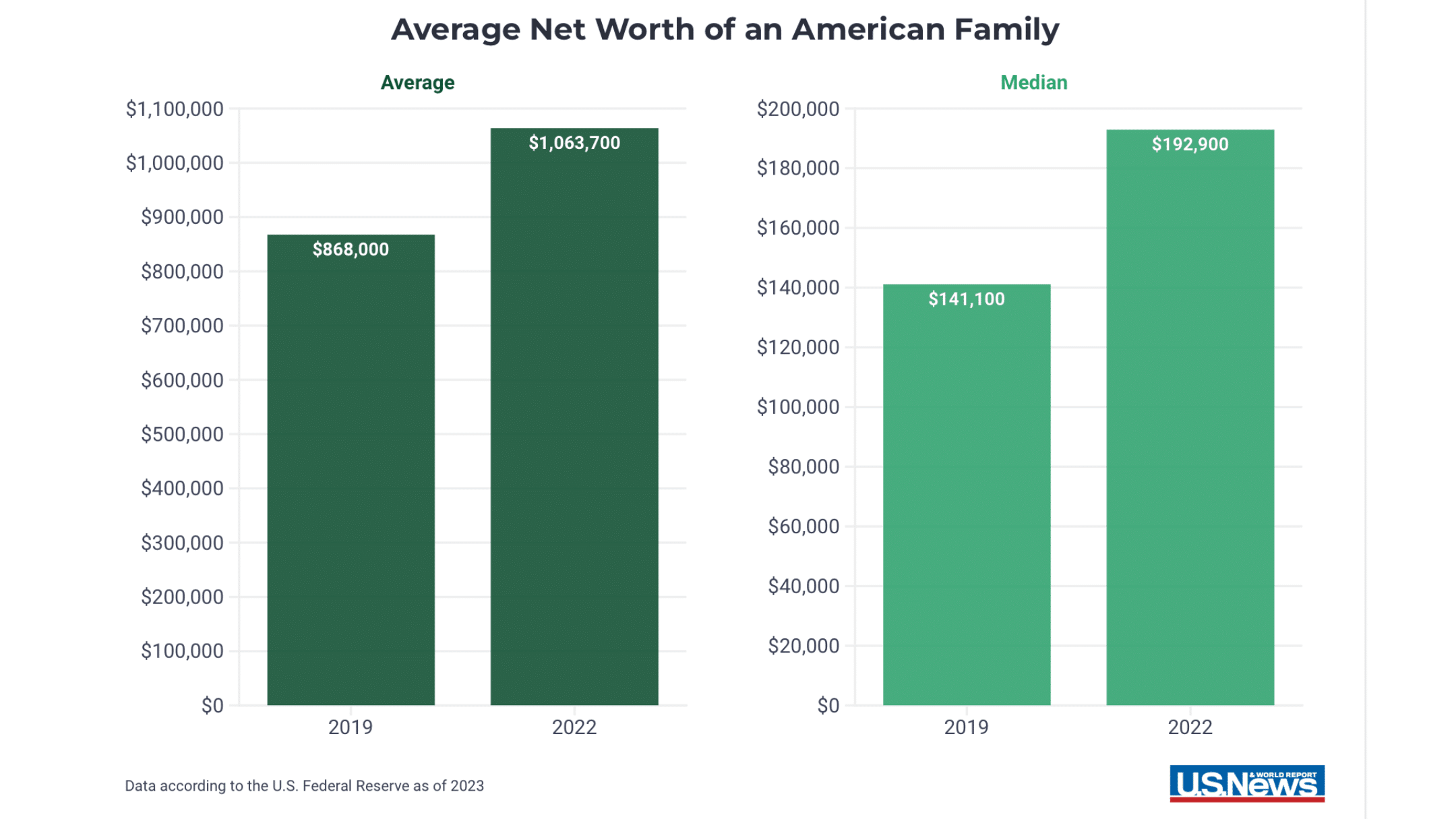

The average net worth of Americans is $1,063,700. How does that number compare to yours? This post breaks down the average net worth by age group. You’ll love this post if you want to discover how secure your financial future looks. Let’s get started.

Understanding your net worth is crucial because it reflects your overall financial health—what gets measured gets managed. Without this number, you lack a comprehensive view of your financial situation.

What Is Net Worth?

Net worth is simply your financial health snapshot. It’s calculated by subtracting what you owe (liabilities like loans) from what you own (assets like savings or a house). A positive net worth means you have more assets than you owe. Tracking your net worth helps you understand your financial progress over time.

Whether you want to be debt-free and raise your credit score, are looking to become a homeowner, pay for your children’s college degree, or retire, you need to be on target.

Net Worth Calculation

To calculate your net worth accurately, you should show the value of your home and auto gross (full market value) as an asset and include any outstanding mortgage or loan balance as liabilities.

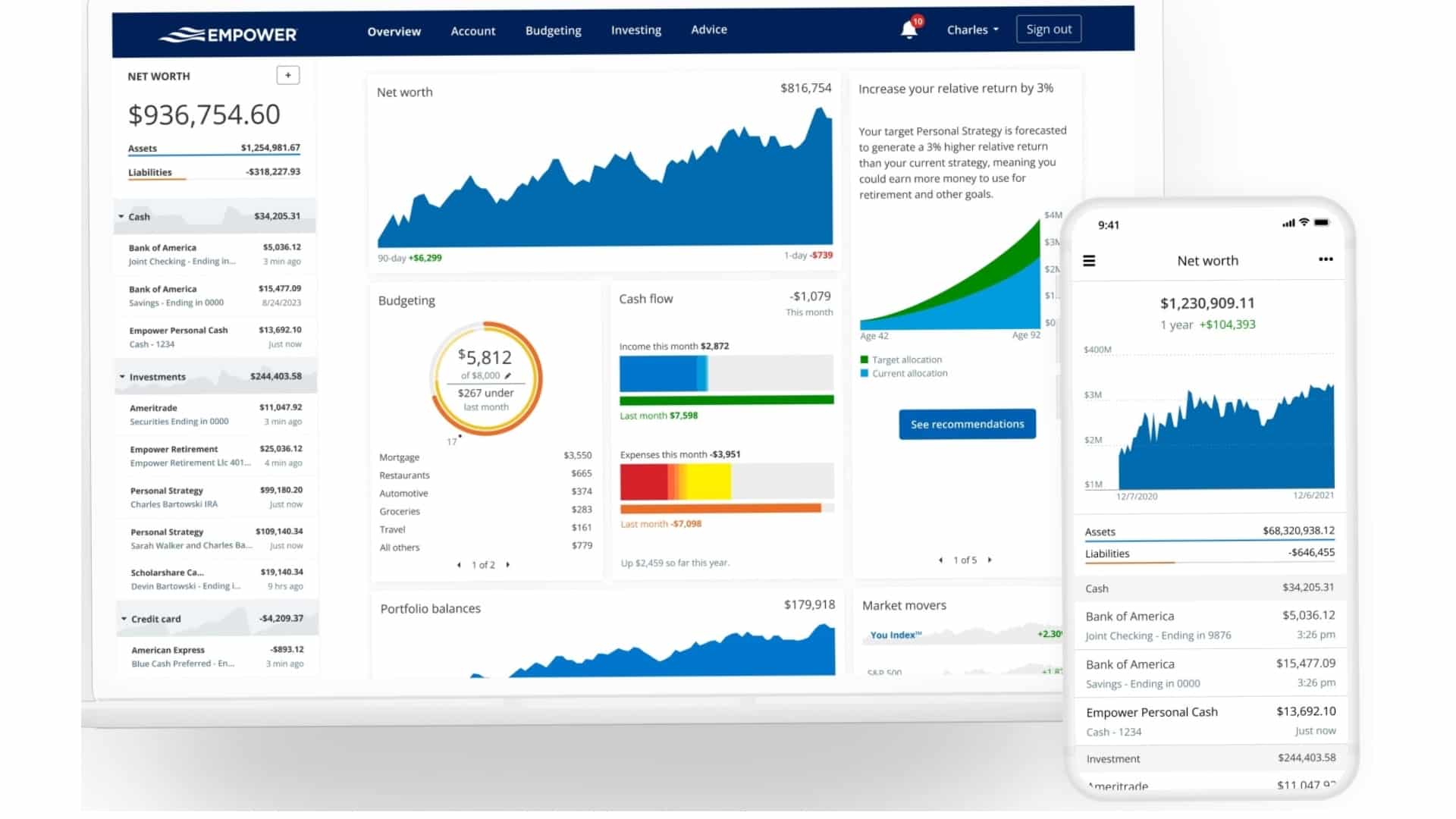

Empower can be a helpful tool to get a clearer picture of your overall financial health. By connecting your accounts and using their budgeting features, you can track your income, expenses, and assets to calculate your net worth. While Empower might show general benchmarks or average net worth figures, it likely won’t provide super detailed comparisons to others by age or income bracket.

Budget like a business and focus on your cash flow. In addition to their budgeting software, they have an awesome suite of tools to help you optimize your investments. Did we mention it's free?

What Does Net Worth Include?

Net worth is the total value of everything you own minus all the debts you owe. It includes all your assets like your house, car, savings, and investments, minus any debts such as your mortgage, car loans, and credit card balances. Simply put, it’s what you have minus what you owe.

Assets for Net Worth Calculation

Assets represent all the valuable things you own that contribute to your financial well-being. To get an accurate picture of your net worth, it’s important to consider these assets. Here’s a breakdown of some common categories:

- Liquid Assets: Cash, checking, and savings accounts.

- Investment Accounts: Stocks, bonds, mutual funds, retirement accounts (like IRAs or 401(k)s).

- Real Estate: Your primary residence, vacation properties, or any other land you own.

- Tangible Assets: Cars, motorcycles, boats (anything with resale value).

- Valuable Possessions: Art, jewelry, antiques (things with significant resale value).

- Life Insurance Cash Surrender Value: This is the amount of money you’d get if you cashed out your life insurance policy before it matures.

While calculating your net worth, it’s important to consider what shouldn’t be included. Here are some items that typically don’t hold significant resale value and are excluded:

- Everyday Household Items: These include things like towels, furniture, and appliances. While they may have value to you, their resale value is generally low.

- Debts Receivable: Money owed to you by others is technically an asset. However, it’s uncertain when or even if you’ll be able to collect it, so it’s not typically factored into net worth calculations.

Liabilities for Net Worth Calculation

Liabilities represent all your financial obligations that you owe money on. To calculate your net worth accurately, you need to factor in these debts. Here’s a breakdown of some common liabilities:

- Credit Cards: The outstanding balance on your credit card statements.

- Student Loans: The total amount of money you borrowed for education, including any accrued interest.

- Car Loans: The remaining balance on your car loan.

- Personal Loans: Any loans you took out for personal reasons, such as home renovations or debt consolidation.

- Mortgage: The outstanding balance on your home loan.

In addition to these, other potential liabilities include:

- Medical bills

- Money owed to businesses

- Unpaid taxes

What Gets Measured Gets Managed.

Now that you know your net worth, what should it be? The numbers are different for everyone because there are a lot of variables involved, but there are some general yardsticks that you can measure your numbers against.

Median vs. Mean Net Worth

Mean net worth is the average number of all the net worths. The median is the number that falls in the middle (or the middle value of the mean).

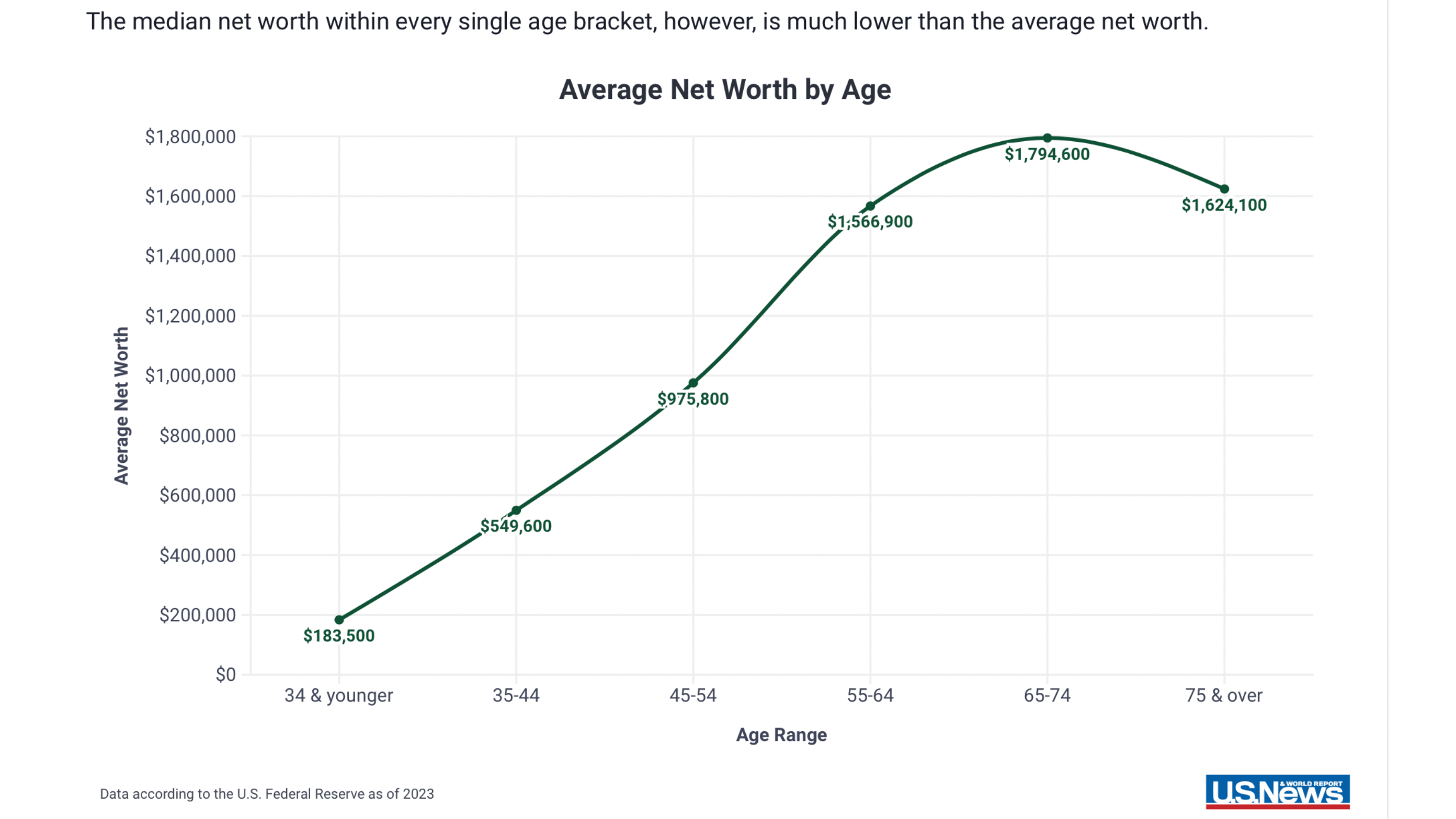

Here is the mean and median net worth by age. Remember, the mean is skewed by the nation’s super-wealthy, so don’t freak out.

For example, if you’re comparing the mean net worth of people in their 50’s, Jeff Bezos (valued at $200 billion as of March 2024) gets included along with the average American.

But the overall figures are just one indicator.

Get our best strategies, tools, and support sent straight to your inbox.

What’s a Good Net Worth at 30?

According to US News Money, the average net worth in the U.S. for those under 35 was $183,500 as of 2022.

Prior work experience gained during your teens and college years may have equipped you with valuable skills. However, the financial realities of adulthood, particularly student loan debt, can present a significant challenge when attempting to accumulate wealth.

General Financial Guideline: Most financial planners suggest aiming to save about one times your annual salary by the age of 30. This target strikes a balance between being challenging and achievable, providing a robust foundation for future wealth accumulation.

Individual Goals Matter: Personal priorities such as career growth, buying a home, or even traveling can influence your savings goals. It’s important to tailor your financial plan to fit these personal ambitions, which might mean adjusting how much you save accordingly.

You may not have had a budget while you were in high school or college. If not, now is the time to make one. A budget will tell you what’s coming in and going out each month.

It will show you where you are wasting money that would be better spent paying off your credit card balance or investing for your future.

Take a look at “Learn how to budget like a pro” and build your budget.

Use the 50/30/20 Budget Rule.

Feeling overwhelmed by budgeting? The 50/30/20 rule offers a straightforward approach. Simply divide your income into three categories: 50% for essentials like rent and utilities, 30% for flexible spending like groceries and entertainment, and 20% towards your financial goals. It’s a great starting point to organize your finances

Budget like a business and focus on your cash flow. In addition to their budgeting software, they have an awesome suite of tools to help you optimize your investments. Did we mention it's free?

Invest Your Money to Build Wealth

Now that we’ve established the importance of creating a budget and managing your student loan debt, it’s crucial to plan for the future with the money you’ve saved. The next step is to start investing.

Each day you delay investing equates to potential gains lost. Investing isn’t magic, but it does have a secret ingredient: time. The sooner you begin, the better your financial future can look.

Typically we recommend people under 30 invest in the Golden Butterfly Portfolio. This strategy is known for diversification and moderate risk. It could be a good fit for young investors with a long-term horizon (10+ years) who prioritize capital preservation along with some growth potential.

This portfolio is a modified version of the Permanent Portfolio with one additional asset class. This is done to incorporate some of the characteristics of a few other notable lazy portfolios.

What you do in your 20s can lay the foundation for your entire financial life.

Tweet ThisEven small amounts of money invested now will grow exponentially because of the power of compound interest.

Where to Invest

Great, you’re ready to start investing. These are the places to do it.

- Brokerage Account: If you want to buy stock in individual companies, you’ll need to open a brokerage account. You can do that with companies like Robinhood, Charles Schwab, or Fidelity. You need to do some research before buying stock in individual companies.

- Mutual Funds: You can buy a mutual fund directly from a mutual fund company like Dimensional Funds, BlackRock, or T.Rowe Price. They can also be purchased through some banks or brokerage firm.

ETFs: You can buy ETFs through companies like M1, Wealthfront, and Empower.

To maximize capital appreciation, start investing with brokerage firms like Vanguard, robo-advisors, or your employer’s 401(k) if available (especially if your employer offers matching).

Wealthfront is ideal for beginners with no minimums and low fees, making it accessible to those new to investing. Conversely, consistently contributing to a 401(k) is crucial. Many fail to invest by waiting to see if money is left at month’s end; it’s more effective to prioritize investing upfront. This “pay yourself first” strategy ensures regular, disciplined investment, leveraging compound interest to build wealth.

If you want to discover more about investing, we designed a blueprint to guide you through the process.

Reaching Your Goals

We like Empower because:

-

- It’s easy to use and free: Empower’s financial tools, mobile app, and web platform are free to use. You can connect your bank and credit card accounts for transaction tracking and budget planning.

- Budgeting features: Empower offers budgeting tools that allow you to set up spending categories and track your progress.

- High-yield cash account: Empower offers a high-yield cash account that typically pays interest rates higher than traditional savings accounts. This can help you earn a little extra on your un-invested money.

- Debt management tools: Empower offers tools to help you track and manage debt, including credit score monitoring and tools to create repayment plans.

- Security features: Empower uses industry-standard security measures to protect your financial data.

- Goal setting: You can set specific financial goals within Empower, which can help you stay motivated and track your progress towards achieving them.

What’s a Good Net Worth by 40?

The average net worth for Americans between the ages of 35 and 44 is $549,600 (the earlier chart).

Your goal in your 30s is to have twice your yearly salary saved by age 40. If you’re now making $75,000, you should have a net worth of $150,000 when you’re a 40-year-old.

Consider the following:

- Consider Your Circumstances: This goal might not be achievable for everyone, especially for married couples with children. Here’s why:

- Increased Expenses: Children introduce additional costs like childcare, education, and healthcare.

- Dual Income vs. Single Income: If one spouse stays home with children, it can impact total household income.

- Student Loan Debt: Existing debt can hinder saving progress.

- Individualized Goals: Savings targets should be personalized. Consider your priorities: early career advancement, a down payment on a house, or higher education savings for your children.

- Alternative Benchmarks: Many financial experts recommend having 1x your annual salary saved by 30, not necessarily twice your salary by 40. This might be a more realistic target for couples with children.

Achieving These Goals

-

-

- Credit Card Debt – To pay off credit card debt efficiently, you can consider two methods: the snowball and the avalanche methods. Both have advantages and disadvantages, so understanding the specifics will help you choose the best approach for your situation.

- Student Loan Debt – Overwhelmed by multiple student loans? Consolidation simplifies repayment, offering one payment and potentially a lower rate for easier management and potential long-term savings.

-

What Should Your Net Worth Be at 50?

The average net worth for Americans between the ages of 45 and 54 is $975,800. The general guideline is that by age 50, your net worth should be roughly four times your salary.

If you make $100,000 a year, your target is $400,000. The good news is that this is likely to be the time in your career when you earn the most money you will ever make.

Consider Your Circumstances: This goal might not be achievable for everyone due to factors like student loan debt, cost of living variations, and starting salary impacting savings potential

- Variations in Recommendations: Financial experts often suggest having a net worth between three and a half to six times your annual salary by 50, offering some flexibility based on your situation.

- Individualized Goals: Savings targets should be personalized. Consider your priorities: early career advancement, a down payment on a house, or other financial goals.

Grow Your Passive Income

It’s also an excellent time to start looking for ways to create a passive income stream. You now have more working years behind you than you have ahead of you, and you need to find ways to have money coming in after you’ve stopped working.

Rental properties offer a path to passive income, where rent payments provide a steady stream of cash flow. However, achieving a truly hands-off experience requires setting yourself up for success. This involves careful property selection, meticulous tenant screening, and potentially hiring a property management company to oversee day-to-day operations. By laying this groundwork, you can maximize your returns while minimizing the active management required.

Our proven, data-driven approach to building a portfolio of income-producing rental properties that perform in the long-term.

You can see the LMM course for rental properties here.

If you want to invest in real estate without owning a property, Fundrise offers an alternative similar to ETFs in that they allow investment with a lower minimum amount. However, unlike ETFs, Fundrise eREITs are not publicly traded and invest directly in real estate projects, resulting in lower liquidity.

Diversify into income-producing real estate without the dramatics of actual tenants. Fundrise eREITs are a diverse family of funds, each of which pursues a focused real estate investment strategy.

Disclosure: When you sign up with this link, we earn a commission. All opinions are our own. I am investing with Fundrise

What Should Your Net Worth Be at 60?

The average net worth for Americans between the ages of 55 and 64 is $1,566,900. Having a net worth of six times your annual salary by age 60 is a reasonable goal for many people aiming for a secure retirement. However, it’s important to consider your individual circumstances and desired retirement lifestyle to determine a more personalized target.

What Will Your Retirement Look Like

Boost Your Savings with Contribution Limits Tailored to Your Age:

Great news for retirement savers! The maximum contribution (for 2024) you can make to your retirement depends on your age. If you’re under 50, you can contribute up to $23,000 annually to your 401(k), while IRAs allow for $6,500. For those fortunate enough to be 50 or older, these limits jump significantly, with 401(k)s reaching $30,000 and IRAs allowing a hefty $7,500. Take advantage of these generous limits to accelerate your retirement nest egg, regardless of your current age.

Envision Your Ideal Retirement Lifestyle:

Now’s the perfect time to daydream about your golden years. Will you become an empty nester, downsizing your home for a more manageable lifestyle? Imagine the freedom of location independence after your career winds down. Perhaps a new locale with a lower cost of living beckons?

Reimagine Your Future Career:

Retirement doesn’t have to mean complete idleness. Consider continuing to work, whether part-time or as a consultant. Is there a passion project or long-held career aspiration you’d like to pursue now that finances are less of a constraint? Maybe a return to school is in the cards! Don’t feel pressured to make choices yet, but start brainstorming possibilities for a fulfilling post-work life.

Get the Correct Insurance Coverage

Securing the right insurance coverage can safeguard your financial future in the face of unexpected medical bills or disability.

- Medical debt is a leading cause of bankruptcy: Studies show medical debt is a major factor in a significant portion of bankruptcies, often cited as the highest single cause.

- Insurance doesn’t always protect from medical debt: Having health insurance doesn’t guarantee immunity from bankruptcy due to medical bills. High deductibles, out-of-pocket maximums, and uncovered services can leave people with substantial costs.

Additional points to consider:

- Disability insurance is important: If you can’t work due to illness or injury, disability insurance can help replace lost income, making medical bills more manageable.

- Family health history matters: Knowing your family’s health history can help you plan for potential future medical needs.

- Long-term care insurance can be beneficial: Medicare may not cover everything, and long-term care insurance can help offset the costs of in-home care or assisted living facilities

Net Worth by Retirement

The average net worth between the ages of 65 and 74 is $1,794,600. The general guideline is that when you are ready to retire, you should have roughly ten times your final salary in your nest egg.

Consider the following:

- Individual Needs Vary: This is a simplification. Factors like desired retirement lifestyle, Social Security, pensions, location, and potential healthcare costs can significantly impact your actual needs.

- Other Rules of Thumb Exist: Some recommend a higher target, like 12 times your salary by retirement.

The 4% Rule

The 4% rule is a starting point, with historical data suggesting a 4% withdrawal rate from a balanced portfolio could last 30 years. This is, of course, not guaranteed. Market fluctuations and individual lifespans can impact success.

Considering Your Ideal Retirement

- Lifestyle: Will your desired retirement lifestyle cost $60,000 per year? Consider relocation options for potentially lower living costs.

- Work: Do you plan to continue working part-time or as a consultant?

- Social Security: What age do you want to start claiming Social Security benefits?

Estate Planning:

- Wills and Trusts: Updating your will and considering trusts for beneficiaries can ensure your wishes are carried out.

- Power of Attorney: Designating someone you trust to make decisions on your behalf is crucial.

End-of-Life Considerations:

- Medical Care: Pre-planning your medical care preferences can provide clarity and peace of mind for you and your loved ones.

- Funeral Arrangements: Pre-planning and potentially pre-paying for funeral services can ease the burden on your family during a difficult time.

Embrace Your Golden Years:

While planning for retirement can involve some challenging discussions, having these things in place allows you to focus on enjoying the well-deserved relaxation and fulfillment you’ve earned.

Milestones

Don’t Stress About the Numbers: Everyone is Different

Financial situations vary greatly, so don’t be discouraged if your net worth isn’t where you imagine it should be. The ideas we’ve provided are meant to be a springboard, and the specific numbers will be unique to your circumstances.

Some people plan to retire in low-cost-of-living areas, while others choose to remain child-free, potentially saving hundreds of thousands of dollars over time. Inheriting wealth or marrying someone well-off can also play a role.

Track Your Progress and Make Adjustments

Even though these are general guidelines, tracking your net worth can be a valuable tool. Compare your current position to your goals and identify any gaps you need to close.

Start Today, Secure Your Tomorrow

Remember, it’s never too late to take charge of your finances. Don’t wait – begin crafting your path to financial security today!