Buying a home is still the American dream for many people but with home prices going up and up, how can you save up for a house without sleeping in your car? With the median home price in the U.S. at $387,600, it seems impossible. How the hell does someone save up for a house?

It’s the American Dream

Buying a home is such a part of the American dream. It seems like once you reach certain milestones that are considered part and parcel of being an adult, every which way you turn, someone or something is telling you to buy a house, you must buy a house! But should buying a home still be a part of the American dream?

The dream of home ownership was something that came after World War II when everyone came back and they built all these houses. Homes came to represent personal success and security, an ideal real estate and mortgage agents perpetuated.

It’s good for the economy to buy houses, but that doesn’t mean it’s actually good for the person that buys it.

According to S&P CoreLogic Case-Shiller, home prices in Boulder, Colorado are up roughly 72.3% from 2012 to 2022 and up around 67.5% in Hoboken, New Jersey for the same period. With so many people struggling with credit card, student loan, and medical debt, how does anyone save up the 20% down payment?

Is buying a home still a good idea and if it is how can you save for a house?

Personal Capital is Now Empower - Track your entire portfolio for free.

All your accounts in one place

- Plan for retirement

- Monitor your investments

- Uncover hidden fees

Do You Really Need 20% Down?

You can certainly buy a home with less than 20% down. Through an FHA loan, you can do it with just 3.5% down. But should you buy a home if you don’t have 20% for the downpayment?

No, you shouldn’t. Without 20%, you’re going to be stuck paying PMI, primary mortgage insurance. PMI typically costs from 0.5%-1% of the original mortgage amount. You can use this PMI calculator to estimate the total cost.

You can ask your lender to remove PMI when the mortgage has been paid down to 80% of your home’s original appraisal value, and once the mortgage balance is down to 78%, the lender is required to remove PMI.

PMI isn’t the only reason at least 20% down is ideal. A bigger down payment means a smaller monthly payment and paying less interest over the life of the loan so putting 20% down saves you money in the long run.

There is a workaround though, and it’s called a piggyback loan. Your first mortgage is for 80% of the cost of the home, a down payment of just 10% is made, and the remaining 10% comes from a second mortgage loan that comes with a higher rate of interest. This strategy allows a buyer to avoid PMI.

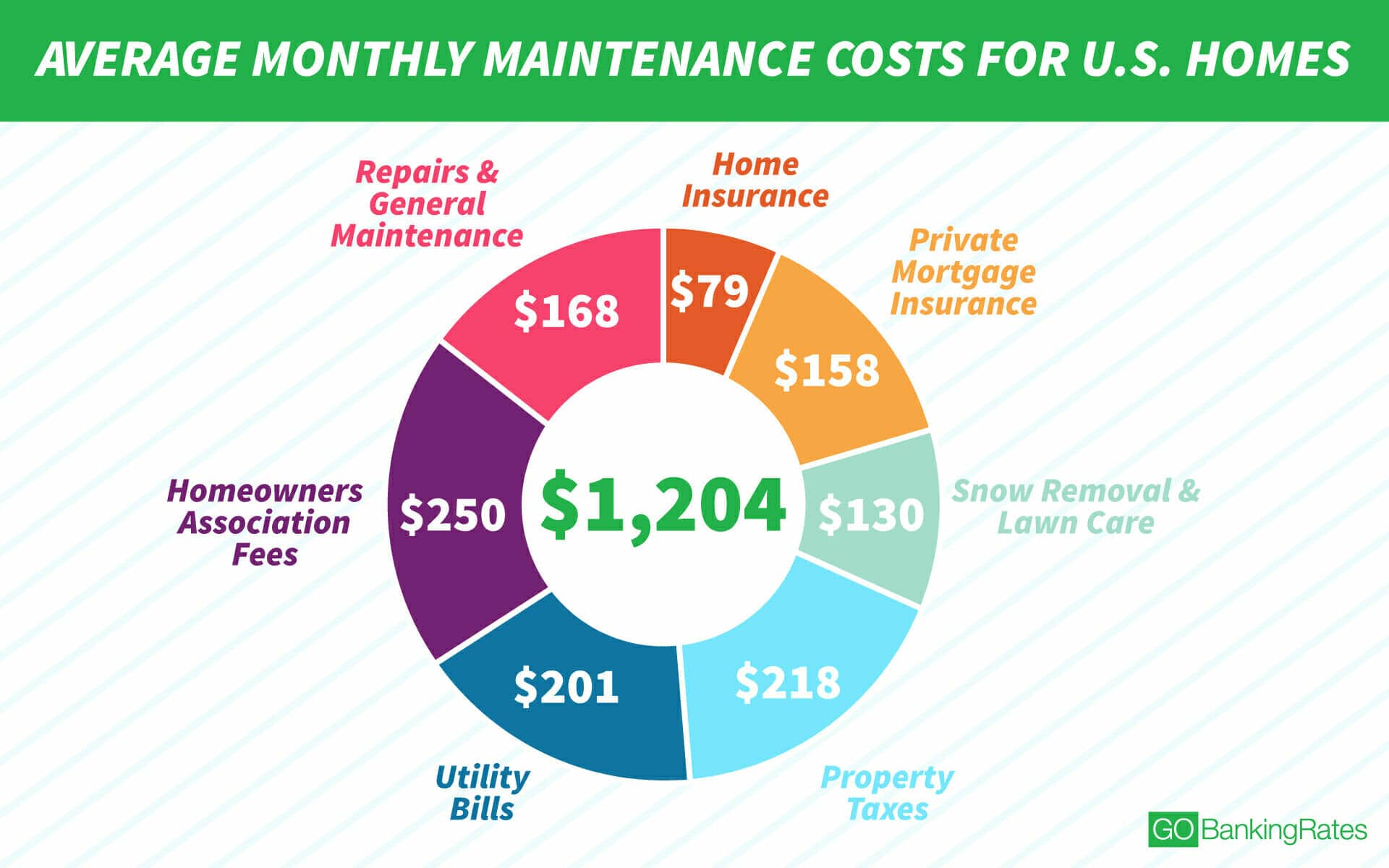

Hidden Costs of Buying and Owning a Home

However, the down payment isn’t the only financial consideration. Often, people input their details into a mortgage calculator and discover that monthly payments for a home could be comparable to, or sometimes even lower than, what they currently pay for rent.

Mortgage calculators don’t tell the whole story though. There are a lot of hidden costs in buying and owning a home. Inspection costs, closing costs, property taxes, and maintenance are just a few of them.

A much more realistic calculator is this one from the New York Times. Plug your numbers in the NYT calculator and then a generic mortgage calculator and see how different the numbers are.

The Right Time to Buy a Home

The decision to buy a home doesn’t hinge on a universally right or wrong time; instead, it depends on whether the conditions are favorable or unfavorable for making such a purchase.

Significant life changes can profoundly impact the decision to purchase a home, as they often alter one’s financial stability, needs, and long-term plans. Here are some of these key life events:

- Marriage or Partnership: Merging incomes might make home-buying more feasible, but requires considering both partners’ needs and finances.

- Divorce or Separation: This can significantly impact financial situations and possibly necessitate a move.

- Starting a Family: The need for more space and increased expenses can influence home purchasing decisions.

- Career Changes: New jobs or changes in income can affect affordability and the desire to buy a home.

- Relocation: Moving for work or personal reasons can lead to buying a home in a new area.

- Changes in Health: Health issues may require a home that accommodates new needs.

- Financial Windfall or Inheritance: Sudden financial gains can open up new possibilities for home ownership.

- Paying Off Significant Debt: Eliminating debts can improve financial standing and make home-buying more viable.

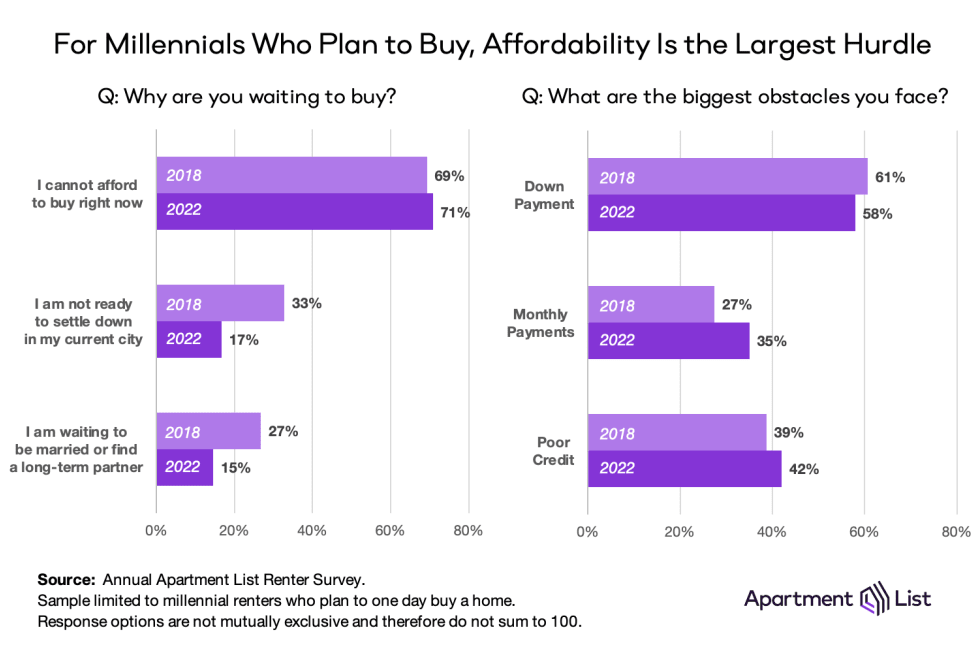

Millennials looking to buy a house often find affordability to be their biggest obstacle. With the burden of student loans, soaring housing prices, and sluggish wage increases, many in this generation struggle to bridge the gap between their financial realities and the dream of homeownership, making it a challenging goal to achieve.

No one can predict what will happen to the economy but are the signs of things like a coming recession, are banks handing out mortgages in this economy, or are they forcing buyers to risky alternatives?

Do you still have credit card or student loan debt? If you do, it’s ridiculous to add more debt into the mix.

Are you married and planning to start a family soon? Are you happy in the city you live in? Do you have a steady career that provides a good income? Are world leaders acting like grown-ups and playing nicely with one another?

Get our best strategies, tools, and support sent straight to your inbox.

How To Save Up For A House

Just because the time and conditions aren’t right for you to buy a house at the moment doesn’t mean you can’t save up for a house right now.

First, you have to know your numbers and be realistic about them. If you make $60,000 a year, you can’t afford a $500,000 house even if a bank will loan you the money. Use the 30% guideline; your housing expenses should be no more than 30% of your income.

It's not how big the house is, it's how happy the home is.

Tweet ThisNext, decide your timeline. Do you want to buy a home in the next two years, five years, ten years? Take your 20% down payment number and add another 10% to it, closing costs alone can be between 2-5% of the purchase price, so an additional 10% isn’t unrealistic.

Divide your 30% down payment number by the number of months in your timeline, and you have your goal.

Make More

Making more money is generally more impactful than saving money, and this isn’t an extra $100 you need, it’s tens of thousands, so clipping coupons and not buying Starbucks isn’t going to get you there.

Ask your boss for a raise but be prepared to show why you deserve it. If you don’t get a raise or enough of a raise to make a real difference, start looking for a new job. The average raise is just 3.9% while the jump in income when you change jobs is a much better at 10-20%.

Everyone should have more than one source of income, and that is undoubtedly true if you want to save up for a house. Use your weekends and evenings to make extra money by driving for Lyft or babysitting.

Even making a few extra bucks with Survey Junkie or Ebates in your downtime can help you reach your goal.

Spend Less

Yes, earning a higher income can be a quicker path to saving for a house, but reducing your expenditures remains crucial. Regardless of whether your goal is to save for a home, minimizing spending is beneficial for your financial health.

The first step is always to make a budget if you don’t have one. A budget doesn’t stop you from spending money but it does show you where your money is going so you can plug any spending leaks.

There are many relatively effortless strategies to save money for a house. For instance, using services like Rocket Money can help cancel subscription services you’ve forgotten about or no longer utilize, trimming unnecessary expenses seamlessly.

When you go out to dinner (which you should cut back on when you’re trying to save up to buy a house!) use Seated to make your reservation. When you complete the reservation, you’ll get a $10-$50 gift card to Amazon, Lyft, or Starbucks.

LMM has articles on how to save on everything from gifts to food to dates.

Where to Put Your Money

Where should you keep the money you’re saving up for a house? It depends on your timeline. Any money you are saving and plan to use in five years or less should not be invested. While investing is safe over the long term, it can be risky in the short term.

Short-term money should be kept in a high-yield savings account or a CD. Check out CIT Bank. Their savings account offers competitive rates. Consumers Credit Union is offering high rates on 10-month CDs.

If you’re planning to buy a home in more than five years, consider investing your savings. This approach prevents your money from sitting idle and earning minimal interest over time.

Accelerate your journey towards your financial aspirations with Premier Savings. Tailored to align with both your ambitions and lifestyle, this savings account offers an exceptional APY of 4.81% on balances exceeding $1,000. They value your hard-earned money by eliminating any monthly or annual account fees.

Should You Do It?

We’re not advising against buying a home. We aim to provide you with a more comprehensive view. The decision to purchase a home should be based on personal readiness and financial logic, not merely because it seems like the societal expectation or the next step in adult life.

Take a good look at the numbers to make sure buying a house fits where you’re at in life and works out for you.

Show Notes

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.