A 401k is a retirement investment account. It’s the first foray into investing for many of us and is an important part of your overall portfolio. We’ll break down how much to contribute to your 401k retirement account based on your age.

A 401k is What Now?

A 401k is an employer-sponsored retirement savings vehicle that allows you to invest part of your paycheck, pre-tax, into a retirement investment account where it grows tax-free until you are ready to start withdrawing from it after age 59 1/2.

Most plans are made up of mutual funds that include stocks, bonds, and money market investments.

The money is taken directly from your check before it hits your checking account, so it’s a built-in way to save consistently, which is a big component of successful investing.

A key to any retirement plan is to save consistently. Determine a percentage of your salary you will contribute each month and stick to it.

Source: Brad Sherman, president of Sherman Wealth Management

While you only have the choices your employer offers, Personal Capital can help you set a fund allocation that works well with your other investments.

A 401k also lowers your taxable income. If you earn $5,000 a month and invest $1,000 into your account, you are only taxed on the remaining $4,000.

Do You Like Free Money?

Of course, you do. And if your employer offers to match, you’re in luck! If you invest 6% of your income, for example, the company will match 3%.

Even if you have high-interest consumer debt, like credit card debt, you should invest enough to get the match because it is free money!

I believe that free money is as addictive as cocaine.

Tweet ThisFor 2018, you can invest up to $18,500 a year in your 401k. If you are over 50, you can contribute up to $6,000 more for a maximum of $24,500 per year.

If you’re going to invest in a 401k, you want to get the most out of it. The default contribution is 3%, but you should be saving at least 10% for retirement.

Make sure you’re contributing more than the minimum 3% and ideally at least the minimum to get matching.

Each time you get a raise, increase your contribution. Raises don’t always make a big difference in our paychecks, but that boost in your 401k will make a difference over the time the money has to grow.

And remember, beware of fees because they can eat into your retirement savings.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

You Can Take It With You

Presumably, most of us are not going to stay at one job for our entire career. On average, people change jobs twelve times over the course of their career.

You don’t want to have a bunch of different 401k’s scattered around.

You have a few options, some employers will allow you to leave the account, you may be able to roll it over to the new employer’s plans, or you can cash it out.

Cashing out is a terrible idea because you’ll take a tax hit and be penalized for early withdrawal if you’re not 59 ½ or older.

The best course of action is to transfer the money to an IRA rollover. There is no tax penalty for doing so, and you will be able to choose your investments.

Empower can handle this for you.

Plan for retirement with our free tools today.

- Get your Retirement Readiness Score™ in minutes.

- Run the Recession Simulator to get perspective on today’s market.

- Use Fee Analyzer™ to find hidden fees in your retirement accounts.

Bench Marks

Great, so you want to invest in a 401k, or you currently are. But how do you know if it’s enough? While financial numbers are individual for everyone, there are some benchmarks we can use to make sure we’re on track for a healthy 401k.

While this article is specific to 401k’s, that shouldn’t be your only investment vehicle, just a part of your overall portfolio.

We did a separate article on how much your net worth should be according to your age.

Remember, the earlier you start investing, the better.

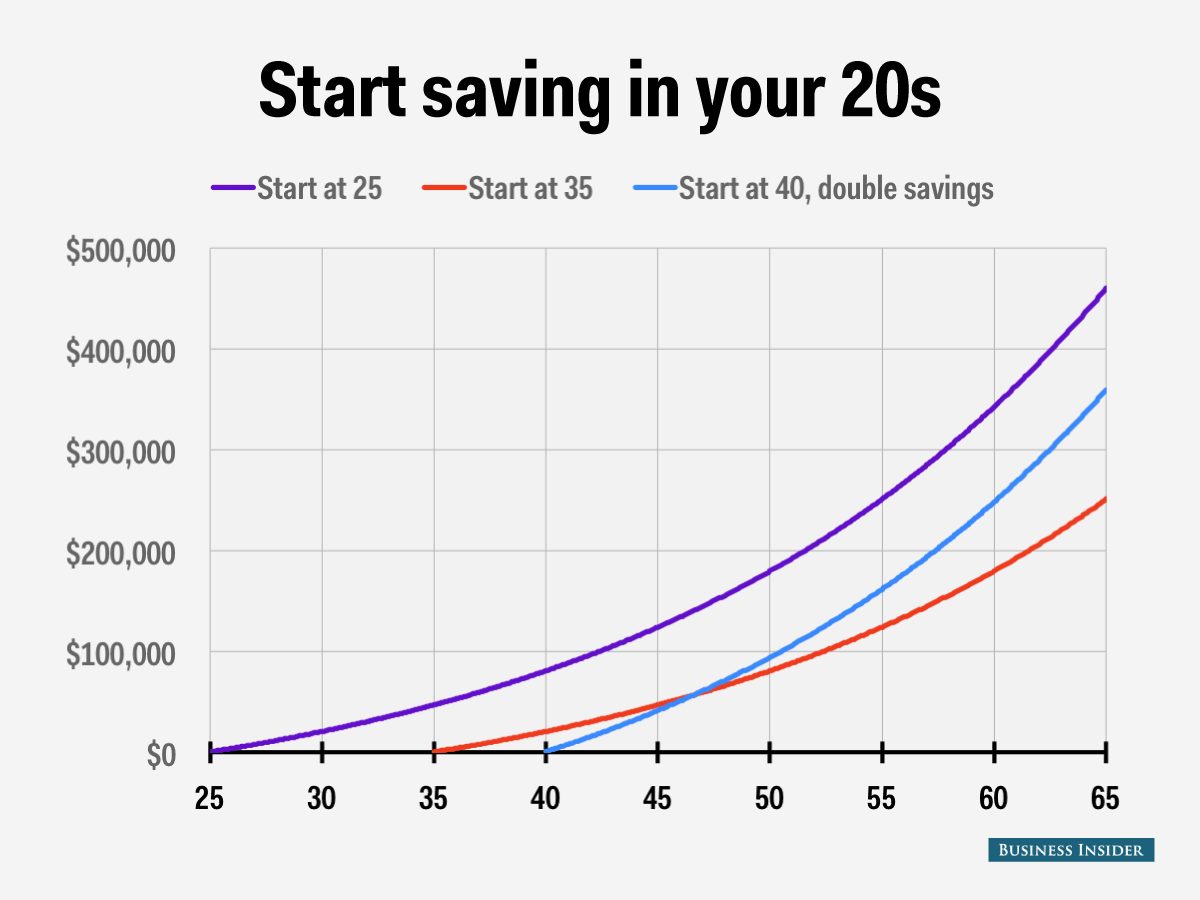

In Your 20’s

It can be tough to save for retirement in your 20’s because most of us aren’t making a ton of money yet, and we may have student loans and credit card debt.

If your student loan debt interest is high, you can refinance to a lower rate with Earnest.

If your rate is already low, you can put paying this debt off on the back burner in favor of investing because the average you can earn in the market is higher than the interest on your loan.

Hustle to get the credit card debt paid down. But in the meantime, if you get matching, contribute the minimum you have to to get that. Because like we said, free money.

Saving for retirement in your 20’s can be easy because you don’t yet have a lot of obligations. Don’t fall victim to lifestyle inflation.

If you make the right moves now, you will be well on the road to financial independence.

Ideally, you are saving 10% of your income for retirement. You can save that entire 10% in your 401k, or consider additional retirement investments like a Roth or Traditional IRA.

We would recommend people in their 20’s invest in the Golden Butterfly Portfolio.

This portfolio is a modified version of the Permanent Portfolio with one additional asset class. This is done to incorporate some of the characteristics of a few other notable lazy portfolios.

In Your 30’s

Your 30’s are often the best decade in which to save for retirement. Hopefully, your debt is paid off or at least manageable.

You are making more money than you were in your 20’s; you may now be part of a two-income household, which takes some pressure off even after you start a family or buy a home.

You aren’t panicking about how you’ll pay for college, and your parents don’t need any financial help. All of those things can change, so in your 30’s you need to save, save, save!

It may not be realistic to max out your 401k at this point; $ 18,500 may be more than you can afford to put away but be sure to steadily increase your contribution each year.

If you are making enough to max out, consider opening an IRA as well.

It’s another retirement savings account that you can open once you’ve reached the 401k max for the year. If you have or plan to have children, now is the time to start a 529 College Savings Account.

If you’re looking to buy a home, make sure your credit score is 760 or above. You want the best possible mortgage rate.

If your score isn’t quite there, we can help you bump it up. Make sure you have at least a 20% down payment so you can avoid the expense of PMI.

We would recommend people in their 30’s invest in the All-Weather Portfolio.

This portfolio's single goal is to make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is. It does this by focusing on growth and inflation cycles.

In Your 40’s

If you haven’t started saving for retirement, you have got to buckle down and catch up. You need to make some tough decisions.

If you were planning to help your kids with college, forget it. They have a lot more time to pay off student loans than you have to save for retirement.

You need to bring in some additional income to kick-start your retirement savings. Start a side hustle, drive for Uber on weekends.

If your partner has been a stay at home parent, the kids aren’t little anymore. They need to get a job and start contributing.

No more vacations and elaborate holiday celebrations. Every bit of extra money you can find needs to be going into your retirement accounts.

We would recommend people in their 40’s invest in the Ivy 5 Portfolio.

This portfolio attempts to diversify your money by dividing it into stocks, bonds, commodities, and real estate in a way that mirrors the Ivy League endowment funds. It doesn't attempt to mirror every move the endowment fund makes.

In Your 50’s

Age has its perks. If you’re 50 or older, you can bump up your 401k contributions from $18,500 a year to $24,500. Start doing that; you’re in the final stretch. You can bump up your IRA contributions, too, from $5,500 to $6,500.

Now is the time to start thinking about what you want your retirement to look like. Will you continue to work in some capacity?

Will you live in the same area or move to a place with a lower cost of living?

If you plan to stay, will you stay in your home or downsize now that you have or will soon have an empty nest?

If you still have a mortgage, you need to pay it off aggressively. You don’t want to retire with mortgage payments hanging over your head.

If you have not yet created a passive income stream, now is the time. Rental property, REIT’s, dividend stocks. You want to continue to generate some income after retirement.

Evaluate your health and that of your spouse. If you have health issues, it’s not too late to address them, but too late is not far off.

Based on your health, evaluate your insurance. Do you have enough and the right kinds?

We would recommend people in their 50’s invest in the Larry Portfolio.

This portfolio's goal is to be both high performance and low volatility. It achieves its performance by tilting your portfolio to higher-risk stocks that are underpriced. Its low volatility is due to only holding 30% in stocks while 70% goes to bonds.

In Your 60’s

At this point, you are hopefully pretty set to retire. If you have left saving until now, you’re going to have to keep working, probably until you physically can’t work anymore.

There are some final steps you should take before you get that gold watch.

Now is the time to decide when to start collecting Social Security. The longer you wait, the more money you will get each month.

AARP has a calculator that can help you decide when to claim. Start compiling a retirement budget.

You can’t afford as much risk in your asset allocation anymore, but if you’re in good health, you may have decades of life left, so you can’t get too conservative either.

Tweak numbers based on other personal circumstances, but a good rule of thumb is to base your asset allocation based on your age. Subtract your age from 120 to get the right ratio. That means a 60-year-old should be allocated 60/40 stocks to bonds.

We would recommend people in their 60’s invest in the Permanent Portfolio.

The Permanent Portfolio (PP) is a portfolio evenly split between stocks, bonds, gold, and cash. It’s best suited for risk-averse investors wanting to minimize losses while still receiving modest returns.

Fees

If you’re not careful, you can lose more than 25% of your 401k to fees. Personal Capital’s Fee Analyzer can show you how much you’re paying in fees. You can visit their site, register your account, and add in financial institutions, much like Mint.

Empower's free fee analyzer helps you understand how investment fees affect your retirement savings. It analyzes your holdings, estimates future fee impact, and suggests ways to potentially save by lowering fees in your retirement portfolio.

From there, you’ll go to the Investments header in the top right, and click 401k Fee Analyzer. On the page, you’ll be greeted with an excellent graph of your potential 401k earnings.

Read the fee disclosure statements for each plan your employer offers and choose the fund offering the lowest fees.

If all of the choices have high fees, you may want only to contribute enough to get the match from your employer and put the extra money in an IRA.

You could also research some options with lower fees and ask your HR department if they would consider making those options available.

The Whole is Greater than the Sum of its Parts

Your 401k is important. You want to get the most out of it you can. But it’s only one part of your overall investment plan.

Get your 401k fully funded and fully healthy, and it’s pretty much set it and forget it after that. Then you can start worrying about your other investments!