros

For those who have never known anything but debt, having no mortgage probably does feel like the promised land. For people like that, it’s a good thing.

The book points out that you can buy a home for cash if you are not buying a very expensive house. I like the idea that you don’t have to buy a $500,000 house, there are houses out there for much, much less.

Cons

Again, this advice is for people not very sophisticated in personal finance. In some cases, debt is not a terrible thing and buying a house can be one of those cases.

Not everyone lives in flyover country where houses can be scooped up cheap and it’s not impossible to pay cash. But some of us don’t like corn and void. We like cities and urban housing is expensive so paying cash is never going to be a realistic option for those of us not in the 1% but that shouldn’t exclude us from home ownership.

Chapter Twelve: Building Wealth Like Crazy

Chapter Twelve tells us what money is for when it’s not needed to pay off debt and save for retirement.

Pros

You get to have some fun with your money! You’ve earned it and money should give pleasure and not just anxiety.

The book encourages giving and I was ready to read whatever percentage grasping religions think they are entitled to off the back of your hard work but there were some touching stories about people giving away money.

Cons

You aren’t allowed to go off the reservation of Ramsey’s conservative investments until you have $10million. I’m skeptical about the ability of Suze Orman’s followers to reach those hallowed halls, never mind Ramsey’s acolytes.

Ramsey advocates always having the final say over your money but he does encourage having advisors. We do not. No one will ever care more about your money than you and they aren’t going to do for pay anything you can’t do yourself for free.

Chapter Thirteen: Live Like No One Else

Chapter thirteen is your pat on the back for a job well done and a caution.

Pros

Stuff does not make us happy. Absolutely true and lots of science to back us up.

I also like the section about wealth enhancing what you always were; if you were a jerk when you were poor, you’ll be a jerk when you are rich. If you were generous when you were poor, you will be generous when you are rich.

Cons

Lots of religious mumbo jumbo.

Overall Thoughts

I’ll admit I came to this book expecting not to agree with it or find it useful. I was wrong. I had my disagreements but overall, I think this book is helpful. That said, it’s most helpful to people who are in a lot of trouble and not savvy when it comes to money.

The book is peppered with testimonials of people who have used the system successfully and found financial pice. That can be encouraging. I think the book could have been cut by about 25% and perhaps been more impactful. It took a few chapters before I was given any actionable financial advice.

But the advice is easy to understand and if not easy to follow, it is simple to do. So I take back some, but not all, of what I’ve said about Dave Ramsey and his system. He is helping people and I guess at the end of the day, that’s what we have to judge any personal finance tool on.

Want to dive deeper into Dave’s game plan? Get The Total Money Makeover Workbook. And if you are looking for something a bit deeper you can join Financial Peace University, Financial Peace University Dave’s nine-week course on money management, will walk you through the 7 Baby Steps in detail and help you put them to work.

Show Notes

Pumpking Imperial: The perfect fall beer.

LMM Toolbox: Everything you need to manage your money.